Does Time Seem To Be Flying By? There Are Ways To Slow It Down. Exposure to variety in your life creates memories, which in turn makes time seem to pass slower because there is more to look back on. For children, fresh experiences and “firsts” are a natural part of everyday life — losing that first tooth, first day of school, first bicycle. This constant stream of new occurrences stretches the passage of time in a young mind.

Older adults, on the other hand, often slip into predictable patterns where days differ only by the calendar date. With scant new memories being formed between existing time markers like birthdays and holidays, Christmas seems to roll around quicker each year.

So as simple as it sounds, if you want time to slow down, the key is to intentionally introduce more novel experiences into your daily routine. Researchers divide these into two categories:

Distinct novelty. Taking a trip to somewhere you have never been fires a whole different system in your mind that preserves all the details like a high-resolution photo, creating vivid memories you recall for years to come. Your brain’s reaction is, “This looks important. I’d better save all of this!”

Common novelty. You decide to try a different restaurant in your neighborhood instead of the ones you normally frequent. It’s new but related to something you already know, so the impression is not particularly powerful.

__________________________

Typically, what you find in highly successful people is that an addiction to work is, in fact, based on an inchoate belief that love from others—including spouses, parents, and friends—can be earned only through constant toil and exceptional merit.

Why might someone fall prey to such an erroneous belief? It could be the way you were raised. Workaholic parents tend to have workaholic kids. If you grow up seeing adulthood modeled by people who work all hours and are rarely home, you can be forgiven for regarding this as appropriate behavior for a responsible spouse and parent. This is at least partly the same mechanism behind the fact that you are much likelier to become an alcoholic if you were raised by one.

Researchers have also shown that when parents express love for a child in a conditional way based on the child’s behavior, that person is likely to grow up feeling that they deserve love only through good conduct and hard work. This might sound as though I’m describing terrible parents, but I don’t mean to do so at all; well-intentioned parental encouragement can be heard by a child as a message about their worthiness.

In the workaholic’s case, it might look like this: Your parents wanted you to succeed in school and in life, so they gave you the most love and attention when you got good report cards, won at sports, or earned the top spot in the orchestra. You were a bright kid, and put two and two together: I am extra lovable when I earn accolades. In my experience, this describes the childhood of a lot of people who strove to be special to gain their parents’ attention, and who carry this behavior into adulthood by trying to earn the love of others through compulsive work.

__________________________

Michelob Ultra has become king of the hill among beer brands. By topping the sales by volume charts for 2025, it has ousted Modelo Especial as America’s best-selling beer.

While its lower caloric content certainly appealed to many people, some of Michelob Ultra’s success can also be credited to aggressive marketing campaigns, which helped the brand gain notoriety at major sporting events like the FIFA Club World Cup, NBA games, and the PGA tour. That falls in line with Michelob Ultra’s focus on folks with active lifestyles.

More people are seeing Michelob Ultra on tap. The new top dog surpassed its sister brand, Bud Light, in bar and restaurant presence in December 2024. Michelob Ultra’s upsurge in popularity happened at a relatively quick pace; the brand has flourished by 15% since 2020. That equates to a 2% hold over the entire beer market in that time frame.

___________________________

A.I. investors shouldn’t swim upstream, but fish downstream: companies whose products rely on achieving high-quality results from somewhat ambiguous information will see increased productivity and higher profits. These sectors include professional services, healthcare, education, financial services, and creative services, which together account for between a third and a half of global GDP and have not seen much increased productivity from automation. AI can help lower costs, but how individual businesses incorporate lower costs into their strategies—and what they decide to do with the savings—will determine success. To put it bluntly, using cost savings to increase profits rather than grow revenue is a loser’s game. The companies that will benefit most rapidly are those whose strategies are already conditional on lowering costs.

With A.I., knowledge-intensive services will get cheaper, allowing consumers to buy more of them, while services that require person-to-person interaction will get more expensive, taking up a greater percentage of household spending. This points to obvious opportunities in both. But the big news is that most of the new value created by AI will be captured by consumers, who should see a wider variety of knowledge-intensive goods at reasonable prices, and wider and more affordable access to services like medical care, education, and advice.

There is nothing better than the beginning of a new wave, when the opportunities to envision, invent, and build world-changing companies leads to money, fame, and glory. But there is nothing more dangerous for investors and entrepreneurs than wishful thinking. The lessons learned from investing in tech over the last 50 years are not the right ones to apply now. The way to invest in AI is to think through the implications of knowledge workers becoming more efficient, to imagine what markets this efficiency unlocks, and to invest in those. For decades, the way to make money was to bet on what the new thing was. Now, you have to bet on the opportunities it opens up.

_________________________

There is a consistent doom-and-gloom forecast that within 18 months A.I. software will make human capabilities worthless. The far more significant crisis is precisely the opposite. Young people are already degrading their cognitive capabilities by outsourcing their minds to machines long before software is ready to steal their jobs.

Many recent articles have loudly proclaimed what most people were already thinking: Everybody is using AI to cheat their way through school. By allowing high school and college students to summon into existence any essay on any topic, large language models have created an existential crisis for teachers trying to evaluate their students’ ability to actually write, as opposed to their ability to prompt an LLM to do all their homework. Massive numbers of students are going to emerge from university with degrees, and into the workforce, who are essentially illiterate.

The demise of writing matters, because writing is not a second thing that happens after thinking. The act of writing is an act of thinking. Students, scientists, and anyone else who lets AI do the writing for them will find their screens full of words and their minds emptied of thought.

As writing skills have declined, reading has declined even more. Most of our students are functionally illiterate. Achievement scores in literacy and numeracy are declining across the West for the first time in decades.

Americans are reading words all the time: email, texts, social media newsfeeds, subtitles on Netflix shows. But these words live in fragments that hardly require any kind of sustained focus; and, indeed, Americans in the digital age don’t seem interested in, or capable of, sitting with anything linguistically weightier than a tweet. The share of Americans overall who say they read books for leisure has declined by nearly 50 percent since the 2000s.

Even America’s smartest teenagers have essentially stopped reading anything longer than a paragraph. Students are matriculating into America’s most elite colleges without having ever read a full book. High schools have chunkified books to prepare students for the reading-comprehension sections of standardized exams.

Thinking benefits from a principle of “time under tension.” It is the ability to sit patiently with a group of barely connected or disconnected ideas that allows a thinker to braid them together into something that is combinatorially new.

__________________________

A.I. related stocks have accounted for 75% of S&P 500 returns, 80% of earnings growth and 90% of capital spending growth since ChatGPT launched in November 2022. Data centers are eclipsing office construction spending and are coming under increased scrutiny for their impact on power grids and rising electricity prices.

The biggest medium-term risk I can think of for top heavy US equity markets: China’s Huawei and SMIC pierce the $6.3 trillion NVIDIA-TSMC-ASML moat by creating their own supernode computing clusters and deep-ultraviolet lithography machines of comparable quality.

Oracle’s stock jumped by 25% after being promised $60 billion a year from OpenAI, an amount of money OpenAI doesn’t earn yet, to provide cloud computing facilities that Oracle hasn’t built yet, and which will require 4.5 GW of power (the equivalent of 2.25 Hoover Dams or four nuclear plants), as well as increased borrowing by Oracle whose debt to equity ratio is already 500%. In other words, the tech capital cycle may be about to change.

__________________________

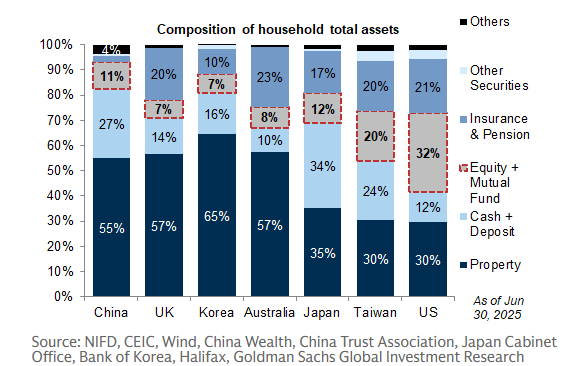

This is a fascinating look at how foreign households invest. I had no idea U.K. residents had such a low percentage of their personal investments in stocks, and the amount Japanese citizens hold in cash (which has provided no interest/return for decades) is incredible.

_____________________________

____________________________________

Africa is enormous. These countries would all fit within Africa’s border: