In some ways I’m as productivity-obsessed as ever. What’s changed, and it’s a big change, is that I no longer take myself to be en route to some final state in which I’ll have discovered the best system, and can feel good about myself at last.

I’m convinced it’s a balm for much of what stresses us out: “the compulsion to closure,” which is the hope that all of this is leading up to some kind of permanent resolution. It isn’t. It’s better than that: you get to just be here, and do stuff.

The lack of resolution feels like a problem that needs solving. But have you considered the possibility that the only problem is your belief that such tensions might ever get resolved?

Living without hope of resolution is liberating because it removes a terrible weight from your actions and decisions – the weight that arises from the feeling that they must always be moving you toward some settled state. (Which often just leads to procrastination, since you’re unsure which action would be most helpful for getting you there.)

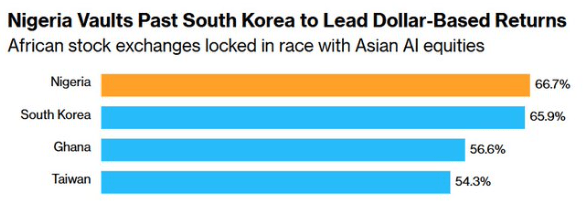

Nigeria now has the best performing stock market in the world, taking the lead over South Korea. As of the end of 2025, there were over 5,000 ETFs, mutual funds, and CEFs that focused on U.S. stocks. There used to be one ETF that invested in Nigerian stocks, but it closed back in 2023 because no one owned it.

__________________________________

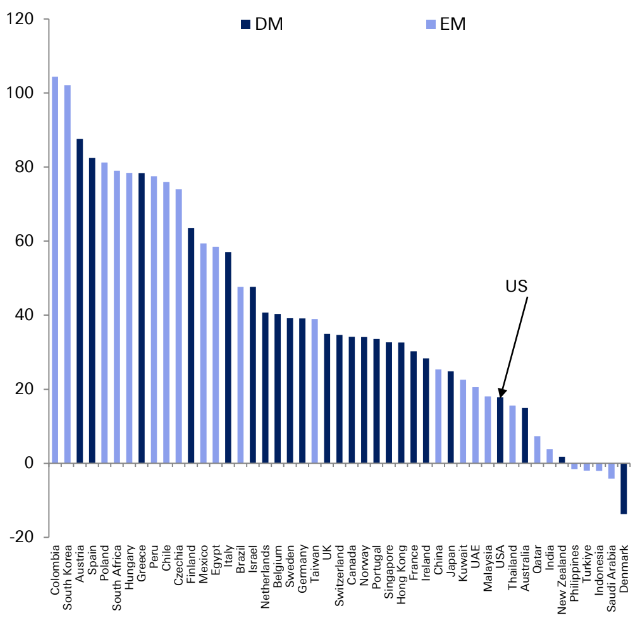

2025 Returns:

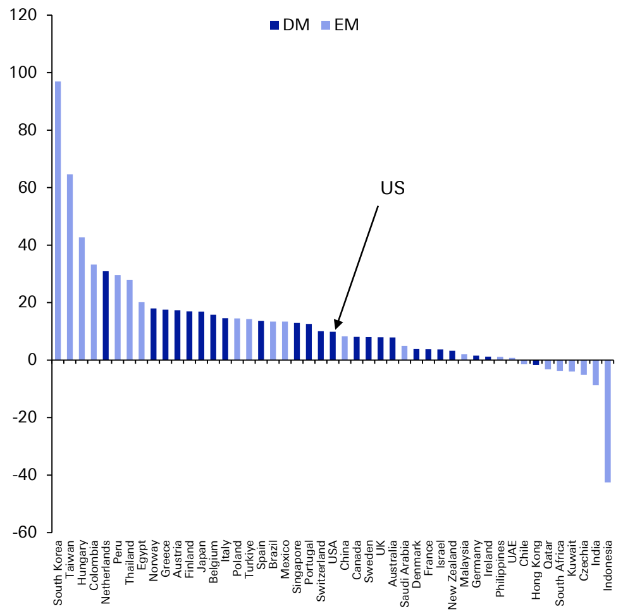

2026 Returns:

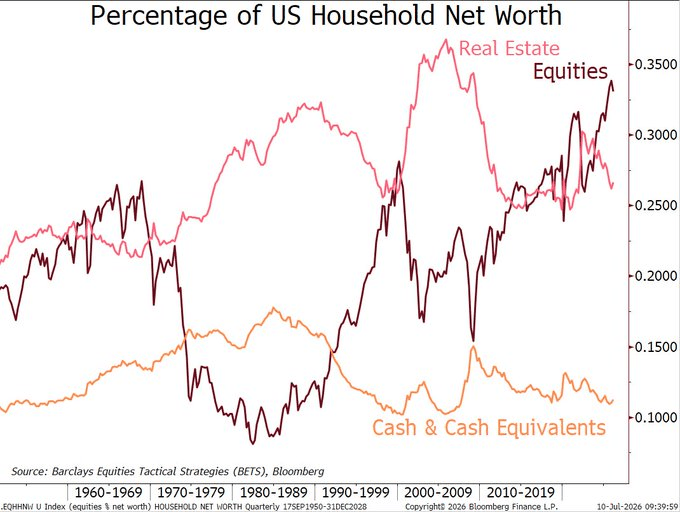

As U.S. stock prices continue to rise into the stratosphere, the percentage of U.S. household net work in stocks (equities) is higher than any point over the last 80 years.

The difference between forward earnings earnings (where analysts project S&P 500 stocks’ earnings will be a year from now) and trailing earnings (what S&P 500 stocks’ earnings actually were over the last year), has rocketed up to record bullish extremes.

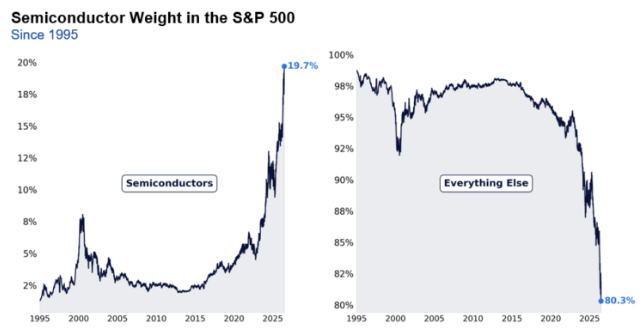

The defining story of the first half of 2026 was not a macro shock, it was the continued structural transformation of equity markets

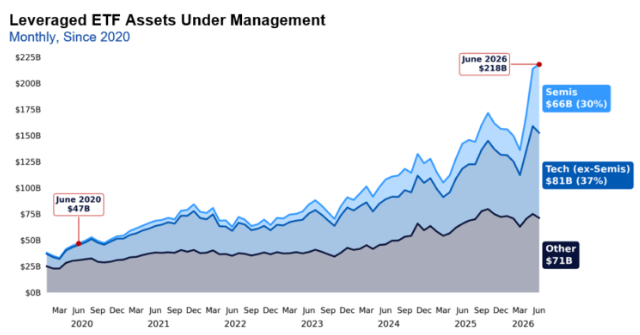

Market concentration remains near historic highs. Passive investing continues to absorb capital at unprecedented rates. Retail investors have become a persistent source of demand. Leverage has migrated toward increasingly short-dated and concentrated exposures. Together, these forces are reshaping liquidity, price discovery, and the behavior of volatility.

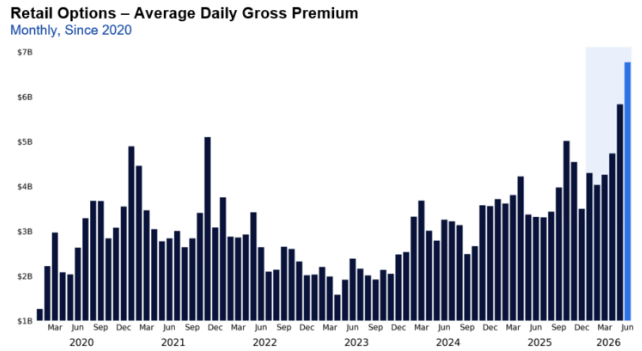

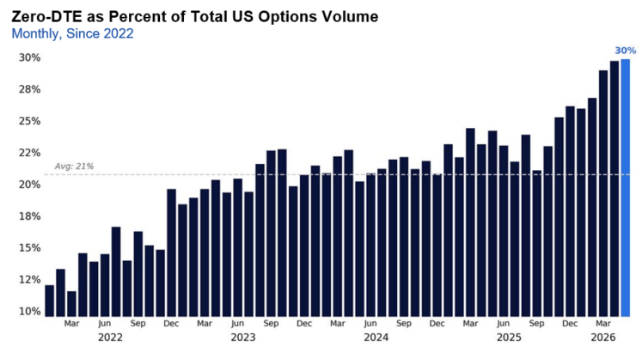

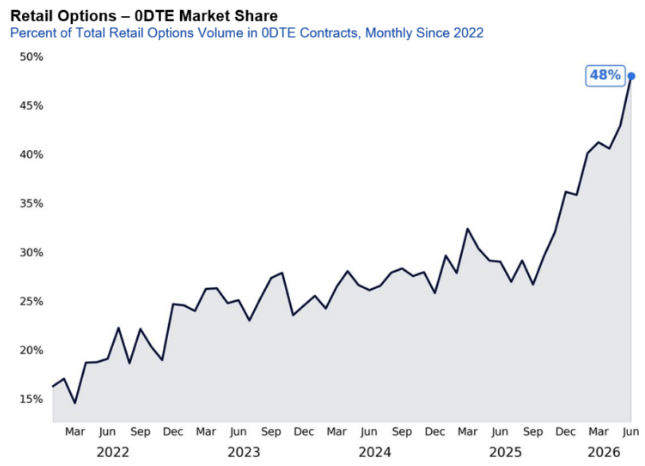

Retail investors have poured into stock options in 2026:

Unlike previous periods of elevated retail activity, today’s retail investor is increasingly concentrated in the same sectors driving benchmark performance, led by semiconductors and broad-based ETFs.

In June alone, retail traded approximately $1.9 billion of semiconductor options premium per day (6x the historical average) with about 75% of that activity concentrated in call options.

One out of every three listed options traded in the US now expires the same day, roughly doubling zero day options’ market share since daily expirations launched in 2022.

Following the introduction of Monday and Wednesday expirations in single stocks at the beginning of this year, nearly half of all retail options volume executed by Citadel Securities now trades in zero day contracts, up from 30% in 2025 and just 13% in 2021. Average time to expiry on Citade’s platform is less than 3 days.

Investors chase what’s hot (semis and tech) with leveraged ETFs:

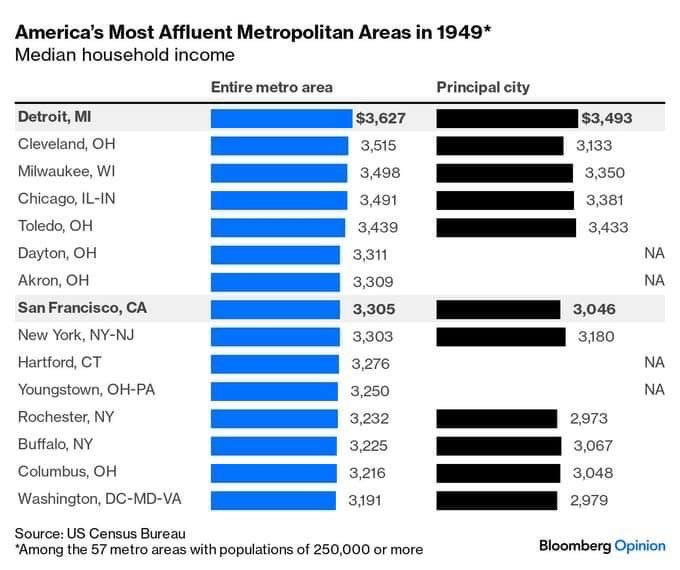

In 1949, four of America’s seven richest metro areas were in Ohio. Cleveland, Toledo, Dayton and Akron were out-earning New York, San Francisco and DC.

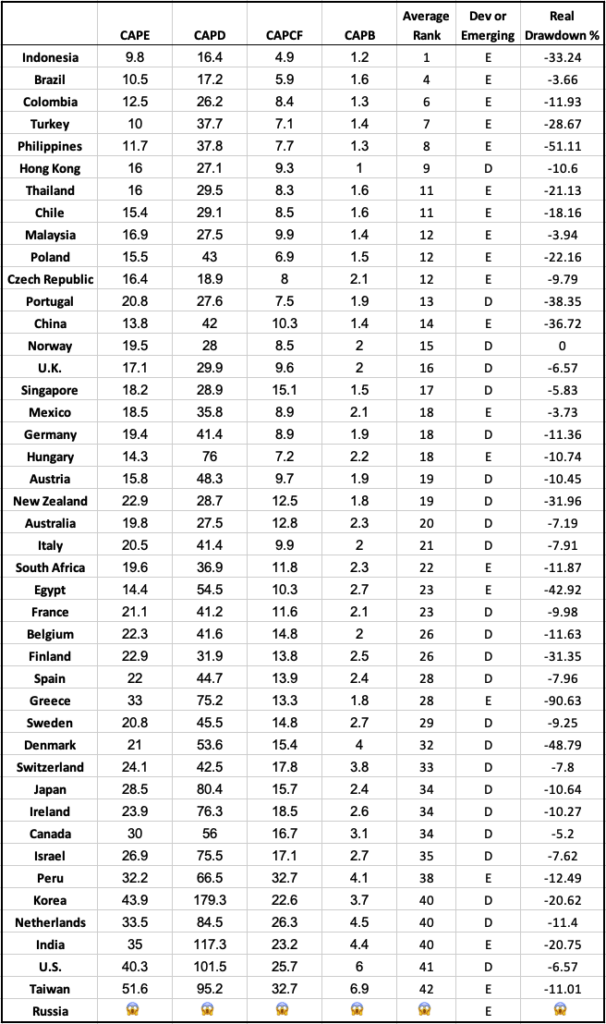

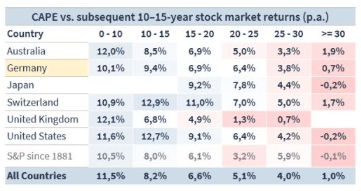

A higher price to earnings ratio (CAPE) means a country’s stock market is more expensive. A lower number is less expensive.

United States Stock Market: 40

Average of Foreign Developed Stock Markets: 24

Average of Foreign Emerging Stock Markets: 19

The rankings below show the price you are paying for the earnings, dividends, cash flow and book value for the companies within these countries.

*Abbreviations:

CAPE: Cyclically Adjusted Price Earnings – a valuation measure that uses real earnings per share (EPS) over a 10-year period to smooth out fluctuations in corporate profits that occur over different periods of a business cycle.

CAPD: Cyclically Adjusted Price Dividends – a valuation measure that uses dividends over a 10-year period to smooth out fluctuations in corporate profits that occur over different periods of a business cycle.

CAPCF: Cyclically Adjusted Price Cash Flow – a valuation measure that uses cash flow over a 10-year period to smooth out fluctuations in corporate profits that occur over different periods of a business cycle.

CAPB: Cyclically Adjusted Price Book – a valuation measure that uses book value over a 10-year period to smooth out fluctuations in corporate profits that occur over different periods of a business cycle.

Michael Cancelleri, an entrepreneur in San Clemente, Calif., has poured tens of thousands of dollars into his son’s baseball career—club team fees, tournament travel and top-of-the-line equipment. As high school approached, Cancelleri decided that wasn’t enough. He paid about $20,000 for his son, a straight-A student, to repeat a grade at a private middle school sports academy.

Sixty other boys are repeating a grade at the same academy, The Togethership, where coursework includes throwing mechanics, game film review and nutrition along with traditional subjects such as Algebra and English. Holding kids back in school for an athletic edge has existed for decades on the elite fringe of prep sports. In recent years, it has exploded in popularity for middle school boys.

Fueled by the lure of Name, Image and Likeness money in college, families are delaying high school so their sons can get bigger, stronger and more recruitable. The practice, known as “reclassifying,” “reclassing,” “bridge year” or “gap year,” is spreading fast in football, basketball, baseball, lacrosse and other sports where height and strength are key.

In his videos, George Makihara appears to have a lucrative side hustle making bets on Polymarket. In January, the college student posted a video that showed him winning $100,000 on a wager that President Trump would publicly say the word “McDonald’s” that month.

The bet was one of 145 that Makihara appeared to place on Polymarket’s website between January and mid-May, based on his videos—bets adding up to almost $410,000. But none of those bets were real, according to a Wall Street Journal investigation.

Makihara is one of dozens of mostly college-age creators Polymarket paid to film themselves making fake trades and sometimes scoring fake wins, according to an analysis of more than 1,100 videos by the Journal, along with instructional materials and interviews with creators who have worked with the company. On Polymarket’s actual site, more than 50 accounts made the McDonald’s bet in January, public data shows. All of them lost.

In its push to draw users to its unregulated platform, Polymarket has flooded social media with videos like Makihara’s, which appear genuine at first glance. In reality, Polymarket built near-perfect copies of its website, then instructed creators to make simulated trades on those dummy sites and hide that they were being paid by Polymarket. To get the videos to go viral, Polymarket has recruited a social-media army to copy and re-post creators’ footage.

______________________________

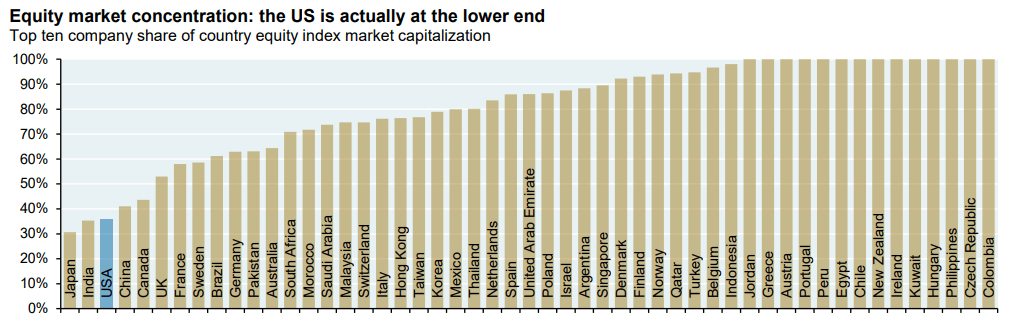

As recently as 2015 the 10 largest US stocks represented just 17% of the S&P 500 market cap. That was also the level that prevailed during the mid-1990’s. Now this figure has risen to about 40%.

However, relative to the rest of the world, the US has one of the lowest concentrations for its top 10 largest stocks:

__________________________

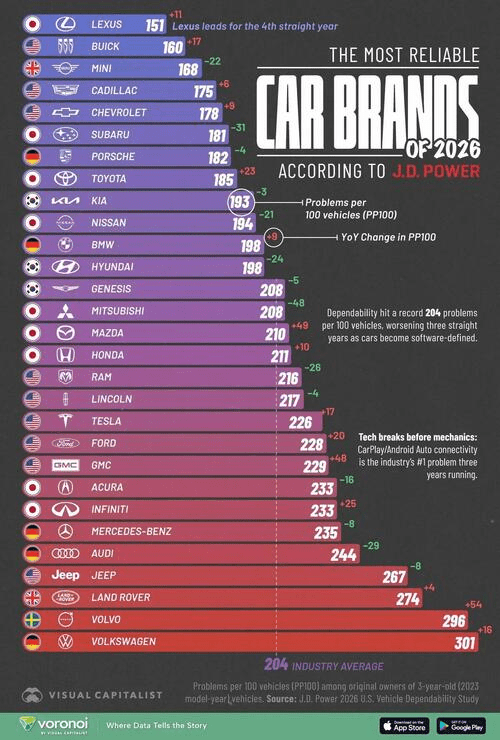

This graphic ranks the car brands with the fewest reported problems in 2026 based on J.D. Power’s Problems Per 100 Vehicles metric. Lower scores indicate fewer owner-reported issues and better long-term dependability.

Half of U.S. millennials have at least one tattoo.

The state of Wyoming only has 2 escalators.

Being born blind completely abolishes the risk of developing schizophrenia.

Why do women’s shirts button from the left, while men’s button from the right? When buttons first appeared in the 17th century, they were only for the wealthy. Women were dressed by (right-handed) servants. Placing buttons on the left made it easier for them.

There’s a hedge fund that buys and sells Hermes Birkin and Kelly bags on the secondary market and makes a 40.6% return with plans to grow in 2026.

If Paul Revere took his midnight ride this year, he could stop at 7 Dunkin locations.

LeBron James has played against over 35% of all players in NBA history.

Erik Spoelstra is now the most tenured coach across the four major sports leagues (NBA, NFL, MLB, NHL). He was hired in 2008.

Only 15% of Generation Alpha, the incoming cohort of teens, enjoys watching sports.

The second fastest growing sector in America in terms of GDP growth from 2019-2024 was gambling. In 2017, Americans legally bet $4.9 billion on sports. In 2025, it was over $160 billion.

40% of Americans did not read a single book in 2025.

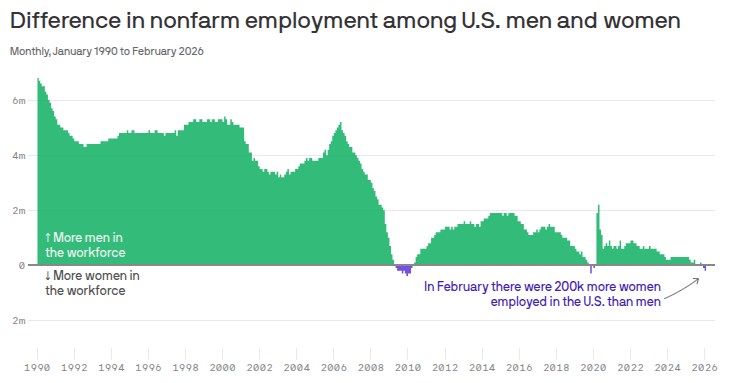

For only the third time ever, there are more women employed in the U.S. than men.

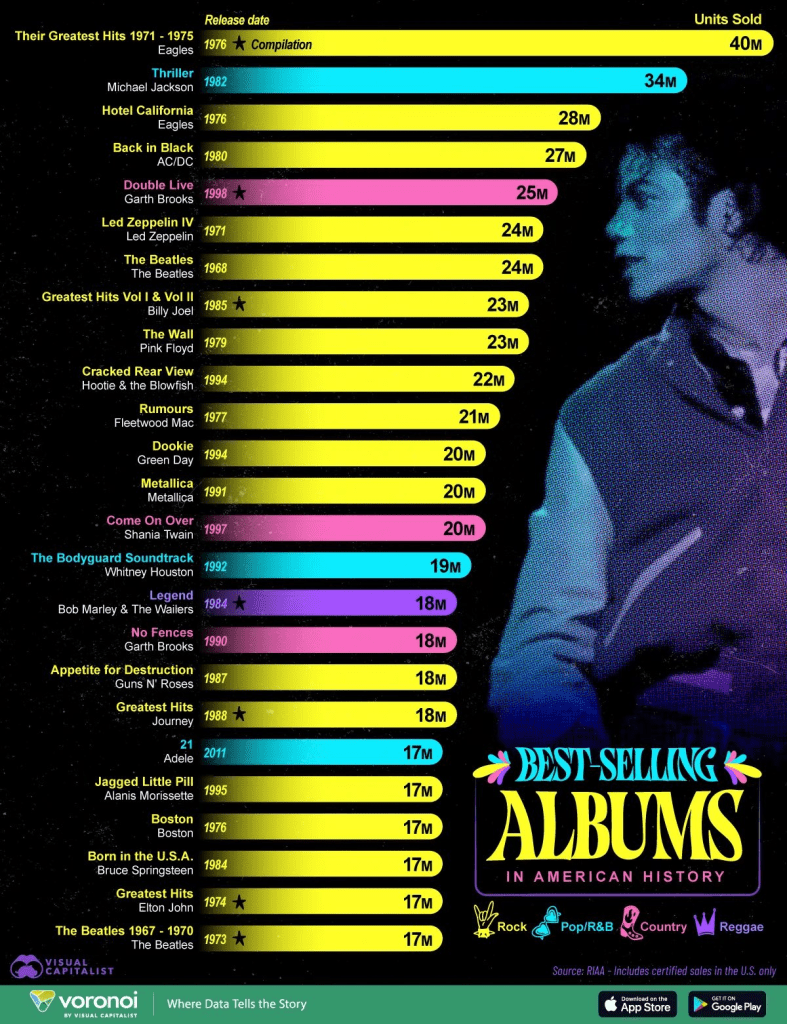

The Eagles have the highest selling album of all time.

At its best, having an Oura ring makes you fitter, happier, and, sure, even more productive. You may walk more, lift more, sleep more, and drink less. You will be hard-pressed to find a physician who thinks there’s anything amiss in the previous sentence.

However, the obsession with winning the measurable games of health can encroach on the less measurable games of life. The best way to sleep more is to see fewer friends in the evening. The best way to lift more during the week is to eliminate social lunches to protect your midday gym time. To become a measurably enhanced self often means eliminating your less quantifiable sources of meaning and happiness.

The ring can improve your life. But its form of self-improvement often pulls you away from other people. This left me with a nagging question. At what point is it unhealthy for me—for anyone, for all of us—to be this obsessed with health?

The share of people who drink hit an all-time low last year, according to Gallup, whose data go back to 1939. While many social changes happen slowly, the attitude shift against alcohol has been quite sudden. The decline of drinking is one part of a larger cultural phenomenon, the rise of the Enhanced Self.

The Enhanced Self is the evolution of medicine, technology, and consumer culture from an emphasis on curing illness to an obsession with optimizing normal, healthy life. We see this with the rise of GLP-1s, the explosion in biohacking with peptides, and the continued growth of supplements.

More Americans are using therapies not only to cure what is wrong with them but also to improve what is not wrong with them. At the layer of leisure, the tendrils of the Enhanced Self touch the white-hot rise of fitness in American life.

At the layer of biology, the Enhanced Self incorporates the belief that the human body is akin to a single-issue hardware device, whose owner should obsessively seek to extend its operating life beyond its scheduled date of obsolescence through relentless work and eagle-eyed neuroticism.

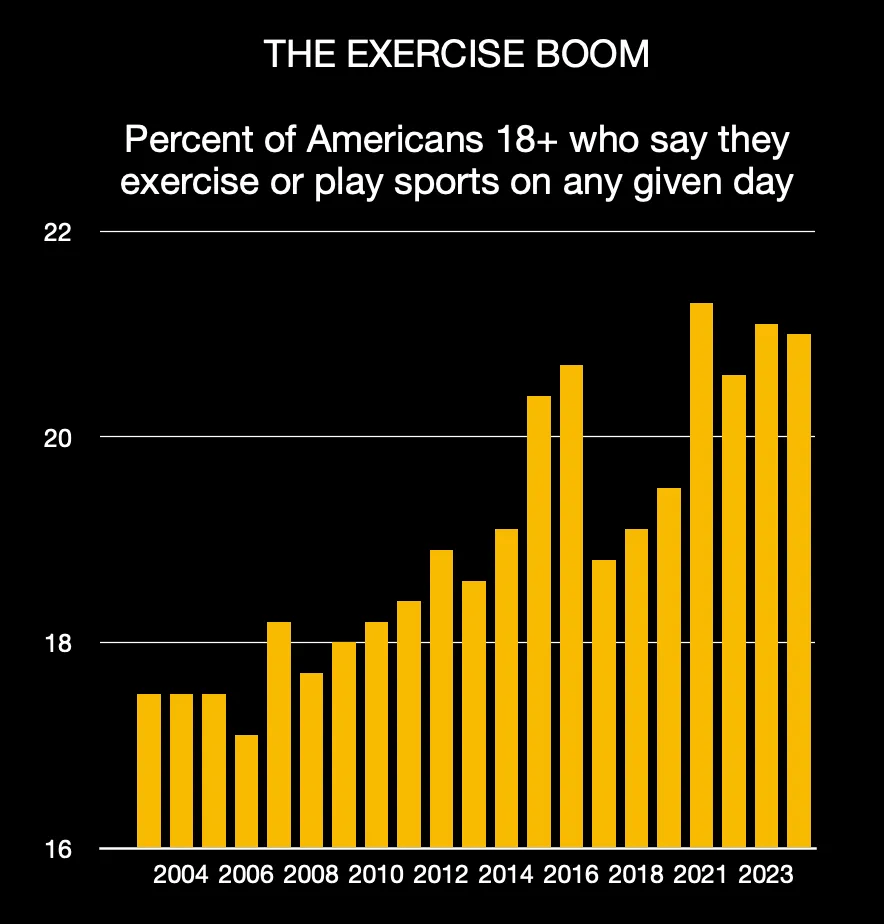

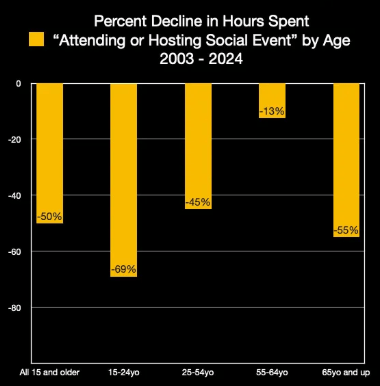

At the layer of sociology, the Enhanced Self is inseparable from the decline of socialization. While running clubs and morning workouts are booming, nightclubs are closing and parties are withering. Young Americans spend about 35 percent less time socializing and 70 percent less time attending or hosting parties than they did at the beginning of the century.

The age of the Enhanced Self is different from health movements of the past, not only because many of its elements are distinctly of the 2020s, including peptide shots, social media, and biometric scanners, but also because it does not particularly seek to build anything outside of the self.

For a long time, abstinence was associated with religion or personal histories, such as addiction recovery or pregnancy. But in the new health culture, abstinence is not about faith or addiction; it is about bodily perfection. On health podcasts and videos, influencers and science communicators talk about alcohol’s association with sleep scores, skin clarity, energy levels, cardiometabolic biometrics, and executive function.

The fruits of the Enhanced Self movement will include fitter people, with less disease, who live longer lives. But what are the costs? Young people, who are seeing the highest increases in exercise time, also say they have fewer friends than any cohort ever; that they spend more time alone than any generation on record; and that they are more anxious and depressed than previous groups.

Our bodies want us to be social. Research finds that “super-agers” (individuals over 80 with the cognitive function of people decades younger) shared little in common except for an unusually robust history of friendship and other social connections. A 2025 analysis of 500,000 participants in the UK reported that living with a partner and frequently visiting family had roughly the same relationship with longevity as exercise.

While the pursuit of health does not have to cleave us away from others, the project of delaying mortality is often a solitary undertaking.

Adam Mastroianni notes that over the past few decades, high schoolers have steadily drunk less, smoked less, and fought less. In the same period, serial killers have all but vanished, blockbusters have grown less original, design has grown less distinctive, and cars have gone monochrome. Mastroianni ties these together with a theory he calls “the decline of deviance.” As people get richer and the world gets safer, deviance falls, because “life is worth more now.” When people think that they might live to be 100, the strategy for every life-game is the same: play it safe.

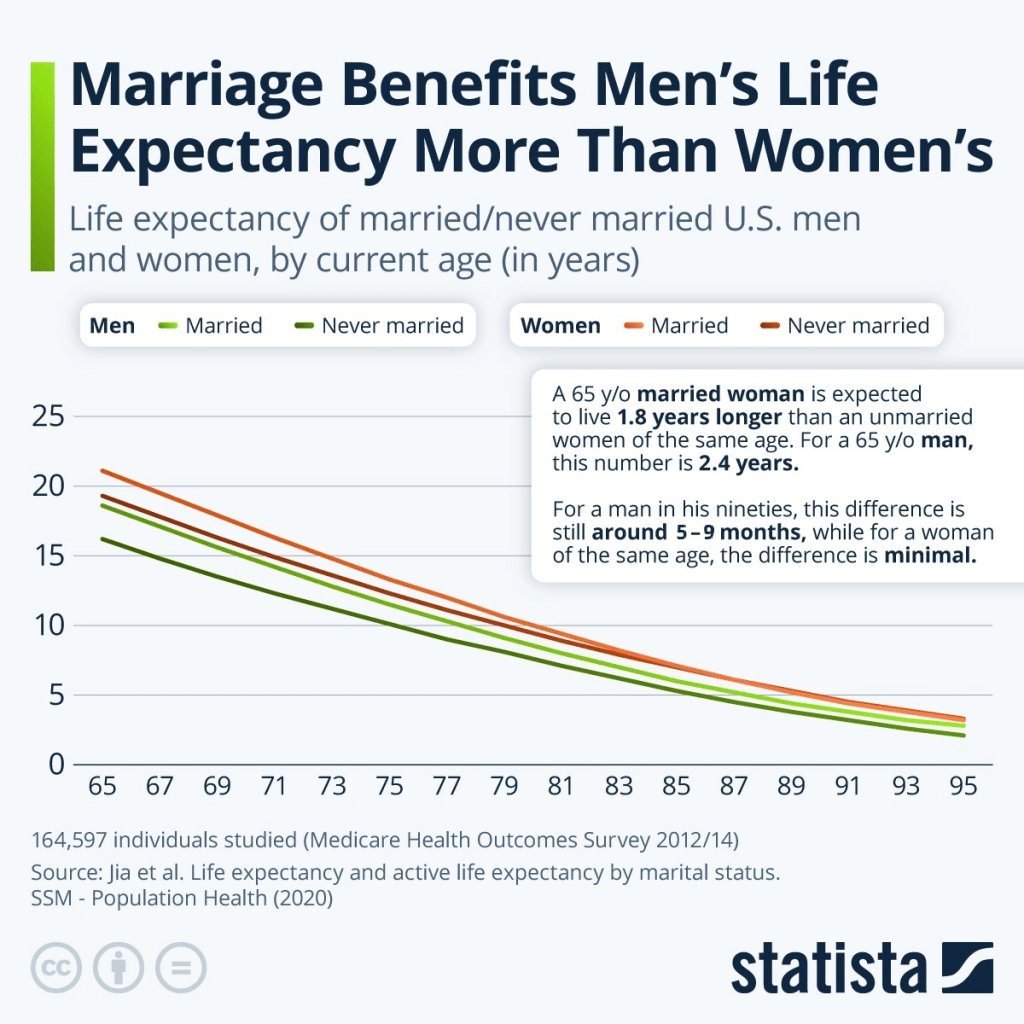

In general, women tend to live longer and healthier lives than men for a variety of reasons, including greater health consciousness and a tendency to avoid risky behaviors, but also genetic and hormonal factors. At 65 years old, U.S. women are expected to live for an additional 19 to 21 years, while for U.S. men, this number only stood at around 16 to 18.5 years.

However, married men aged 65 gain almost 2.5 years of life expectancy over their unmarried counterparts of the same age, boosting their outlook on life significantly. The role women play in marriages as planners and facilitators of medical care as well as advocates for healthy habits becomes clear when looking at divorced and widowed men’s life expectancy.

Married and never-married women, on the other hand, have a more similar expected lifespan. But even if a women is divorced or widowed, her life expectancy is still somewhat above that of a never-married woman, highlighting how women benefit from the overall advantages of marriage rather than just their spouse. These come in the form of so-called marriage protections, like adopting better habits, better mental health outcomes and better social connectedness. They are also often explained by so-called marriage selection, the idea that those individuals who manage to get married are already starting out with a better outlook on life.

Money doesn’t really change people. It magnifies what’s already there. Anxious people become more anxious. Generous people become philanthropists. Spenders ramp up spending on a never-ending hedonic treadmill of delights. Sibling disputes become expensive multi-year legal battles.

The children of successful, wealthy families often internalize enormous pressure to excel and perform at high levels. They know they have no excuse to fail and every opportunity to succeed. They also learn that no one will ever extend them a lick of sympathy.

Wealthy people aren’t better at managing money. They struggle to save; they get scammed; they don’t stick to a budget or know how much they spend. They have no special investing prowess.

They still worry about money – about running out, about spoiling their kids, about making the wrong investments, about not making the most of it. Wealth does not alleviate money anxiety; in fact it can exacerbate it.

They are very susceptible to peer pressure and groupthink. This applies to lifestyle choices and investing trends. The most popular conversations and think pieces were inevitably along the lines of “what our other clients are doing.”

Rich people mostly own the same ETFs and index funds as the rest of us. There are no inside investing secrets. They don’t time the market or trade actively – if they listen to their advisors. Some love a flashy PE fund or venture capital stake to talk about on the golf course, but alternatives are generally more status flex than return enhancement.

Wealthy parents worry unnecessarily about hammering a “strong work ethic” into their kids. Whether childhood is rough or smooth, some people develop it, and others just don’t. Similarly, some kids have a tendency to over-save, while others spend or give too much. This happens in poor and rich families alike.

____________________________

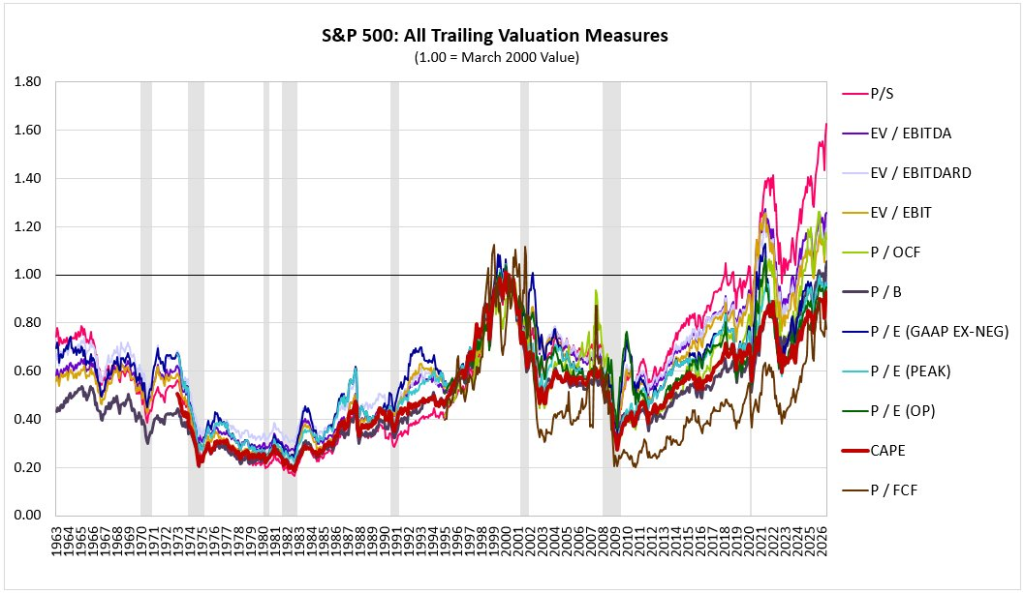

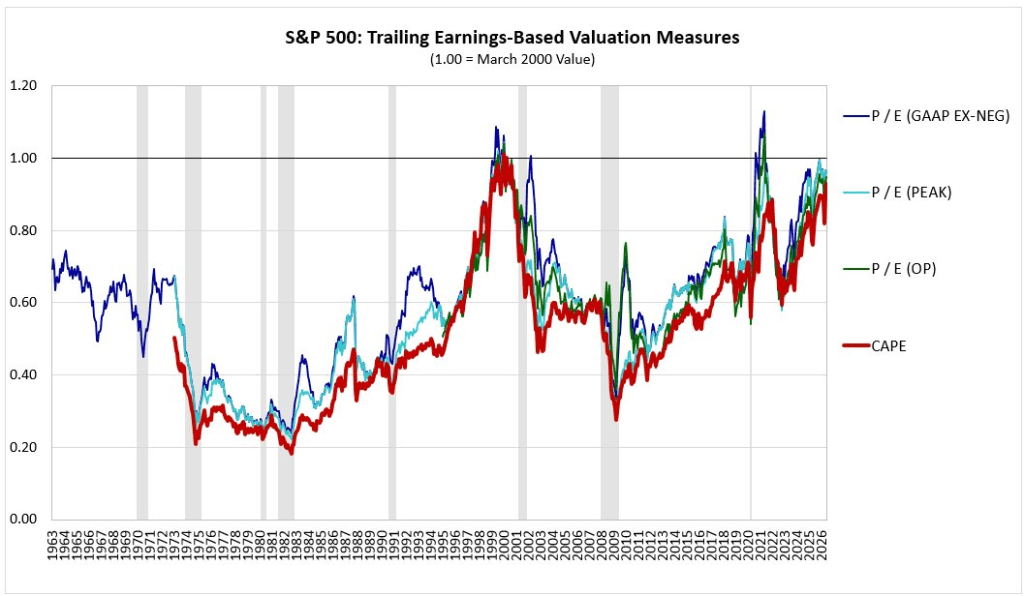

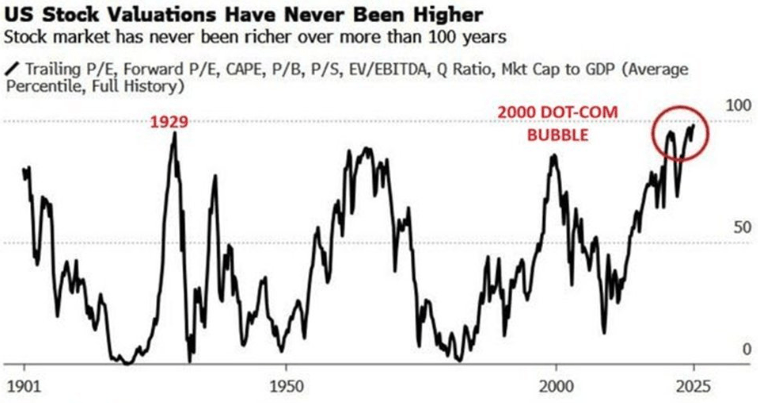

Almost every metric of U.S. stock valuations are at or above their 2000 bubble high peak:

____________________________

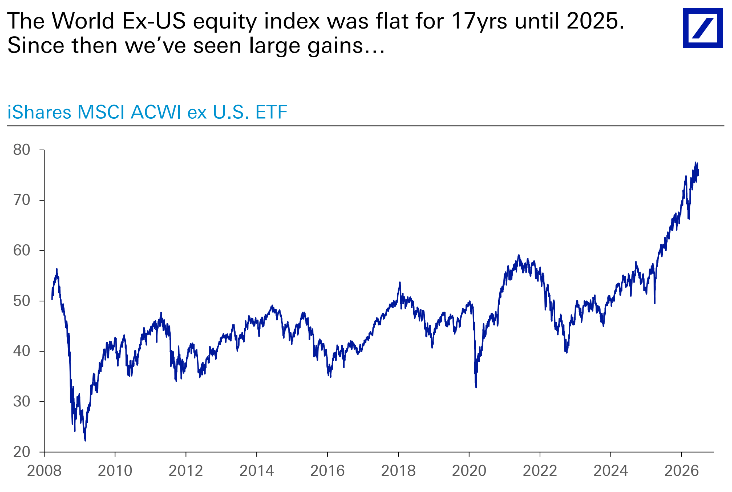

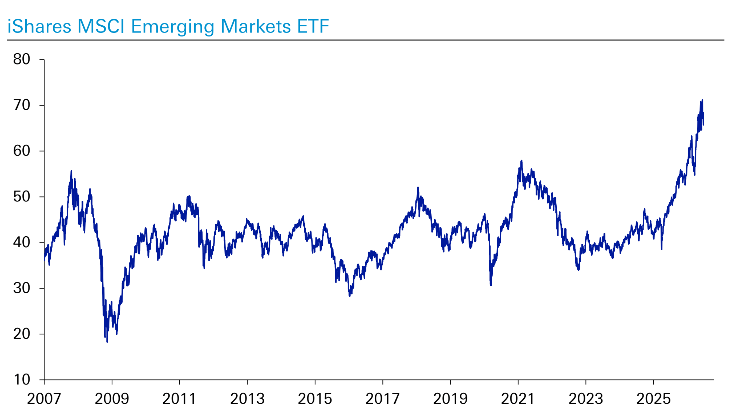

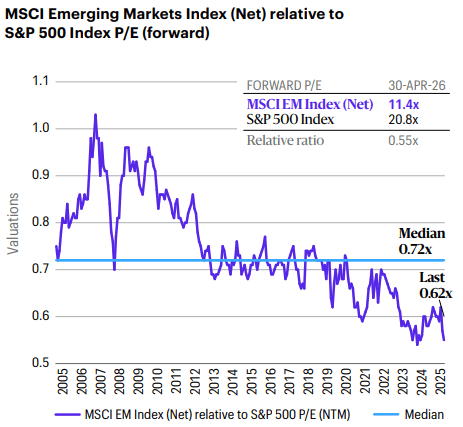

The price to earnings ratio of emerging market stocks were over 100% higher than U.S. stocks in 2006-2007. Today emerging market p/e ratios are almost 50% lower than the U.S.

The MSCI Emerging Markets Index captures large and mid-cap representation across 24 emerging-markets countries, with roughly 1,200 constituents, and covers about 85% of the free-float-adjusted market capitalization in each country. The country roster includes places like China, India, Taiwan, South Korea, Brazil, Saudi Arabia, Mexico, and South Africa, among others.

It’s “free-float-adjusted market-cap weighted,” meaning constituents are weighted by the share value actually available to public investors, and larger companies carry more weight.

It’s difficult to escape “temporal chauvinism,” which is the feeling that the time we’re living in now is the most significant or terrifying one ever, simply because it’s the one we happen to be around to experience.

Everything about our situation as humans pushes us to overrate the importance of our own era. Apart from anything else, present-day unknowns feel the scariest, because all previous unknowns eventually resolved themselves into knowns (every prior prediction of the end of the world turned out to be wrong) while future ones haven’t occurred to us yet.

It is very, very, very, very unlikely that the literal apocalypse is coming anytime soon. We’re almost certainly not living at the end of human civilization. Frankly, it’s pretty unlikely we’re even on the cusp of unprecedented levels of disruptive change. The truth is that we’re probably living through times that future historians will think of as broadly normal.

The point is not that life is safer and more secure than the heralds of the apocalypse would have us believe. It’s the opposite: that human existence is intrinsically unsafe and insecure, all the time. Anything could happen at any moment, the future is unknowable, one day you’ll die, and some people end up having vastly more traumatic encounters with these realities than others.

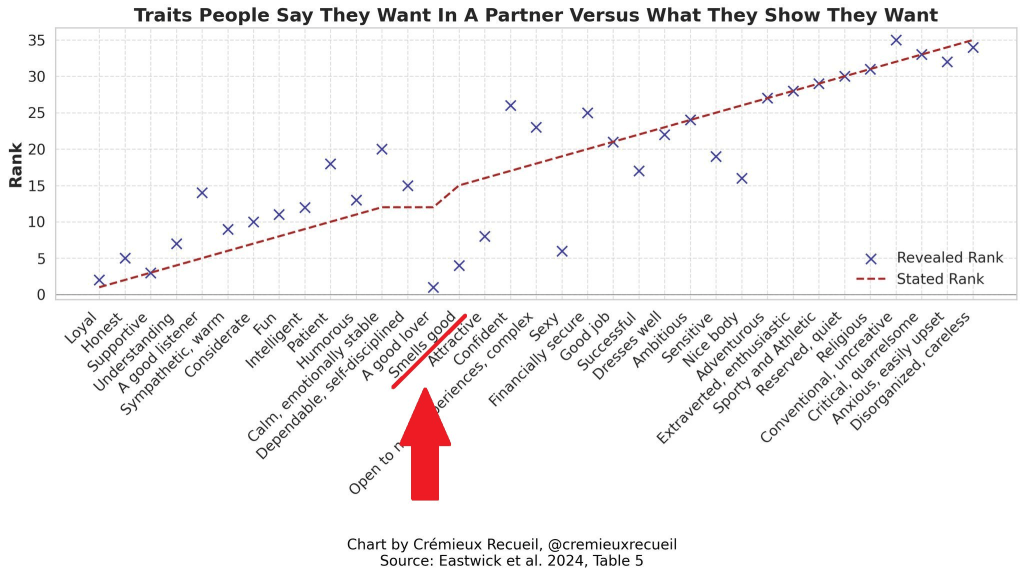

The graph below shows what people say they want or what is important to them in a partner (red line). The “X” marks show how much each trait correlated with people’s actual romantic evaluations or how important it was in real life.

The biggest discrepancies were in (1) being attractive, (2) being a good lover, (3) being sexy, (4) having a nice body, and (5) smelling good. Perhaps people are simpler than we realized once we look beyond surveys.

The discrepancies run the other way too. Being (1) a good listener, (2) patient, and (3) calm and emotionally stable were all overrated in stated preferences.

It’s a little confusing that the red line rises from left to right, suggesting increasing importance, but since these are rankings, a higher number actually means less important (1 = most important).

_________________________

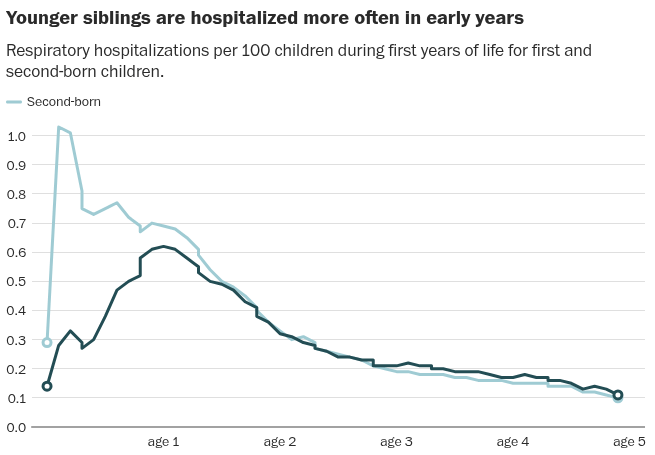

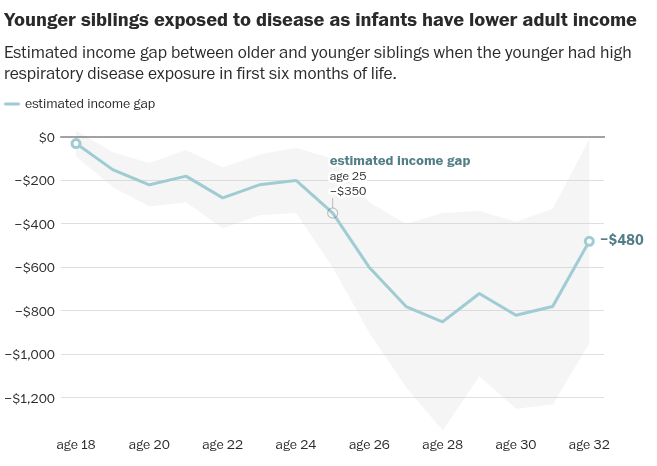

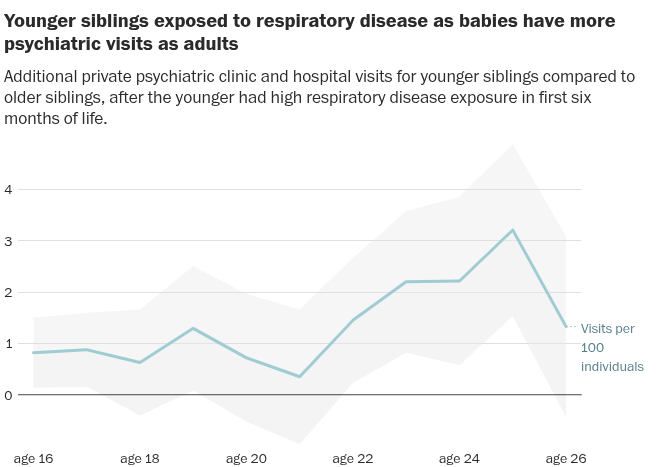

Research has consistently shown that younger siblings fare worse than firstborns on lifetime earnings, educational achievement, mental health and, for women, teen pregnancy. The later the birth order, the worse the stats get. Why?

(1) Less Quality Time with Parents

First-born children average 20 to 30 more quality minutes each day with parents compared with a second-born child of the same age. The deficit amounts to about 3,000 fewer hours spent on reading, playing, talking or other activities with at least one parent for younger siblings. That’s roughly comparable to more than a year of schooling between the ages of 4 and 13.

The gap only widens as more kids enter the picture. That means the youngest siblings get far less quality time overall because whatever is available gets split among more children.

(2) Germs

Studies find that the tiniest organisms have a profound impact on a child’s future. Exposure to respiratory viruses before a baby’s first birthday, when immune systems are immature and before most childhood vaccinations, consistently predict reduced earnings, education and health decades later.

Researchers estimate that half or more of the gap in life outcomes between older and younger siblings can be attributed to pathogens inadvertently brought home by older siblings.

The disparity is stark: Younger siblings are two to three times more likely to be hospitalized for acute respiratory conditions than their older siblings during their first year of life. After that, when younger children generally begin attending group child care, the hospitalization gap disappears. Older siblings, the data suggested, bring home viruses to vulnerable infants with no other significant sources of exposure.

To show that higher disease exposure causes harm later in life required more work for researchers. They had to control for parental income, education and employment across municipalities with higher and lower infection rates. Yet the pattern was clear: earnings, education and mental health outcomes all declined as community disease exposure rose.

In the first months of life, roughly 85 percent of an infant’s calorie intake goes toward neural development. A serious infection can reduce how much a baby eats and divert calories away building a brain. If a child is very ill during that time, it might impact brain development by diverting biological resources to fighting an illness.

Money is less of a factor in attraction than people think. What matters more is your ambition. The academic literature on evolutionary biology supports this. In a study across 37 cultures, evolutionary psychologist David Buss found that, on average, potential partners valued “ambition and industriousness” more than “good financial prospects” when choosing a mate.

In evolutionary terms, this is known as Resource Holding Potential (RHP), or your ability to acquire resources in the future. A husband signals high RHP while working, but signals low RHP if he retires early, gets high and plays video games with friends all day; even if he worked unbelievably hard to get to that point. Why is ambition more attractive than money?

Because money says, “I was useful,” while ambition says, “I am useful.”

People care about the future. People care about the genes they pass on to their offspring. And they want to pass on traits like industriousness because those traits will help their children acquire future resources, and so on. Having money makes you more attractive. But it’s not the money that’s actually appealing, only how you acquired it. The potential to collect more resources is the draw from potential mates.

A loser’s game is any game, contest, or activity in which the ultimate victor is determined by the actions of the loser. These contests are not won; they are lost.

In tennis, pros can be aggressive. They have the skill, precision, and experience to place shots just outside their opponent’s reach. They play a winner’s game. The match goes to the player who earns the most wins. Amateurs, however, often lose by trying to play like the pros, because it leads to unforced errors. It’s a loser’s game. Amateurs win in tennis by volleying until their opponent hits it into the net or out of bounds. They win by not losing.

There are two different games being played in the stock market. The game the experts play differs from the game the amateurs play. The game amateurs should play, and many experts too, is built on a foundation of avoiding errors. Essentially, not losing. Fewer errors lead to better results.

Luck

Every investor should recognize the powerful potential impact of luck — not good luck, but bad luck. We can all live through good luck. But bad luck — the apparently random occurrence of adversity — is equally prevalent, and its consequences can be far greater.

Getting Excitement Out of the Market

Go to a continuous-process factory sometime — a chemical plant, a cookie manufacturer, a place that makes toothpaste. Everything is perfectly repetitive, automated, exactly in place. If you find anything interesting, you’ve found something wrong.

Investing is a continuous process too; it isn’t supposed to be interesting. It’s a responsibility. If you go to the stock market because you want excitement, then sooner or later you will lose. Everyone who thinks the stock market is a game loses — everyone, to the last man, woman, and child. So, the purpose of an investment policy is simply to ensure that your continuous process never breaks down.

On Over-Confidence

A rapidly rising market makes you forget that those whom the gods would destroy, they first make confident. The more you know, the higher the odds that you’ll make a serious mistake. That’s why it’s not the beginners who tend to die at skydiving and why most car accidents happen within a few miles of home. There’s a saying in the British Royal Air Force that investors need to remember: “There are old pilots, and there are bold pilots, but there are no old, bold pilots.”

As human beings, particularly if we are successful in other parts of our lives, we are notoriously unable to accept the obvious reality that, on average, we are average, and that our normal experiences will usually be about average because we are, as a group, captives of the normal distribution of the bell curve. Studies all the time show we think we are above-average drivers, above-average parents — and above-average investors. And we do tend to take it personally when our stocks go way up or go way down, even though, as Adam Smith admonishes, “The stock doesn’t know you own it.”

________________________

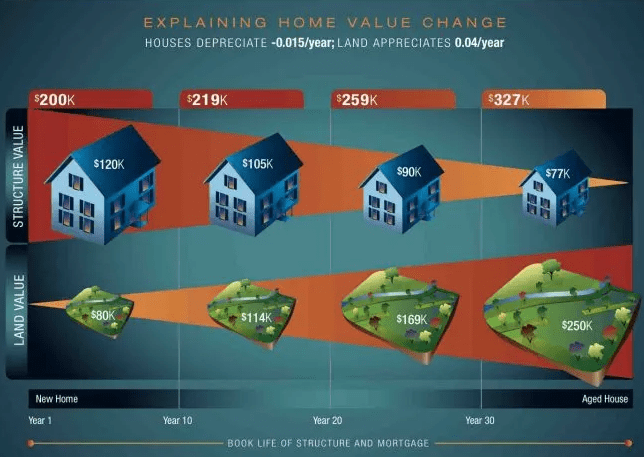

Land Appreciates. Homes Depreciate.

The value of a home (excluding land) declines over time unless it is updated to break even. Think of it in the context of not updating the home for 30 years, which makes the concept much easier to understand. The house will slowly fall apart. Meanwhile, in most housing markets, land values eventually rise over a 30-year period, and the cash-poor homeowner can sell for more than their original purchase price.

__________________________

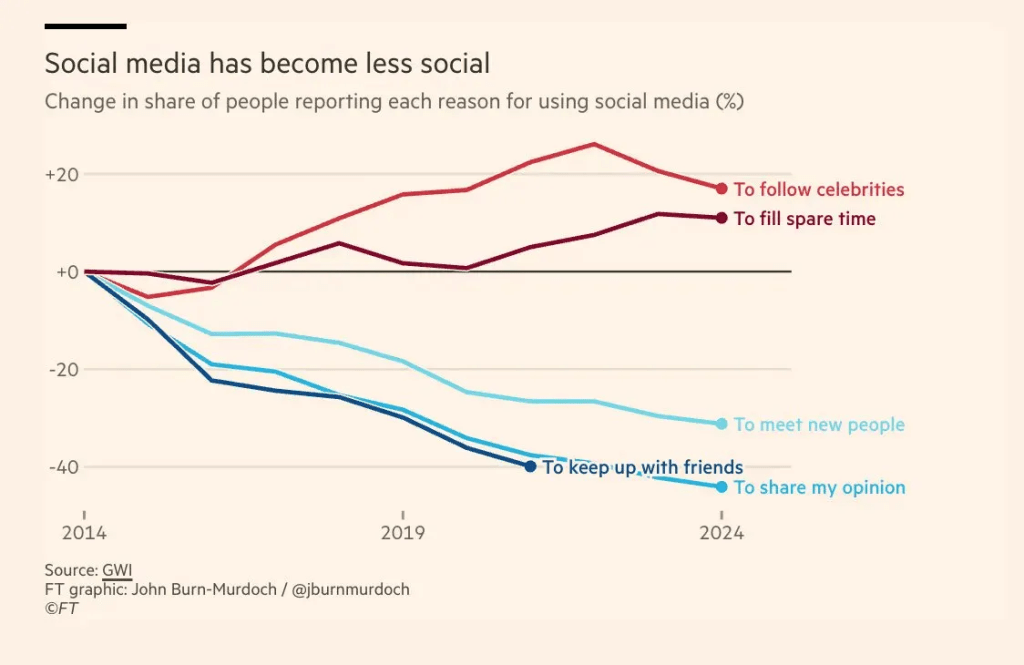

Social media has become less social.

__________________________

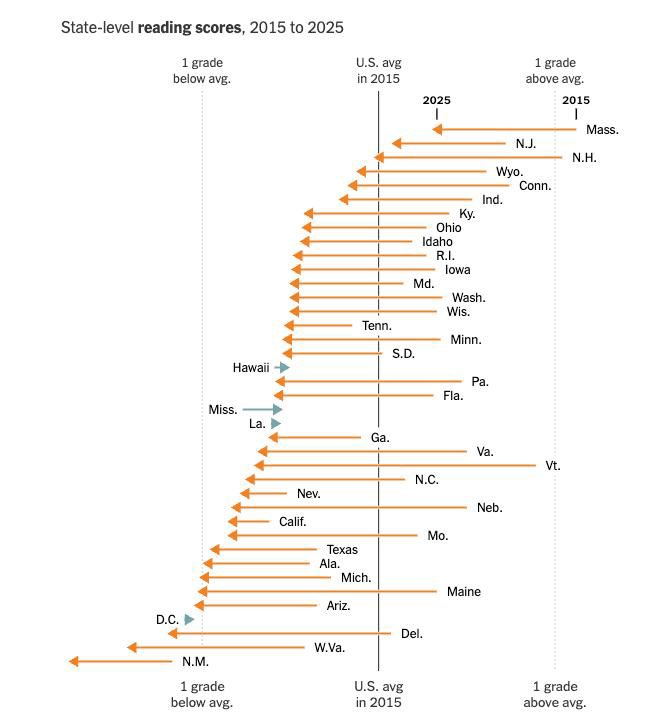

State level reading scores have dropped dramatically over the last 10 years.

__________________________

Based on an average the average of the valuation metrics below, the U.S. stock market has now become more expensive than both the 1929 and 2000 bubble peaks:

Trailing (P/E) Price to Earnings

Forward (P/E) Price To Earnings

Cyclically Adjusted Price To Earnings (CAPE)

Price to Book (P/B)

Price to Sales (P/S)

Enterprise Value (EV) to Earnings Before Interest Depreciation & Amortization (EBITA)

Market Value to Replacement Cost Of Physical Assets (Q Ratio)

Market Cap to GDP

_________________________________

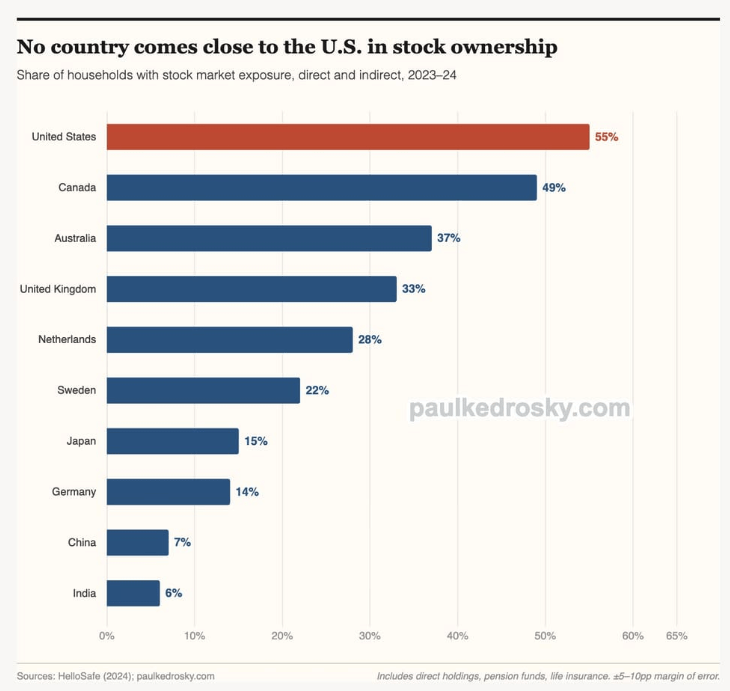

U.S. households are far more invested in stocks relative to the rest of the world:

Loneliness as we think about it today is a new phenomenon. In the past, people often talked about being alone, but there were lots of benefits to it : spiritual connection, getting to know yourself, emotion regulation. For most of human history, there was a sense that you were never truly alone; God was around, or you were one with nature. Our modern notion of loneliness is a 19th century concept that emerged as culture became more secular and more individualist.

In Robinson Crusoe, from the early 1800s, being stranded was a moment of spiritual enlightenment, a chance to find yourself. In Cast Away with Tom Hanks, the whole point is that Hanks went crazy because he had no one to talk to. There’s a real difference in what we think alone time does.

Psychologists have started asking whether our construal of loneliness is actually creating the feelings associated with it, and people talking about the loneliness crisis could be making them more lonely. Studies have been run where some people read a typical news article about the loneliness crisis and others read about the benefits of solitude. That simple intervention changes how people experience being alone. Your perception of how bad it is to be alone is making loneliness worse when you actually find yourself alone.

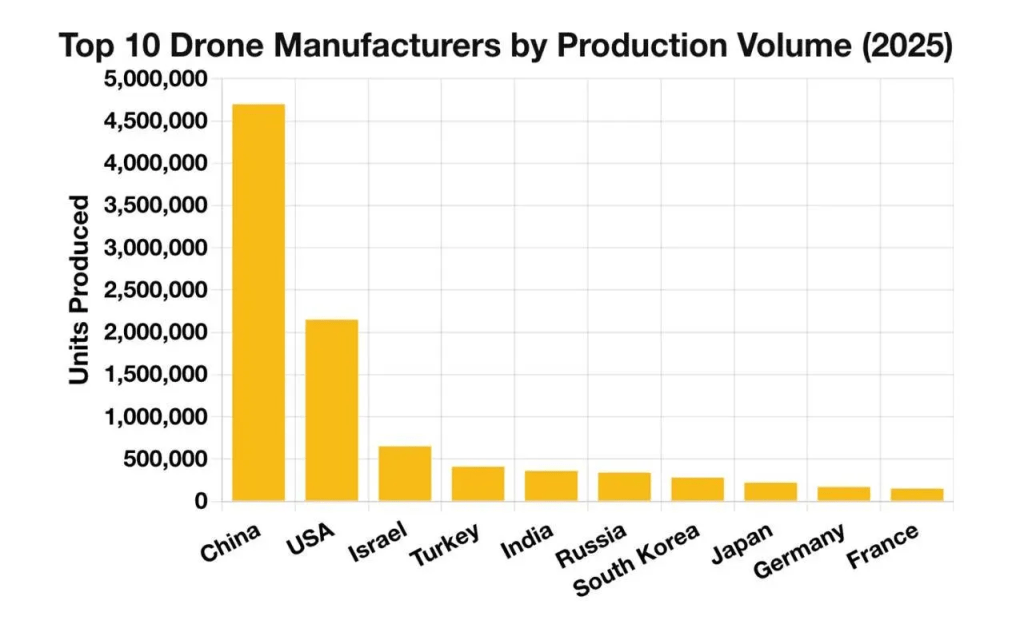

Two years ago, it was clear that in a direct confrontation, the U.S. military would walk all over Russia’s clumsy, outdated post-Soviet army. Now, the reverse is probably true; the Ukraine War has forced the Russian army to learn how to fight with drones, while America is still mostly inexperienced with the new kind of warfare. Russia may not be quite as good at drone war as the Ukrainians, but the U.S. has so far made only incremental changes to how it fights. If the U.S. were to fight Russia today, it would be in for a rude surprise.

Of course, the same is true of China. Its military, like America’s, is still focused mainly on expensive high-performance platforms — aircraft carriers, hypersonic missiles, submarines, and so on. But there’s one big difference between China and the U.S. here — China’s peerless industrial base would give it the ability to construct an overwhelming drone-based force very quickly, while America’s withered industrial base would make it impossible to adapt in time.

Interestingly, the U.S. is still #2 here — albeit a distant second. But worryingly, the U.S.’ traditional allies — Germany, Japan, France, Korea, etc. — make very few drones at all.

Even if they want to, the U.S. and its allies will have an incredibly hard time scaling up indigenous drone production. The reason is that drones are built using a set of technologies that the U.S. and its allies have mostly decided to forfeit to China. Drones use lithium-ion batteries and rare earth electric motors, both of which are almost entirely manufactured in China.

If you want to find the smartest person in the room, find the nicest person in the room.

The smartest person in the room is probably fighting back against the natural tribal urge so many of us have to compete, suppress, and insert ourselves above other people. It takes a lot of mental horsepower to suppress those emotions and realize that if you’re actually nice to people, you can get ahead.

The smartest people in the world know what they don’t know, or they know how little they know. They’re much more likely to say, “Hey, that idea you just talked about, maybe it’s right. I don’t know. I know how uncertain and difficult and complicated the world is.”

The smartest people know the world is not zero-sum. They know that I can get ahead and you can get ahead and we can both win. It takes much less intelligence to think every debate and every interaction is zero-sum, where there is one winner and one loser.

Ozempic and other GLP-1 drugs were initially understood as a metabolism breakthrough: medicines that act like hormones to control hunger, blood sugar and weight. But as researchers probe deeper into how the drugs work, early evidence suggests that GLP-1s may also be reshaping parts of the brain.

Tens of millions of people are now taking the medications worldwide, turning what began as an obesity and diabetes treatment into what could bemodern medicine’s largest unplanned neuroscience experiments.

Some users have reported a type of brain fog and others something broader and harder to define:a strange emotional flattening. People describe less pleasure, less motivation, diminished interest in hobbies and even reduced sexual desire.

At a Shiller CAPE of 39 or above, there is no historical period since 1881 that was followed by attractive long-term real returns.

The CAPE ratio in the United States moved above 42 this week, inching closer to the all-time peak of the tech bubble high in March 2000 when it hit 44.

Part 1: The People Making Enormous Money (For The Moment)

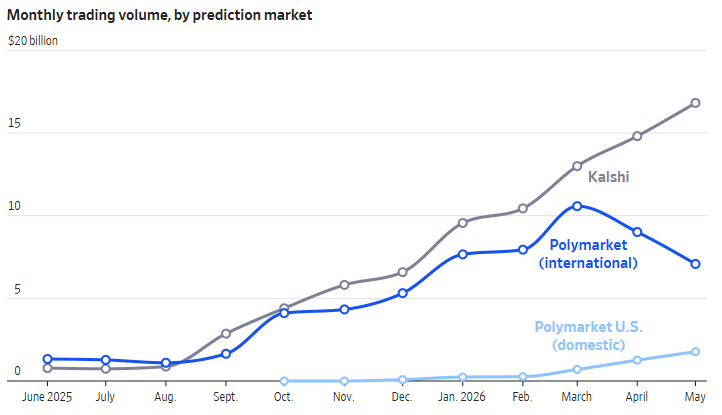

Polymarket is sort of like the Nasdaq or the New York Stock Exchange, except instead of buying and selling shares of publicly traded companies like Apple or Microsoft, the platform allows you to trade on what will happen in the future.

Polymarket and its main rival, Kalshi, are the two largest prediction markets in the world. The two platforms processed $25 billion in trading volume in April, up tenfold from a year ago.

On Kalshi, sports wagers are the largest betting category, accounting for roughly 70 percent of all revenue on the platform. But users on both platforms can wager on just about anything: the price of Bitcoin; the duration of Donald Trump and Xi Jinping’s handshake; whether the headlines on the front page of this newspaper will use the word “stupid” in a given week. Unlike a sports-betting app or a casino, there’s no house, just other bettors on the other side of each trade: Every dollar you lose is a dollar won by someone else.

Traditional financial markets (stocks, bonds) have thousands of sophisticated players battling over trillions of dollars. This means that market prices usually reflect reality, and it’s incredibly difficult for even the most seasoned Wall Street traders to find an edge. Prediction markets, on the other hand, are so immature and so illiquid — there’s just not enough money moving around in them — that the price may not reflect reality.

An army of “sharps” (a loosely coordinated group of traders who are each making six- and seven-figure annual returns) have built a system to exploit it by figuring out what other people don’t yet know. Like Wall Street analysts, they get their edge from research: Hours scouring public voter data, building financial models and even contacting professors, journalists and actual Wall Street analysts to get a leg up. Right now, they are getting very, very rich.

A 25-year-old sharp who goes by the username @Frosen; “I really am just takingmoney from people.” Frosen is a graduate student, and he turned $200 into nearly half a million dollars last year. “Every dollar that I gain is someone losing, and there’s just a lot of people joining, betting, losing and leaving,” he said, laughing nervously. “And then there’s a group of a couple hundred people consistently winning, and that’s the story.”

A better named Fean noticed Kalshi had 98 percent odds of Lady Gaga and Bruno Mars’s “Die With a Smile” topping the Billboard Hot 100 chart. No,he thought, it’s going to be Travis Scott.He then discovered that Scott had sold more than 100,000 singles by inspecting his website’s source code. He was right. Within an hour, Fean had made a 1,000 percent return on his $80 wager.

Most of the sharps ask to be identified by one of their usernames out of fear of being hacked or even “crypto kidnapped.” @JesterTheGoose, a college student studying computer science, deployed an open-source machine-learning tool to predict the outcome of the Chess World Championships. He has turned $2 into more than $150,000.

@PrinceHal, a struggling screenwriter turned full-time Kalshi trader, has been trading for about a decade. He builds inflation-forecasting models that consistently outperform major financial institutions to the tune of $3.7 million in lifetime profits.

The best traders often work alone and try to hide their edge. @Domer, who is widely regarded as one of the most successful prediction market traders on Polymarket, having put money on Robert Francis Prevost’s election as pope and JD Vance’s selection to be vice president, will sometimes email Bloomberg reporters or university professors to try to get a leg up. “It’s every man for himself,” he said; he’s made nearly $5 million.

Some say that @RememberAmalek, who is up more than $750,000, scraped the Nobel Prize Committee website hours before the Peace Prize announcement in order to bet on María Corina Machado.

In the private chat rooms sharps coordinate the best way to buy up ignorance. Recently, after President Trump announced he would nominate the financier Kevin Warsh as the next chair of the Federal Reserve, a conspiracy theory spread online that he would instead choose Judy Shelton, who was an economic policy adviser during his first campaign. The market saw $127,684,065 in Shelton trades on Polymarket. Warsh was nominated; the “dumb money” lost millions; and per usual, the sharps won big. “You can’t stop the “noobs,” the newbies, “from buying literally worthless shares, over and over and over again, every single day. You can’t stop them.”

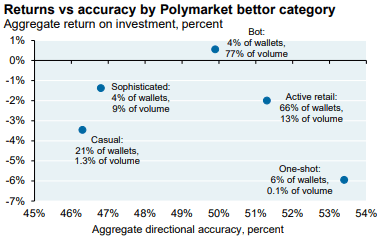

Part Two: The High Speed Algorithmic Bots Are Coming For Everything

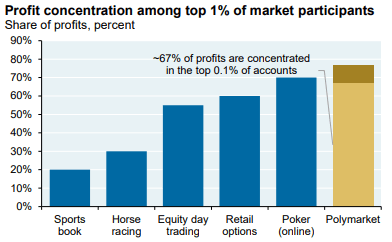

There’s a lot of predation in prediction markets: 1% of participants on Polymarket earn 76.5% of the profits due to high speed algorithmic bots that reprice prediction contracts based on breaking information faster than the average person. Prediction market profit concentration is much higher than in online poker, day trading, horse racing and other gambling platforms shown below.

These gains accrue overwhelmingly to automated traders (bots). Joshua Della Vedova at the University of San Diego performed a fascinating analysis of over 200 million Polymarket trades from November 2022 to February 2026. Vedova found that profits are more closely linked to execution timing than to directional accuracy.

Automated traders (bots) achieved 49.9% aggregate directional accuracy (no better than a coin flip), yet earned the only positive aggregate return in the sample at $133 million. Active retail traders achieved 51.3% accuracy but lost $79 million, and other non-bot bettor categories had negative returns as well.

The reason is execution, not forecasting: bots win by providing liquidity and entering markets early (about 10 bots account for 70% of bot profits), while bettors that arrive after prices absorb relevant information pay entry prices that leave no room for profit, regardless of accuracy.

Della Vedova also identifies a subset of accounts whose accuracy and execution are consistent with trading on private (inside) information stripping those profits out would make the non-bot returns shown on the right look even worse.

Welcome to the weird and twisted philosophy of looksmaxxing, the online subculture devoted to optimizing male appearance through gym routines, skin care, jawline exercises and surgery. They advocate bonesmashing, or hitting one’s face repeatedly with a hammer to change the face shape.

Looksmaxxers may not be aware of it, but they are optimizing themselves not for attraction from women, but for respect from men. That is the hidden logic of “looksmaxxing”. Men respect signs of dominance and toughness. A heavy jaw, sharp cheekbones, a hard stare. These features impress other men because they signal strength. So when a young man imagines an attractive male face, he tends to imagine an exaggerated version of those traits. He then sets out to build it.

Women, generally speaking, want something different. They tend to prefer a face that is softer than men assume. When masculine features get too extreme, they stop registering as attractive and begin to appear bizarre or even frightening. The looksmaxxer who has carved himself into a comic book caricature has pushed past the point where most women find him appealing. (Relatedly, some women make a parallel mistake, assuming men prefer extreme thinness when many men actually prefer healthier, curvier female bodies.)

A man who spends hours every day fine-tuning his face and body exudes qualities women tend to dislike. He can come across as vain, high-maintenance and self-absorbed — less like a secure partner than someone perpetually scanning for the next option.

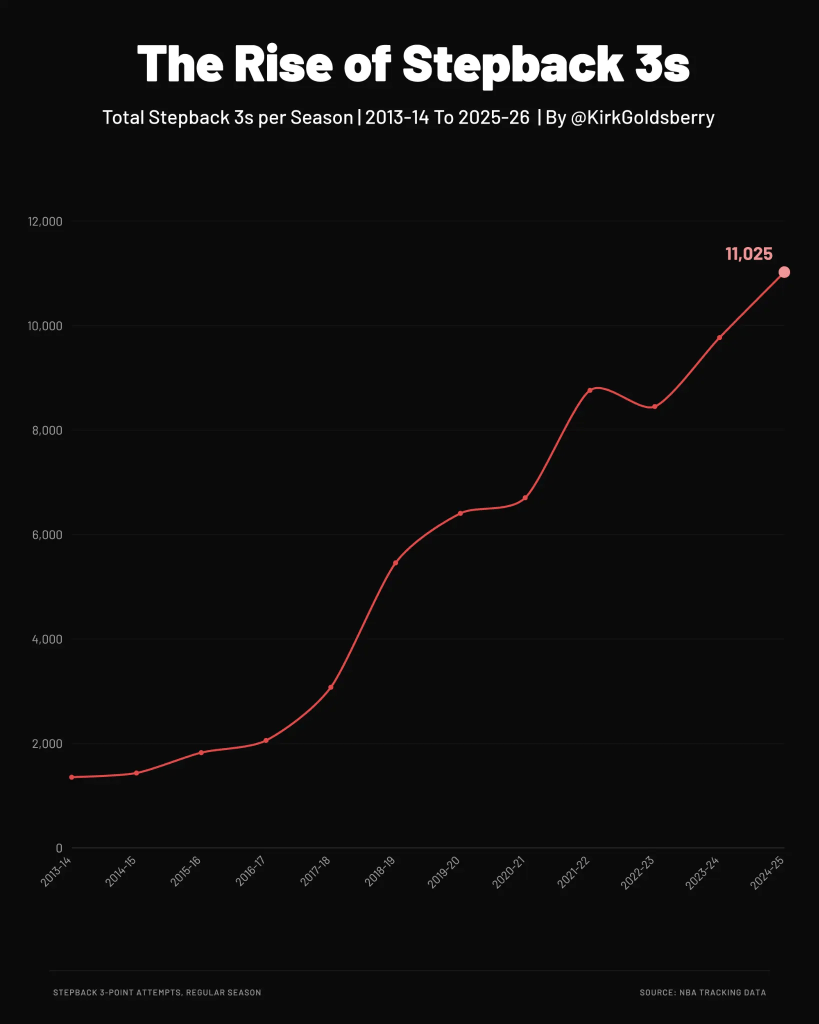

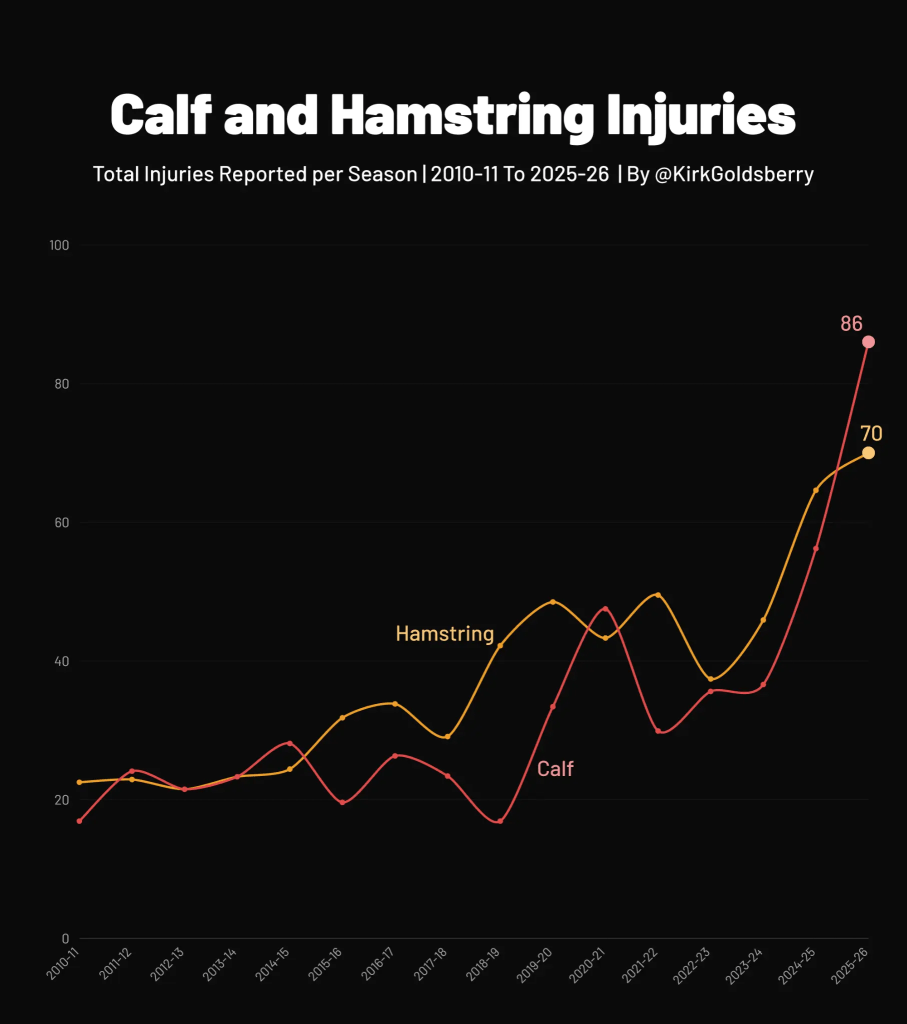

In 2010-11, there were 18 documented calf injuries across the entire NBA season. Last season, there were 60. This season, 86. Why?

Basketball used to be a two-footed sport. Nowadays, the game is a one-footed sport. Most players are making every move off of one foot. The modern NBA is a pace-and-space machine—100-plus possessions a night, built on rapid ball movement, floor spacing, and the core principle that any player must be able to create offense off the dribble from anywhere. The epicenter of NBA offense has migrated from the low block to the perimeter, where endless drive-and-kick sequences stack on top of one another.

Today’s game of relentless one-on-one creation; guards, wings, and increasingly centers attacking closeouts; and transition offense requires a different kind of movement. It requires rapid changes of speed and direction. And almost all of it happens off one foot.

Muscle damage isn’t caused by how hard a muscle works, but rather by how far it stretches while it’s working. The muscle almost always has to be activated to really be injured, and it almost always has to be stretched. When both of those things happen at once, that’s when injuries can happen.

The calf is particularly vulnerable to that combination because of our anatomy. The calf muscle has short fibers, and when the ankle rotates and the knee extends at the same time, it puts immense strain on the muscle.

That strain is amplified for taller people. The fibers don’t scale with the body. The bones—the levers—do. So a bigger person, when they rotate their knee joint or their ankle joint 20 degrees, they stretch their muscles relatively more. The same move, performed by a larger body, is more dangerous. Not because the player is weaker, but because the geometry is worse.

____________________________

I recently tuned into an episode of “The Diary of a CEO” podcast. The guest was an Irish comedian by the name of Jimmy Carr. The host asked Jimmy a pointed question: “What is the meaning of life?” Jimmy responded, “I’ll do it in five words.” What were the five words?

“Enjoying the passage of time”

Remember that trip you took with your friends to that warm weather destination? You enjoyed each other’s company and the days were filled with friendship, camaraderie, and wonderful moments of joy and happiness? You were absolutely enjoying the passage of time, and it had nothing to do with money or the state of the stock market and the world. You were living your best life.

All of this is to say, if we constantly worry about the national debt, the dollar, politics, how much money we have, or what someone on the news is saying, we are trapped in a prison of our own design. Now I know this isn’t a black or white thing; there are times when we won’t be enjoying the passage of time. We might be sick, or a family member may be struggling, or something is really impacting us.

Build for the long-term. Be thoughtful and patient. Have a plan. But enjoy the passage of time. Focus less on the things that can make us miserable. This life is all we’ll ever get.

___________________________

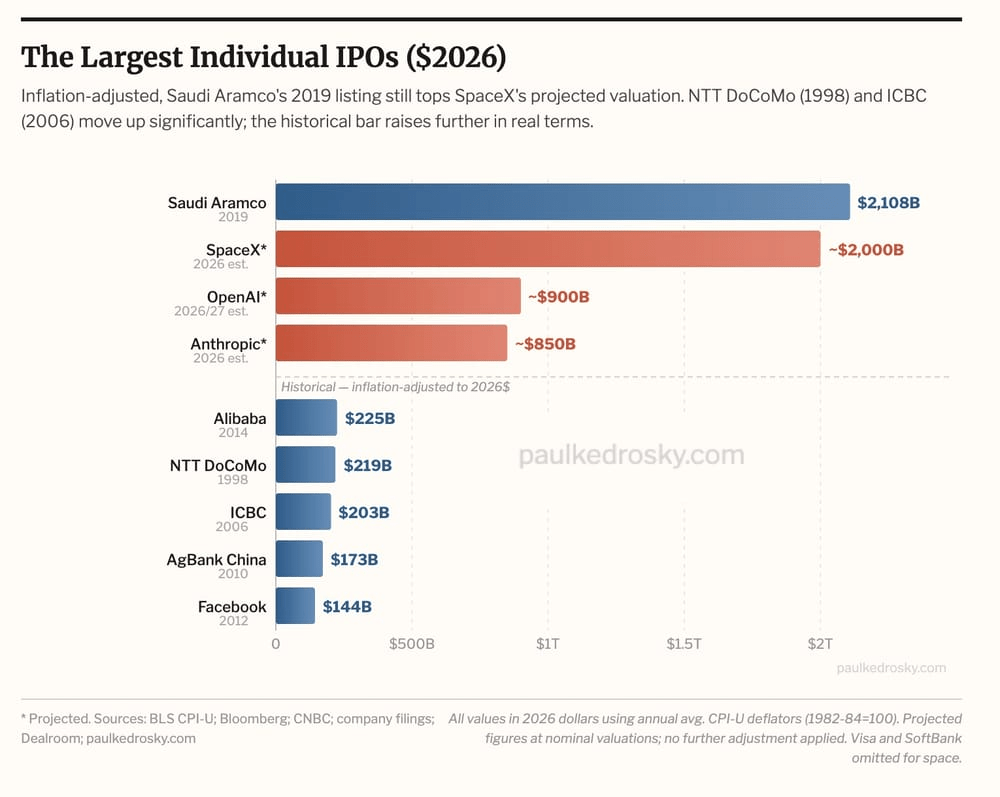

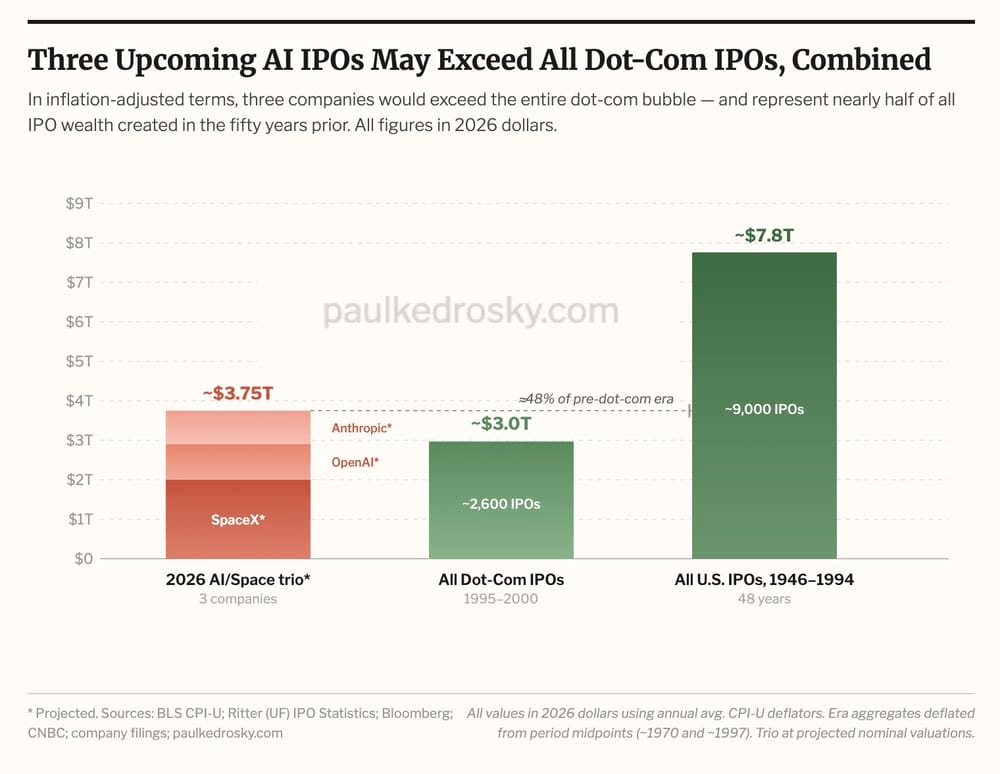

Three companies — SpaceX, OpenAI, and Anthropic — are expected to go public in mega-IPOs in the second half of 2026. The posited numbers are simply staggering compared to the largest IPOs in recent history, as the following figure shows.

In inflation-adjusted terms, SpaceX alone would rank as the second-largest IPO in history, just behind Saudi Aramco. All three together would exceed the entire dot-com IPO wave of 1995–2000. They will be at least half the value, inflation-adjusted, of all US IPOs since WWII.

But people aren’t focused on the right things. That much new equity supply hitting in a few months creates a math problem: the money has to come from somewhere. Most of it will come from existing holdings. Passive funds will be forced buyers once these names join the indexes, which will happen much faster than usual, given recent index rule changes. That means mechanical selling pressure on whatever many funds currently own, which is mostly the same large-cap tech stocks everyone else owns.

_______________________________

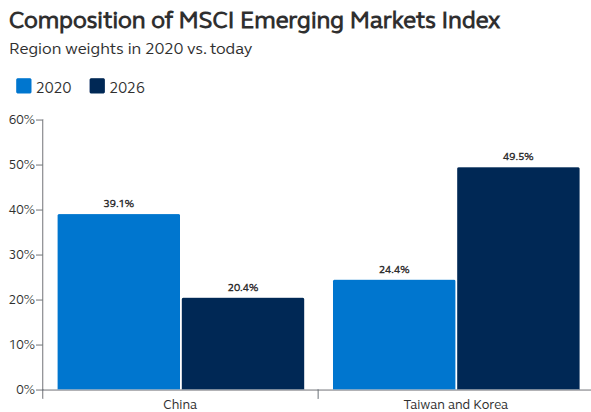

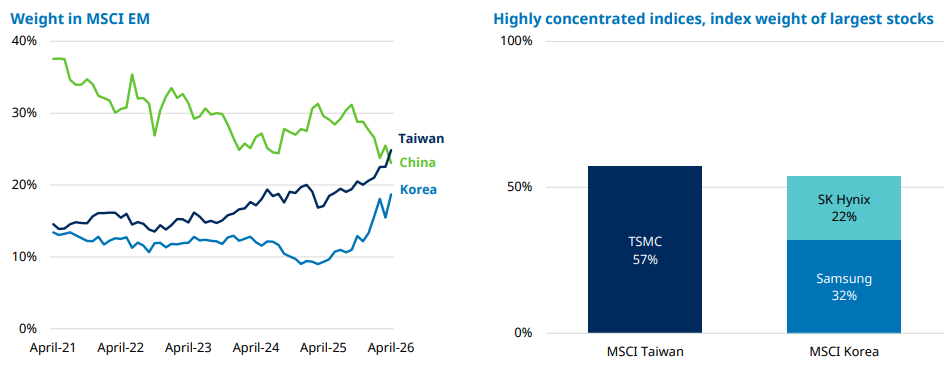

Taiwan and Korea are close to overtaking China’s stock market in size, largely due to only three stocks:

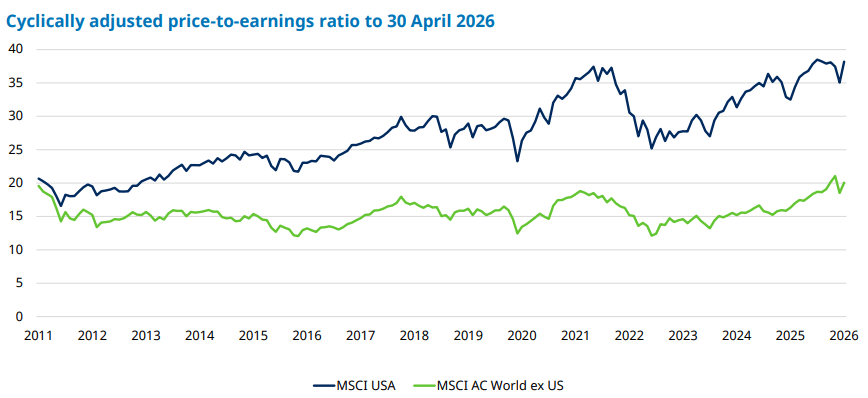

The gap between the United States (blue) and the rest of the world (green) based on their Price To Earnings ratios remains enormous: which means the U.S. is far more expensive.

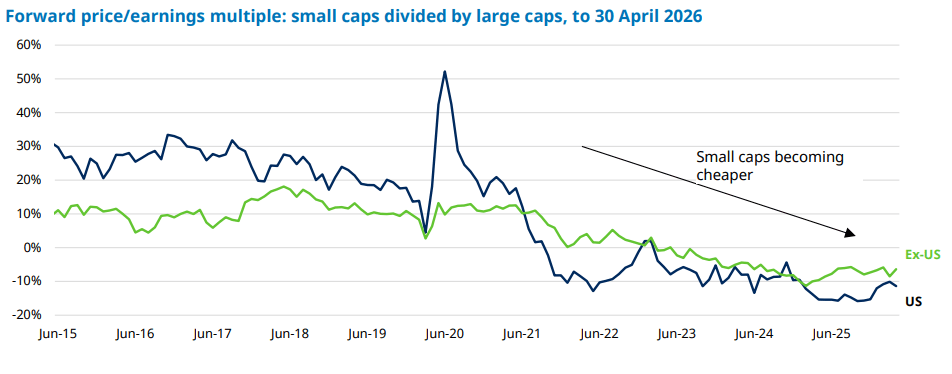

Small cap stocks continue to become less expensive relative to large cap stocks around the world: