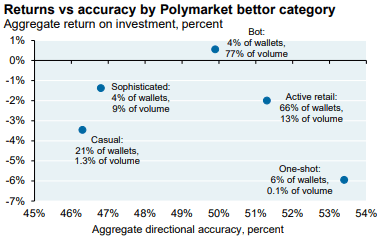

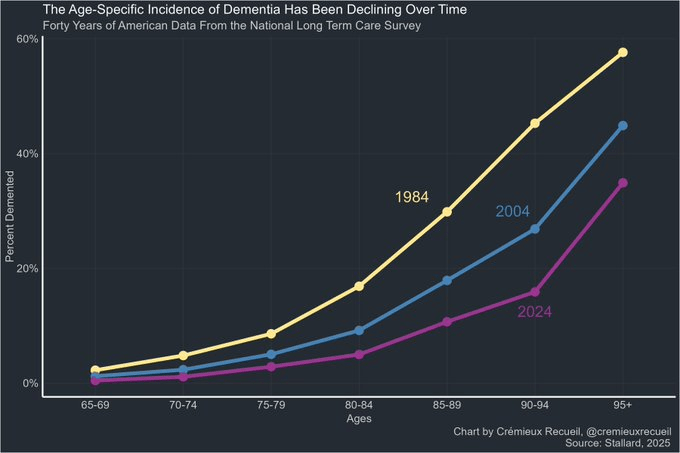

At its best, having an Oura ring makes you fitter, happier, and, sure, even more productive. You may walk more, lift more, sleep more, and drink less. You will be hard-pressed to find a physician who thinks there’s anything amiss in the previous sentence.

However, the obsession with winning the measurable games of health can encroach on the less measurable games of life. The best way to sleep more is to see fewer friends in the evening. The best way to lift more during the week is to eliminate social lunches to protect your midday gym time. To become a measurably enhanced self often means eliminating your less quantifiable sources of meaning and happiness.

The ring can improve your life. But its form of self-improvement often pulls you away from other people. This left me with a nagging question. At what point is it unhealthy for me—for anyone, for all of us—to be this obsessed with health?

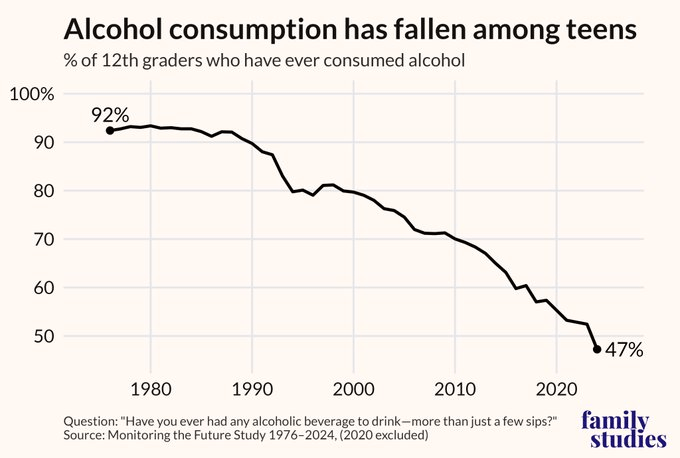

The share of people who drink hit an all-time low last year, according to Gallup, whose data go back to 1939. While many social changes happen slowly, the attitude shift against alcohol has been quite sudden. The decline of drinking is one part of a larger cultural phenomenon, the rise of the Enhanced Self.

The Enhanced Self is the evolution of medicine, technology, and consumer culture from an emphasis on curing illness to an obsession with optimizing normal, healthy life. We see this with the rise of GLP-1s, the explosion in biohacking with peptides, and the continued growth of supplements.

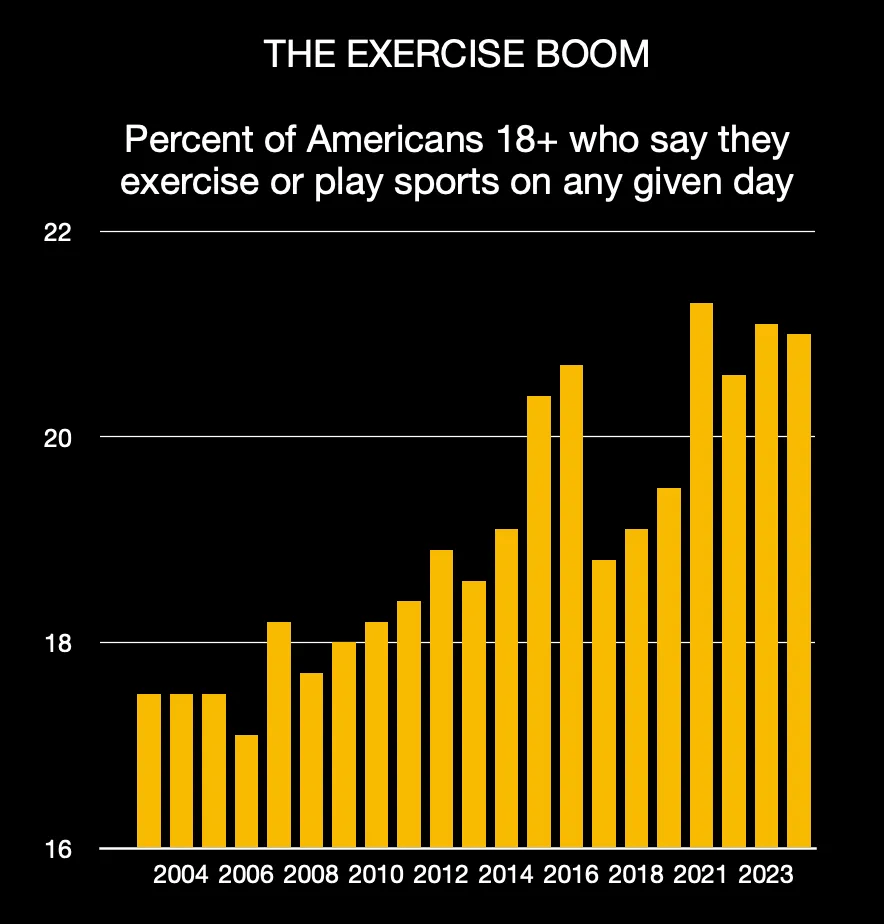

More Americans are using therapies not only to cure what is wrong with them but also to improve what is not wrong with them. At the layer of leisure, the tendrils of the Enhanced Self touch the white-hot rise of fitness in American life.

At the layer of biology, the Enhanced Self incorporates the belief that the human body is akin to a single-issue hardware device, whose owner should obsessively seek to extend its operating life beyond its scheduled date of obsolescence through relentless work and eagle-eyed neuroticism.

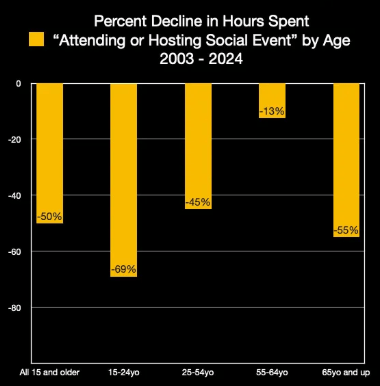

At the layer of sociology, the Enhanced Self is inseparable from the decline of socialization. While running clubs and morning workouts are booming, nightclubs are closing and parties are withering. Young Americans spend about 35 percent less time socializing and 70 percent less time attending or hosting parties than they did at the beginning of the century.

The age of the Enhanced Self is different from health movements of the past, not only because many of its elements are distinctly of the 2020s, including peptide shots, social media, and biometric scanners, but also because it does not particularly seek to build anything outside of the self.

For a long time, abstinence was associated with religion or personal histories, such as addiction recovery or pregnancy. But in the new health culture, abstinence is not about faith or addiction; it is about bodily perfection. On health podcasts and videos, influencers and science communicators talk about alcohol’s association with sleep scores, skin clarity, energy levels, cardiometabolic biometrics, and executive function.

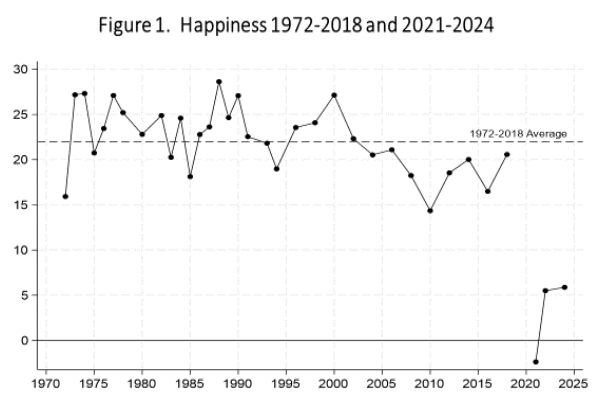

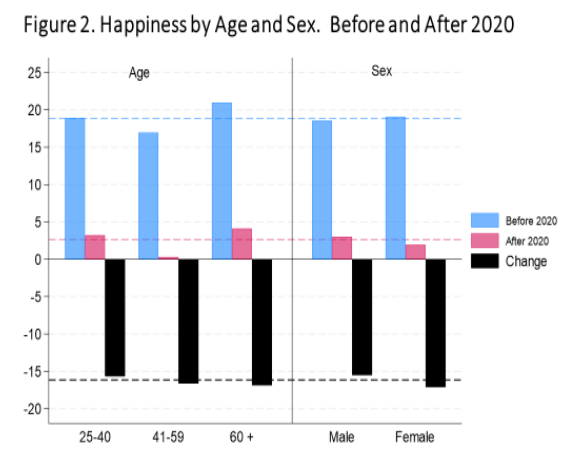

The fruits of the Enhanced Self movement will include fitter people, with less disease, who live longer lives. But what are the costs? Young people, who are seeing the highest increases in exercise time, also say they have fewer friends than any cohort ever; that they spend more time alone than any generation on record; and that they are more anxious and depressed than previous groups.

Our bodies want us to be social. Research finds that “super-agers” (individuals over 80 with the cognitive function of people decades younger) shared little in common except for an unusually robust history of friendship and other social connections. A 2025 analysis of 500,000 participants in the UK reported that living with a partner and frequently visiting family had roughly the same relationship with longevity as exercise.

While the pursuit of health does not have to cleave us away from others, the project of delaying mortality is often a solitary undertaking.

Adam Mastroianni notes that over the past few decades, high schoolers have steadily drunk less, smoked less, and fought less. In the same period, serial killers have all but vanished, blockbusters have grown less original, design has grown less distinctive, and cars have gone monochrome. Mastroianni ties these together with a theory he calls “the decline of deviance.” As people get richer and the world gets safer, deviance falls, because “life is worth more now.” When people think that they might live to be 100, the strategy for every life-game is the same: play it safe.

Bryan Johnson’s wellness company, book, and Netflix documentary are not called “Live Better” or even “Live Forever.” It’s called “Don’t Die.” The moment-by-moment obsession with death may extend our lives, but when we cannot stop practicing this lifespan arithmetic, many of us will slip out of the thick appreciation of the here and now and approach life with all the verve of a lonely risk-assessment officer at a life insurance firm.

___________________________

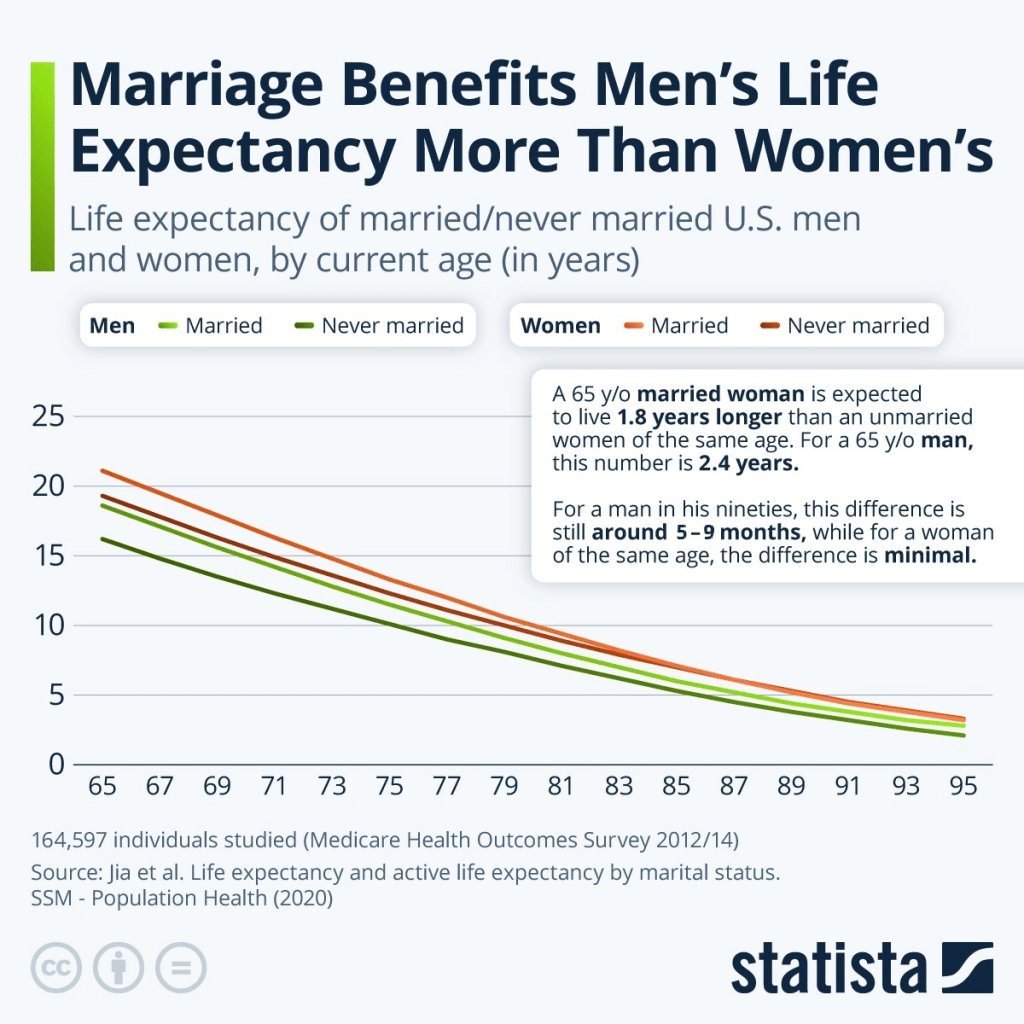

In general, women tend to live longer and healthier lives than men for a variety of reasons, including greater health consciousness and a tendency to avoid risky behaviors, but also genetic and hormonal factors. At 65 years old, U.S. women are expected to live for an additional 19 to 21 years, while for U.S. men, this number only stood at around 16 to 18.5 years.

However, married men aged 65 gain almost 2.5 years of life expectancy over their unmarried counterparts of the same age, boosting their outlook on life significantly. The role women play in marriages as planners and facilitators of medical care as well as advocates for healthy habits becomes clear when looking at divorced and widowed men’s life expectancy.

Married and never-married women, on the other hand, have a more similar expected lifespan. But even if a women is divorced or widowed, her life expectancy is still somewhat above that of a never-married woman, highlighting how women benefit from the overall advantages of marriage rather than just their spouse. These come in the form of so-called marriage protections, like adopting better habits, better mental health outcomes and better social connectedness. They are also often explained by so-called marriage selection, the idea that those individuals who manage to get married are already starting out with a better outlook on life.

Of course, this data depends on the quality of a marriage. A poor marriage has the opposite effect on lifespans due to increased stress and burdens.

____________________________

- Money doesn’t really change people. It magnifies what’s already there. Anxious people become more anxious. Generous people become philanthropists. Spenders ramp up spending on a never-ending hedonic treadmill of delights. Sibling disputes become expensive multi-year legal battles.

- The children of successful, wealthy families often internalize enormous pressure to excel and perform at high levels. They know they have no excuse to fail and every opportunity to succeed. They also learn that no one will ever extend them a lick of sympathy.

- Wealthy people aren’t better at managing money. They struggle to save; they get scammed; they don’t stick to a budget or know how much they spend. They have no special investing prowess.

- They still worry about money – about running out, about spoiling their kids, about making the wrong investments, about not making the most of it. Wealth does not alleviate money anxiety; in fact it can exacerbate it.

- They are very susceptible to peer pressure and groupthink. This applies to lifestyle choices and investing trends. The most popular conversations and think pieces were inevitably along the lines of “what our other clients are doing.”

- Rich people mostly own the same ETFs and index funds as the rest of us. There are no inside investing secrets. They don’t time the market or trade actively – if they listen to their advisors. Some love a flashy PE fund or venture capital stake to talk about on the golf course, but alternatives are generally more status flex than return enhancement.

- Wealthy parents worry unnecessarily about hammering a “strong work ethic” into their kids. Whether childhood is rough or smooth, some people develop it, and others just don’t. Similarly, some kids have a tendency to over-save, while others spend or give too much. This happens in poor and rich families alike.

____________________________

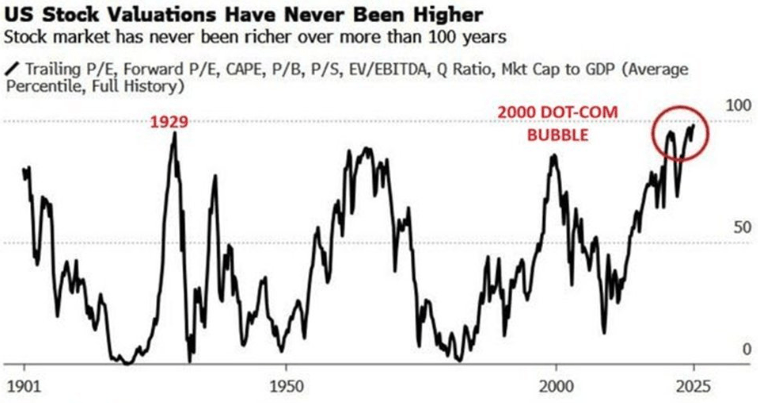

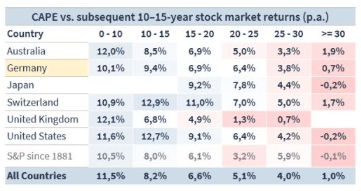

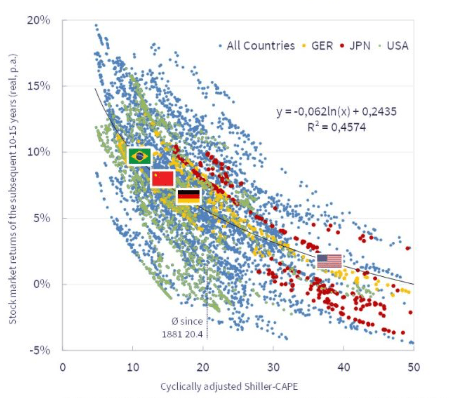

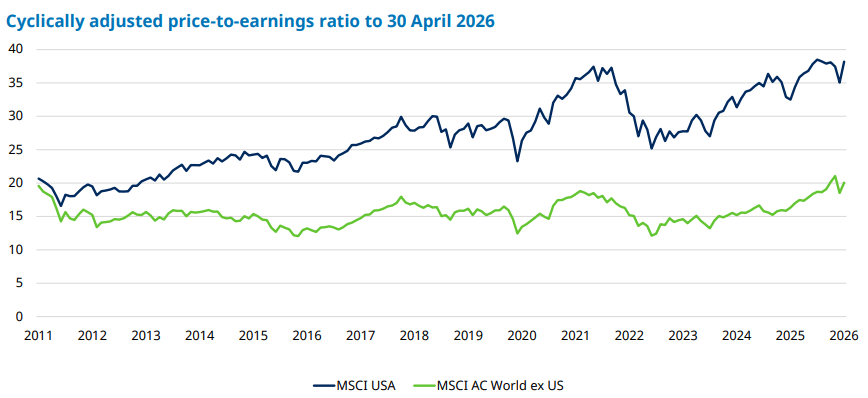

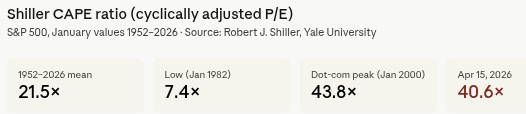

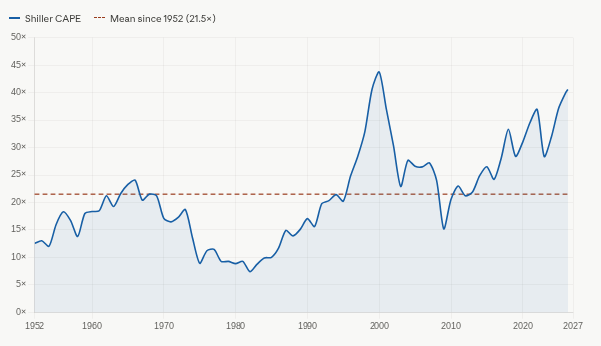

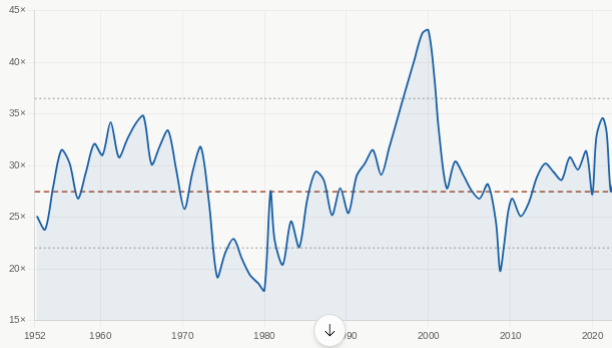

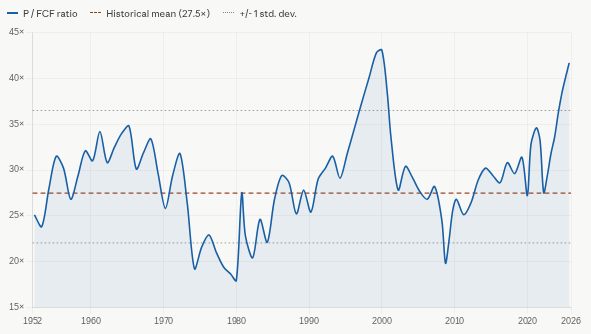

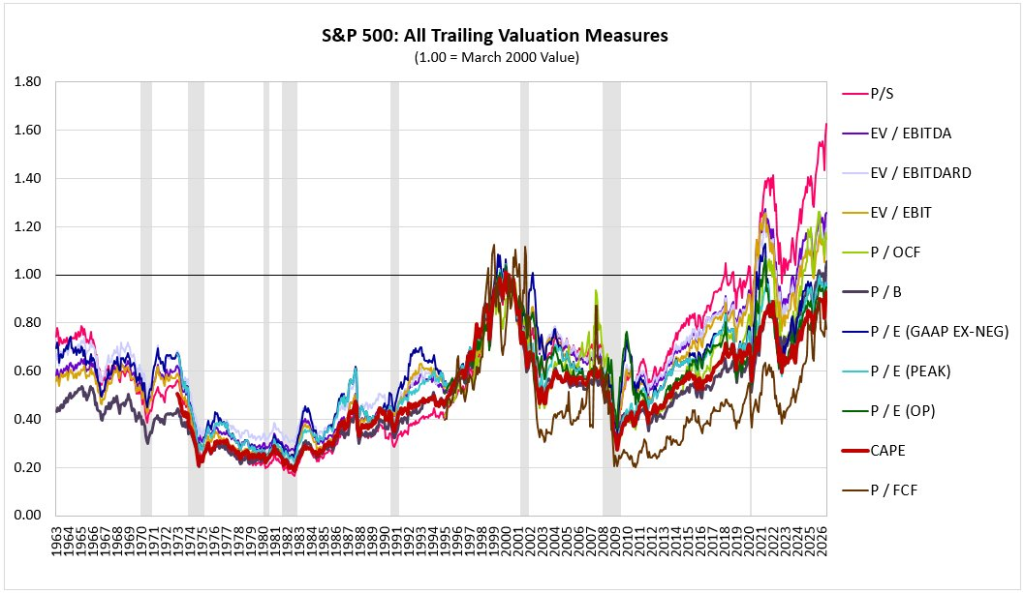

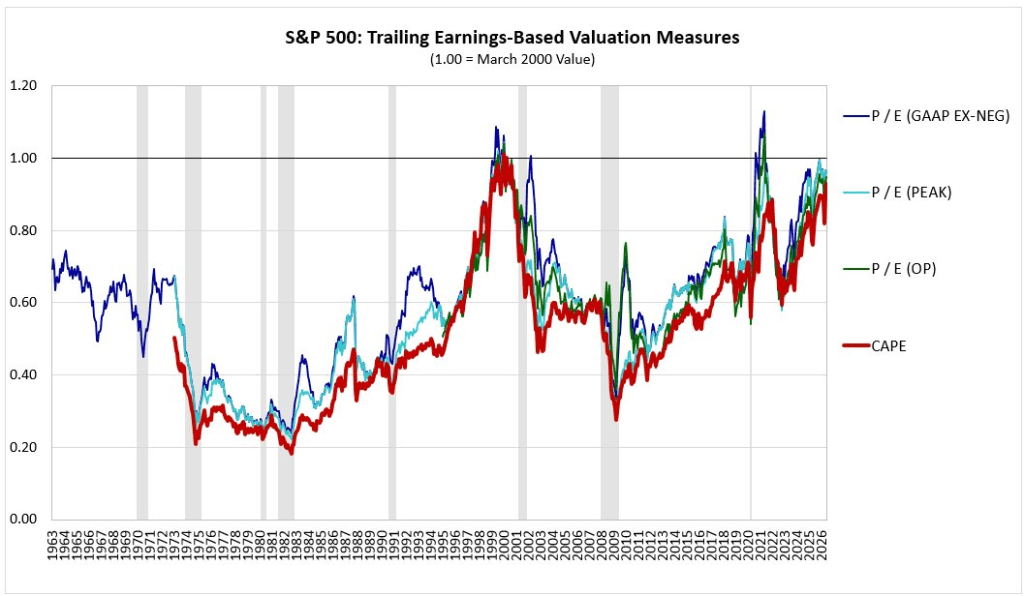

Almost every metric of U.S. stock valuations are at or above their 2000 bubble high peak:

____________________________

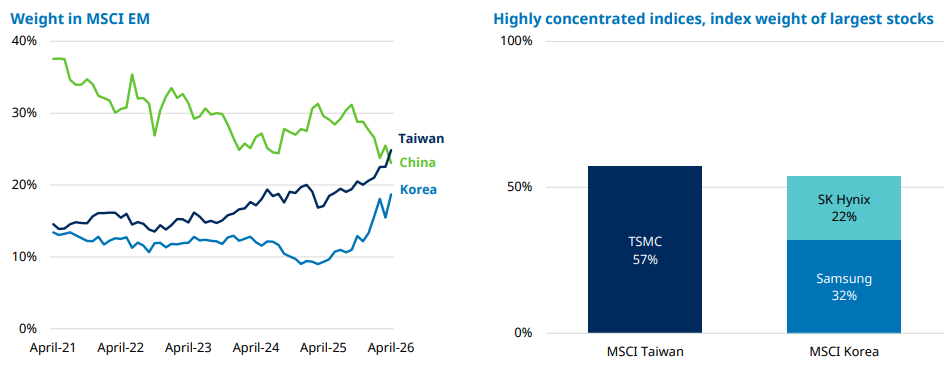

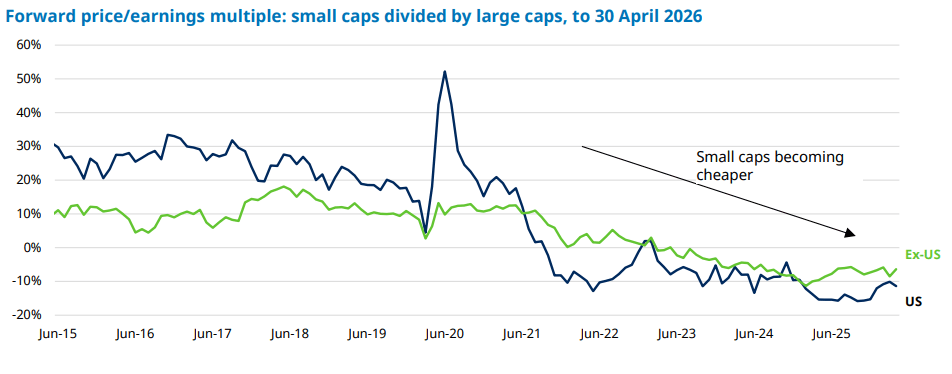

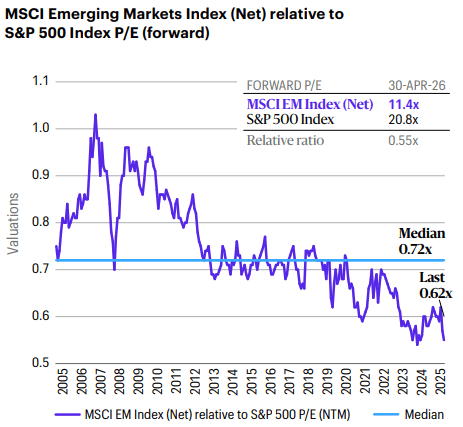

The price to earnings ratio of emerging market stocks were over 100% higher than U.S. stocks in 2006-2007. Today emerging market p/e ratios are almost 50% lower than the U.S.

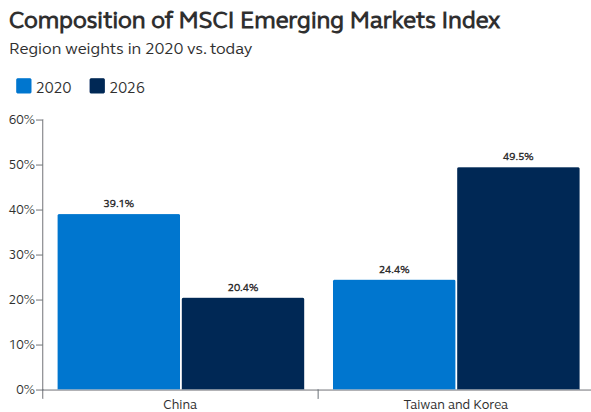

The MSCI Emerging Markets Index captures large and mid-cap representation across 24 emerging-markets countries, with roughly 1,200 constituents, and covers about 85% of the free-float-adjusted market capitalization in each country. The country roster includes places like China, India, Taiwan, South Korea, Brazil, Saudi Arabia, Mexico, and South Africa, among others.

It’s “free-float-adjusted market-cap weighted,” meaning constituents are weighted by the share value actually available to public investors, and larger companies carry more weight.

Korea and Taiwan now account for nearly half of the MSCI Emerging Markets Index, roughly double their 2020 weight, making the index increasingly sensitive to U.S. tech dynamics. As a result, EM equities have become more correlated with the U.S. AI cycle, diminishing their role as a portfolio diversifier.

_____________________

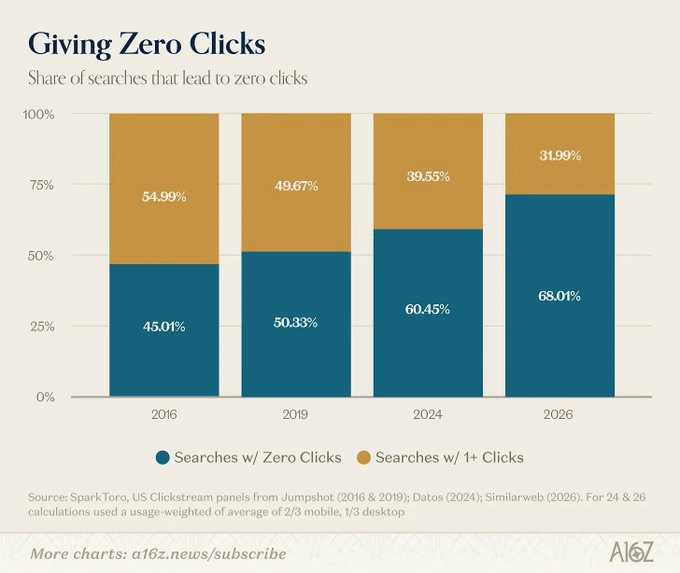

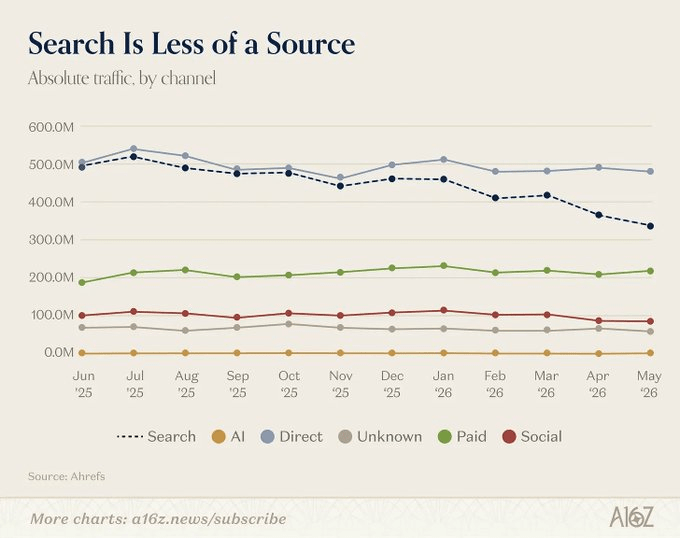

AI summaries are the likely driver of search’s decline as an online traffic source and the recent uptick in zero-click searches.

An increasing share of searches ends in no links being clicked.