When the average person graduates from high school, they’ve already used up 93% of the total in-person time they’ll ever spend with their parents. They’re already in the tail end.

The same often goes for old friends. In high school or college, you hang around the same group of friends about five days a week. In four years, you probably rack up 700 group hangouts. Now, scattered around the country with totally different lives and schedules, you’re probably in the same room at the same time only 10 days each decade. The typical person leaving college is already in the last 7% of the time they’ll ever spend with their friends.

What do you do with this information? There are three main takeaways:

1) Living in the same place as the people you love matters. You probably have 10 times the time left with the people who live in your city as you do with the people who live somewhere else.

2) Priorities matter. Your remaining face time with any person depends largely on where that person falls on your list of life priorities. Make sure this list is set by you—not by unconscious inertia.

3) Quality time matters. If you’re in your last 10% of time with someone you love, keep that fact in the front of your mind when you’re with them and treat that time as what it actually is: precious.

_______________________________

U.S. corporate profits and stock market valuations are at historic highs, but the kind of real, productive investment that’s supposed to create those profits (building factories, equipment, infrastructure, etc.) has been falling for decades. Why have U.S. corporate profits and equity valuations reached historic highs despite a concurrent secular decline in net domestic investment?

In the mid-20th century, profits came from companies investing money to build things, sell more, and earn returns. Today, profits keep climbing even though companies aren’t really investing more in the real economy. So where are the profits coming from?

Federal budget deficits are the source. The government is essentially borrowing money and pumping it into the economy through programs like Social Security and Medicare, and that money flows almost dollar-for-dollar into corporate profits — which then get recycled into the stock market, inflating share prices.

Net Corporate Profits = Net Domestic Investment + Government Deficit − Household Saving − Foreign Saving.

This is just bookkeeping — it has to be true by definition. A government deficit is negative saving. When the government spends more than it takes in through taxes, it stimulates income and profits.

Here’s how it works in plain terms:

- The Treasury issues bonds and uses the money to send entitlement checks (Social Security, Medicare, etc.) to households

- Those households (mostly middle and lower-income, who spend nearly everything they get) go out and buy goods and services

- That spending shows up as revenue at corporations

- Because the spending didn’t require companies to spend more on production, most of it drops straight to the bottom line as profit

The wealthy people who originally bought the Treasury bonds basically just swapped cash for a Treasury bond — they didn’t lose anything. But the Treasury’s spending stimulates real consumption, which becomes corporate profit.

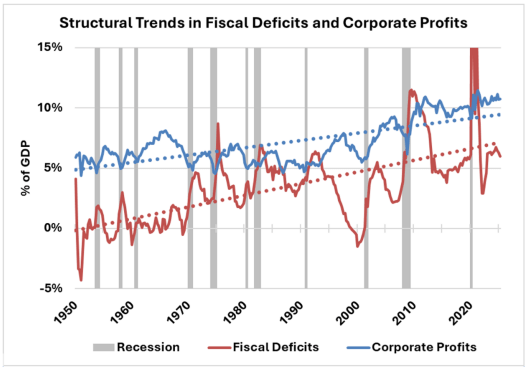

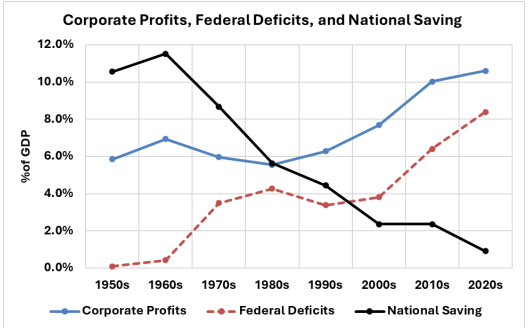

There’s a nearly one-for-one long-run relationship between fiscal deficits and corporate profits. In other words, every additional dollar of deficit roughly translates into a dollar of corporate profit over time. However, if you just look at quarterly correlations between deficits and profits, you’ll see a negative relationship — that’s because during recessions, profits collapse and deficits spike at the same time. But that’s a short-term cyclical effect that masks the long-term structural relationship.

The “natural experiment” occurred when the U.S. government briefly ran brief budget surpluses in the late 1990’s, withdrawing net spending from the economy. During this period of declining deficits and brief surpluses, corporate profits fell too. But with the recession in 2001, fiscal deficits returned and profits immediately resumed their upward climb.

What Happens Then?

Once corporations have these excess profits, what do they do with them? Here’s where the second half of the financialization story kicks in.

In a healthy economy, companies would reinvest profits into expanding production. But for decades, the returns on real investment haven’t been attractive enough to justify it (due to global competition, especially from China, weak domestic demand, etc.). So instead, firms returned profits to shareholders through dividends and buybacks.

Those distributions go mostly to wealthy households — and wealthy households don’t spend most of that money on goods and services. They reinvest it in financial markets, often through passive index funds. Mandated to remain fully invested, these funds then recycle the inflows to purchase stocks in proportion to their market capitalization indifferent to valuation, thus bidding up prices without any change in fundamentals.

In other words, an index fund doesn’t ask “is this stock cheap or expensive?” — it just buys mechanically. So when more money flows in, prices get pushed up regardless of underlying fundamentals. Research shows that each $1 of inflow increases market value by roughly $5 — meaning passive flows have an outsized impact on valuations.

How Did We Get Here?

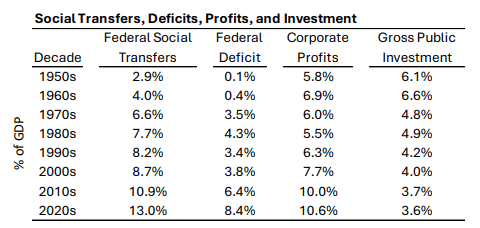

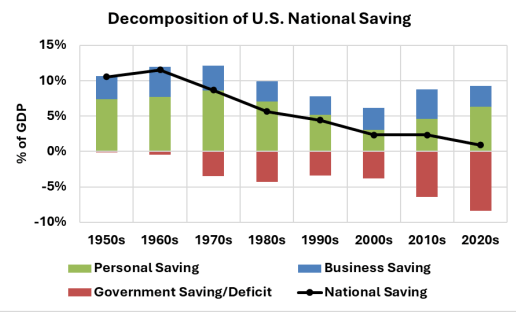

1. The collapse of national saving. In the 1950s and 1960s, net domestic investment, funded entirely by national saving, averaged 11% of GDP. But then structural fiscal deficits started to offset private saving, and national saving has now collapsed to nearly zero.

2. The long decline in interest rates. Two big forces pushed rates down: China joining the WTO in 2001 (which created huge trade surpluses that flowed back into U.S. Treasuries) and the post-2008 era of zero interest rate policy and quantitative easing. Cheap borrowing costs let the government run big deficits without “crowding out” private investment.

3. The shift from tangible to intangible investment. Gross domestic investment ebbs and flows with the business cycle, but its longer-term average has held relatively steady, only slipping from about 23% of GDP during the 1950s to 1980s to about 21% in recent decades. Net domestic investment has declined from nearly 11% of GDP in the mid-twentieth century to about 5% in recent years. Over the same period, depreciation rose from roughly 12% of GDP to more than 16%.

The reason: today’s “capital” is software, data, servers, and R&D — which depreciates and goes obsolete much faster than the factories, machines, and infrastructure of 50 years ago. So companies have to spend more just to replace worn-out capital, leaving less for genuine expansion.

4. The financialization of profits. As deficits soared from near zero in the 1960s to 8% of GDP by the 2020s, the profit share grew in parallel, from 6% of GDP to more than 10%. Over this same time, national saving collapsed from 11% of GDP to near zero.

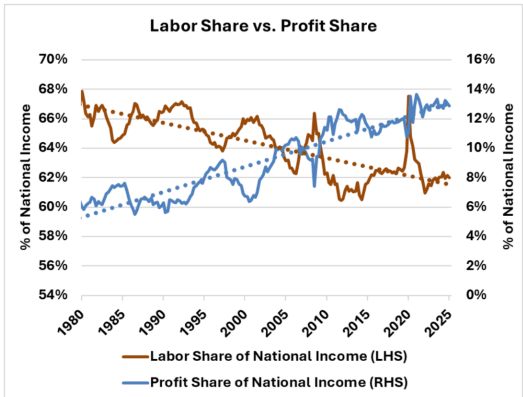

5. Growing inequality as a consequence. Because the profit share of GDP grew, the labor share necessarily shrank. Even as social transfers soared by 10% as a percentage of GDP, the labor share of national income entered a prolonged decline, falling from near 68% in the early 1980s to 62% by the mid 2020s. And because the rising profits accrue mostly to wealthy households, who don’t spend much in the real economy, this further fuels the cycle of recycling profits into financial assets.

There are competing theories for why corporate profits have grown so much — the “superstar firm” hypothesis (industry consolidation gives dominant firms pricing power), globalization (cheap foreign labor crushed wages), and the rise of high-margin tech companies with intangible-heavy business models.

While part of the equation, these factors operate within the larger macroeconomic environment established by fiscal and monetary policy. In other words: those theories explain which companies win, but the deficit story explains why the total pie of corporate profits has grown so much faster than the underlying economy.

What This Means Moving Forward:

The foundation supporting U.S. corporate profits and equity valuations has weakened, leaving the market increasingly fragile. Profits now depend on large-scale fiscal deficits, a sharp departure from the mid-century model when profits were generated by private investment of retained earnings.

Today’s stock valuations rest on continued (and growing) fiscal deficits. If at some point the U.S. is forced — by the bond market, by political will, or by a debt crisis — to reduce deficit spending, the entire mechanism that’s been propping up profits and stock prices could go into reverse.

Reversion to a healthier macroeconomic environment of declining deficit spending and greater net investment may cause sharp declines in both corporate profits and valuation multiples and likely trigger a financial crisis with politically toxic consequences. Ironically, the more palatable option may be to remain on the current path until a financial crisis imposes on us the discipline that we are unwilling to impose on ourselves.

_______________________________

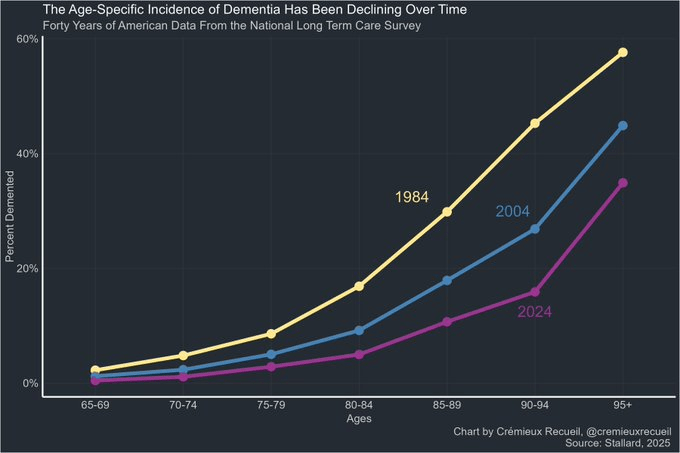

One of most exciting longevity trends right now is the decline in dementia. At a given age—70, 75, 80, etc.—the prevalence of dementia is down compared to what it was decades ago. Today’s 90-year-olds have less than half the risk of dementia that ones in 1984 did.