Money is less of a factor in attraction than people think. What matters more is your ambition. The academic literature on evolutionary biology supports this. In a study across 37 cultures, evolutionary psychologist David Buss found that, on average, potential partners valued “ambition and industriousness” more than “good financial prospects” when choosing a mate.

In evolutionary terms, this is known as Resource Holding Potential (RHP), or your ability to acquire resources in the future. A husband signals high RHP while working, but signals low RHP if he retires early, gets high and plays video games with friends all day; even if he worked unbelievably hard to get to that point. Why is ambition more attractive than money?

Because money says, “I was useful,” while ambition says, “I am useful.”

People care about the future. People care about the genes they pass on to their offspring. And they want to pass on traits like industriousness because those traits will help their children acquire future resources, and so on. Having money makes you more attractive. But it’s not the money that’s actually appealing, only how you acquired it. The potential to collect more resources is the draw from potential mates.

______________________

Wise Words From Charley Ellis:

On Winning By Not Losing

A loser’s game is any game, contest, or activity in which the ultimate victor is determined by the actions of the loser. These contests are not won; they are lost.

In tennis, pros can be aggressive. They have the skill, precision, and experience to place shots just outside their opponent’s reach. They play a winner’s game. The match goes to the player who earns the most wins. Amateurs, however, often lose by trying to play like the pros, because it leads to unforced errors. It’s a loser’s game. Amateurs win in tennis by volleying until their opponent hits it into the net or out of bounds. They win by not losing.

There are two different games being played in the stock market. The game the experts play differs from the game the amateurs play. The game amateurs should play, and many experts too, is built on a foundation of avoiding errors. Essentially, not losing. Fewer errors lead to better results.

Luck

Every investor should recognize the powerful potential impact of luck — not good luck, but bad luck. We can all live through good luck. But bad luck — the apparently random occurrence of adversity — is equally prevalent, and its consequences can be far greater.

Getting Excitement Out of the Market

Go to a continuous-process factory sometime — a chemical plant, a cookie manufacturer, a place that makes toothpaste. Everything is perfectly repetitive, automated, exactly in place. If you find anything interesting, you’ve found something wrong.

Investing is a continuous process too; it isn’t supposed to be interesting. It’s a responsibility. If you go to the stock market because you want excitement, then sooner or later you will lose. Everyone who thinks the stock market is a game loses — everyone, to the last man, woman, and child. So, the purpose of an investment policy is simply to ensure that your continuous process never breaks down.

On Over-Confidence

A rapidly rising market makes you forget that those whom the gods would destroy, they first make confident. The more you know, the higher the odds that you’ll make a serious mistake. That’s why it’s not the beginners who tend to die at skydiving and why most car accidents happen within a few miles of home. There’s a saying in the British Royal Air Force that investors need to remember: “There are old pilots, and there are bold pilots, but there are no old, bold pilots.”

As human beings, particularly if we are successful in other parts of our lives, we are notoriously unable to accept the obvious reality that, on average, we are average, and that our normal experiences will usually be about average because we are, as a group, captives of the normal distribution of the bell curve. Studies all the time show we think we are above-average drivers, above-average parents — and above-average investors. And we do tend to take it personally when our stocks go way up or go way down, even though, as Adam Smith admonishes, “The stock doesn’t know you own it.”

________________________

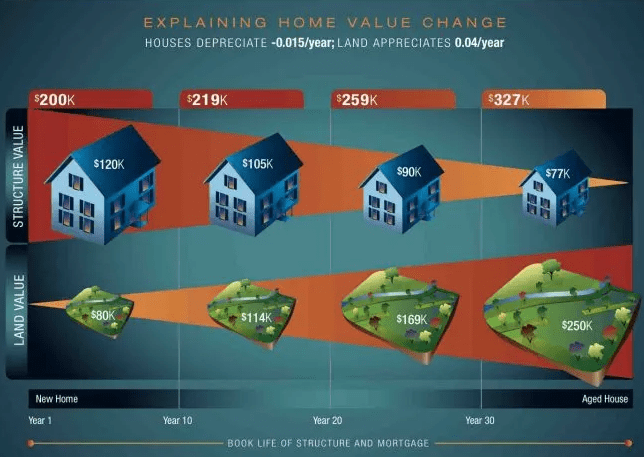

Land Appreciates. Homes Depreciate.

The value of a home (excluding land) declines over time unless it is updated to break even. Think of it in the context of not updating the home for 30 years, which makes the concept much easier to understand. The house will slowly fall apart. Meanwhile, in most housing markets, land values eventually rise over a 30-year period, and the cash-poor homeowner can sell for more than their original purchase price.

__________________________

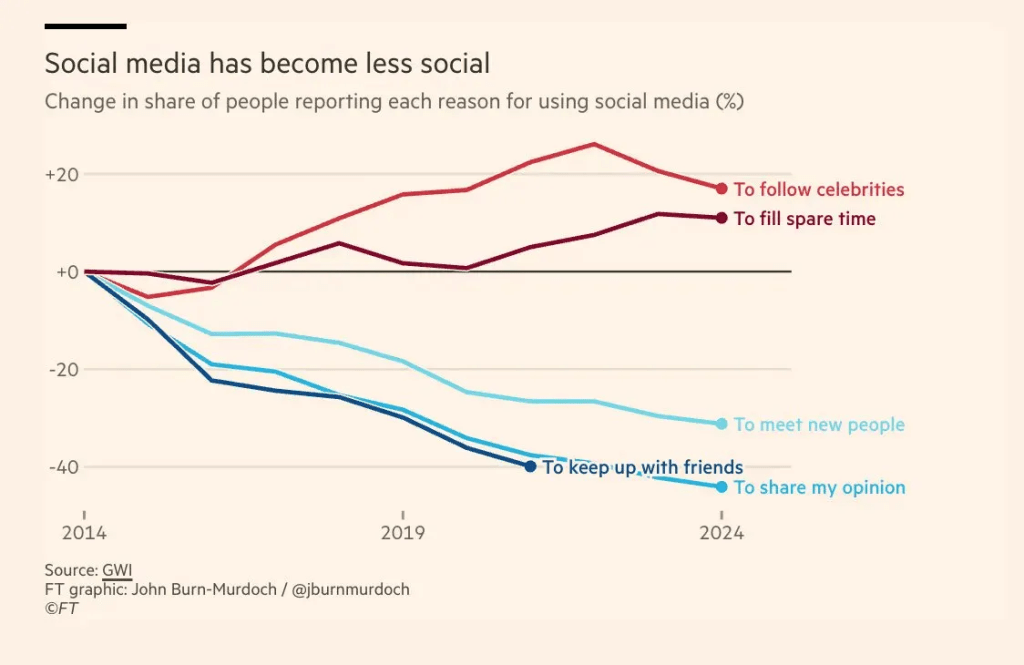

Social media has become less social.

__________________________

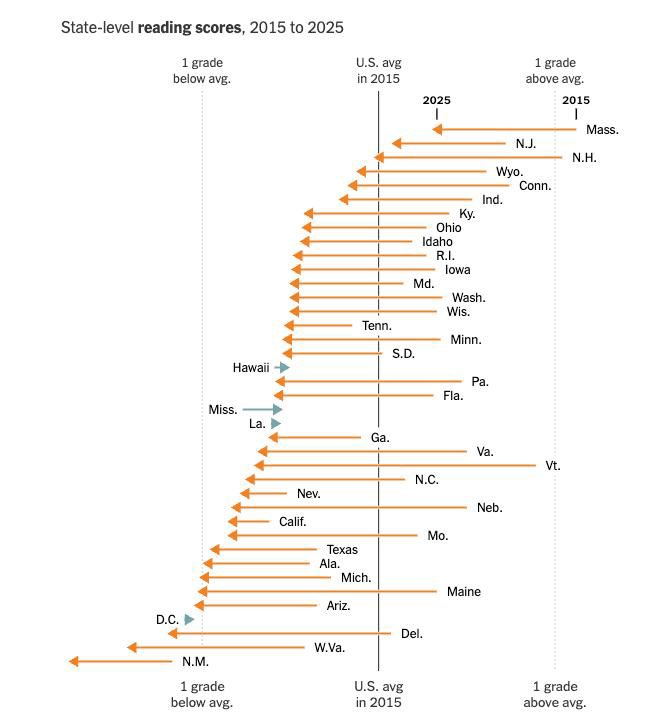

State level reading scores have dropped dramatically over the last 10 years.

__________________________

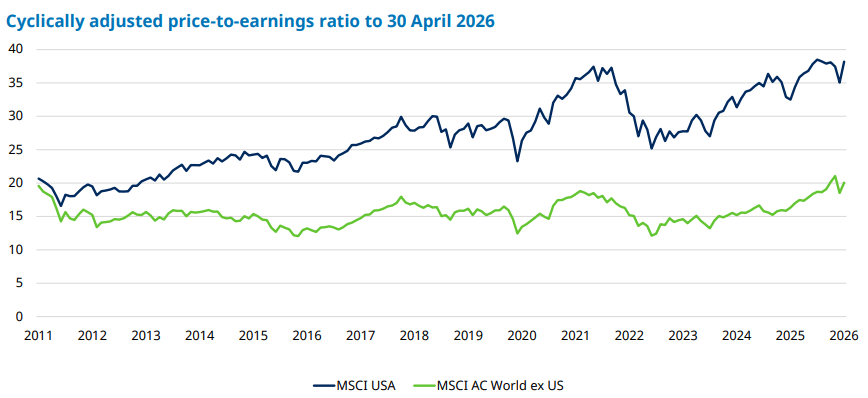

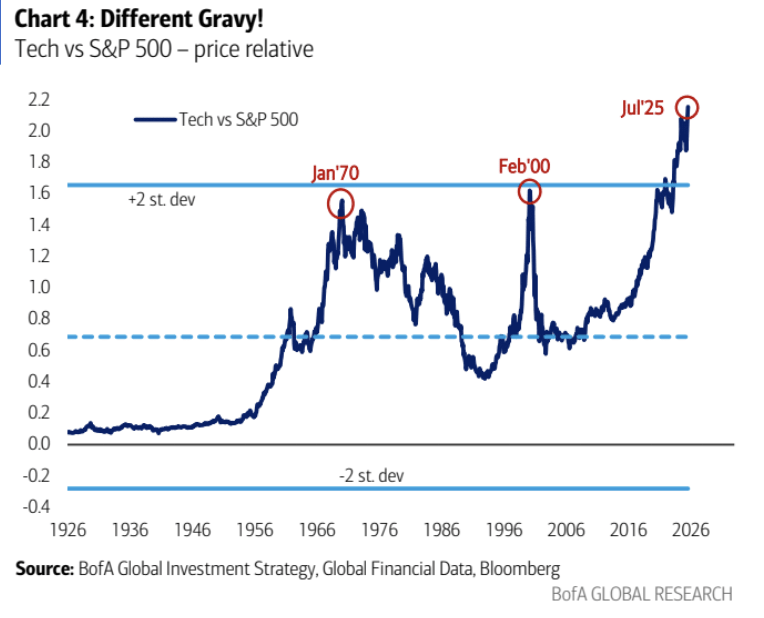

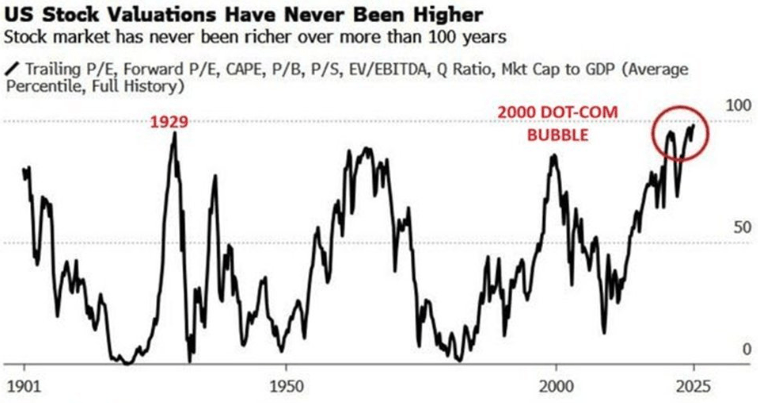

Based on an average the average of the valuation metrics below, the U.S. stock market has now become more expensive than both the 1929 and 2000 bubble peaks:

- Trailing (P/E) Price to Earnings

- Forward (P/E) Price To Earnings

- Cyclically Adjusted Price To Earnings (CAPE)

- Price to Book (P/B)

- Price to Sales (P/S)

- Enterprise Value (EV) to Earnings Before Interest Depreciation & Amortization (EBITA)

- Market Value to Replacement Cost Of Physical Assets (Q Ratio)

- Market Cap to GDP

_________________________________

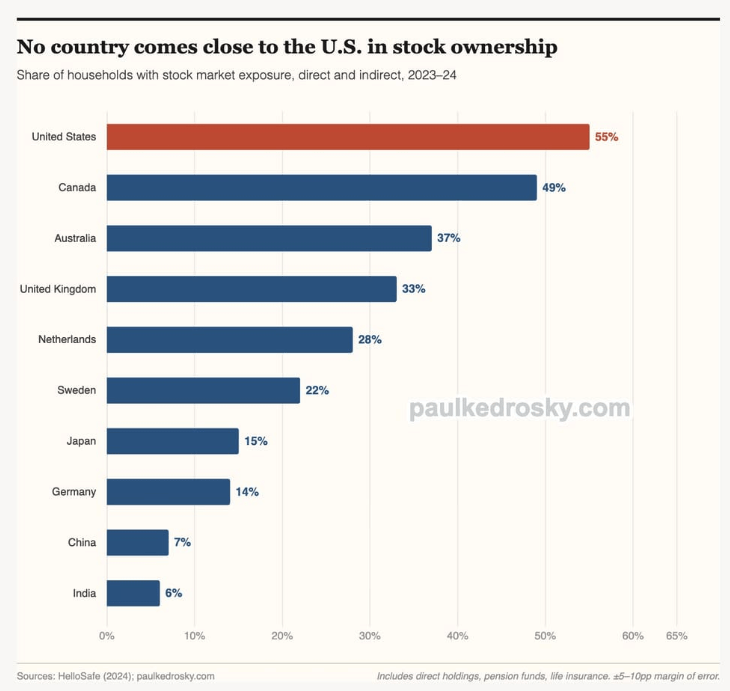

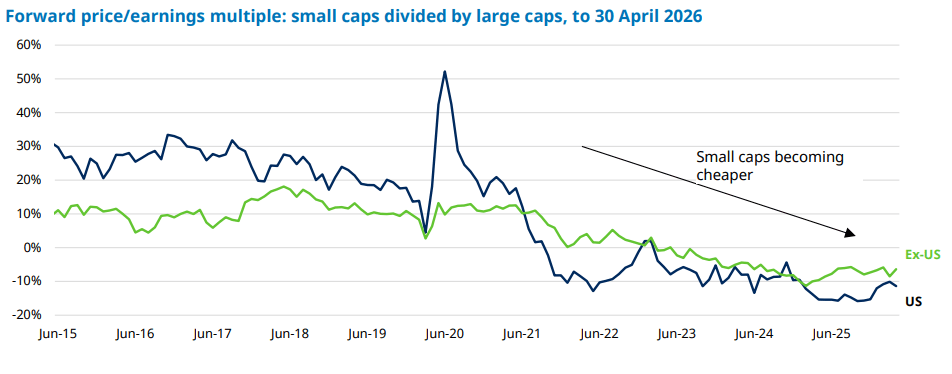

U.S. households are far more invested in stocks relative to the rest of the world: