Statistically, if you’re down by two goals in hockey, you should be pulling the goalie with something like eight minutes left, not with a minute and a half. But if you do that and the other team scores two empty-netters, you look like an idiot. Right now, they pull with 90 seconds left, and if they lose, everyone says, ‘Well, you had to try.’ You pull with five minutes left and lose 5–1 and the announcers say, ‘What the hell is this guy doing?’ These hockey coaches, when they wait too long to pull the goalie and lose the game, they are choosing to be wrong rather than look wrong.

Max Greyserman is ranked No. 33 in the world, not a star but tantalizingly close. In his rookie season of 2024, his average score over 18 holes was 69.998; if he had improved that by .085 — or less than one-tenth of a stroke per round — he would have passed Rory McIlroy and cracked the top five on the tour. It’s not a perfect comparison; McIlroy played some harder courses. But it’s an indicator of how scarily slim the margins are in pro golf — in both directions.

All it takes to slip back into the middle of the pack, maybe even to lose your tour card, is a string of small errors made under pressure, plus some bad luck. Success in golf rides on physical skill, of course, but the closer you get to the top, the more it becomes about intangibles, like the ability to deal with these hairsplitting variations in performance and not lose your grip on probabilities.

That’s why I became interested in Max and ended up out there at Pebble Beach talking to his dad about pulling the goalie. What sounded at first like a digression turned out to be more of a nudge: This is how to watch sports. Don’t get stuck on outcomes. Avoid the knee-jerk determination of good or bad. Look for the patterns, the process, the decision-making, the mind-set, the systems for dealing with risk. This is how sports can actually reveal something to you about human nature.

_______________________________

Douglas MacArthur was the American general who commanded Allied forces in the Pacific during World War II and later ran occupied Japan. William Manchester, in his biography of MacArthur, mentioned how in 1950, when MacArthur was in Tokyo, he read exactly five newspapers every morning. What’s unusual was that these newspapers were all at least three days old. His staff thought he was losing it. Why would the Supreme Commander want stale news when fresh news arrived by the hour?

MacArthur’s reasoning was simple. Three days gave the initial panic time to settle. It let him see which stories actually stuck around and which ones everyone had already forgotten about. For him, this delay acted as a filter because it cut out all noise and what remained, if anything, was a signal.

Nassim Taleb once wrote: “To be completely cured of newspapers, spend a year reading the previous week’s newspapers.”

This is such a powerful thought. Most of what passes for urgent news has zero shelf life. Even if you read it a week later, you’ll see how little of it actually mattered. Taleb was talking about newspapers, but the principle applies even more to social media, where information decays not in weeks but in hours.

Our brains aren’t good at sorting the flood of information in real time. Every piece of information, regardless of quality, takes up mental real estate. It doesn’t matter if it’s valuable or garbage, it still occupies space in your head.

Most investment mistakes aren’t failures of information. They’re failures of judgment. You had the information, like everyone did. But you misjudged what it meant because you were processing it in a rush, surrounded by other people’s opinions.

You do need to stay informed about the businesses you own and the industries you follow. The question is: what’s the minimum effective dose of information? For most investors, that ratio is way lower than they think. You probably need about 10% of the information you’re currently consuming. Maybe less. The rest is entertainment dressed up as education.

____________________________

It’s tempting to believe that smartphones and social media were introduced to an ideal society and ruined everything. But the social problems we face today — while linked to contemporary digital technologies — are deeper and more nuanced than that. They originated from 20th century technological and cultural forces that also brought extraordinary benefits.

Starting in the 1950s, America underwent a wave of changes that looked like unalloyed progress. The 1956 Federal Highway Act funded 41,000 miles of interstate, opening up a suburban frontier where families could afford their own homes with yards, driveways, and privacy. Women entered the workforce en masse, expanding freedom and equality and adding to household incomes. The television — which provided cheap, effortless entertainment — was adopted faster than any technology in history, from 10% of homes in 1950 to 90% by 1959, according to Putnam. Air conditioning made homes comfortable year-round. Shopping migrated from Main Street to climate-controlled malls with better prices and wider selection.

These changes were widely embraced because they made life better for millions of people in countless ways. But they quietly eroded community, shifting American life toward comfort, privacy, and control, and away from the places and habits that had held communities together.

Suburbs scattered neighbors across cul-de-sacs designed for privacy over casual interaction. The front porch — where you might wave to a neighbor and end up talking for an hour — gave way to the private backyard deck and the two-car garage. Television privatized entertainment, moving what once happened in theaters, dance halls, and community centers into living rooms where, by the 1990s, the average American adult was watching almost four hours a day, and, Putnam tells us, half of adults usually watched alone. Dual incomes often meant neither parent had time for the PTA meeting or volunteer shift. Local shops on main street closed because they couldn’t compete with the mall.

Generation by generation, the habits of connection weakened while the scope of everyday comfort, privacy, and control grew. Then came the digital revolution — with the internet and smartphones — and these isolating forces accelerated.

Digital technology extends the logic of suburban sprawl: it allows us to live not just physically apart, but entirely in parallel. In the past decade, e-commerce jumped from 7% to 16% of retail while physical stores shuttered. Online grocery sales are growing 28% year over year. Home exercise has surged in popularity. Twenty-eight percent of Americans work from home, up from just 8% in 2019. Across every sphere — shopping, working, exercising, socializing — we’re choosing staying in over going out because we enjoy the privacy and convenience.

Meanwhile productivity technologies are dissolving the boundaries between work and personal life. While work used to have clear boundaries, today, for knowledge workers in particular, a laptop and Wi-Fi mean the office never closes. Work bleeds into every hour, every room. When you can always be earning, social commitments become harder to justify.

________________________________

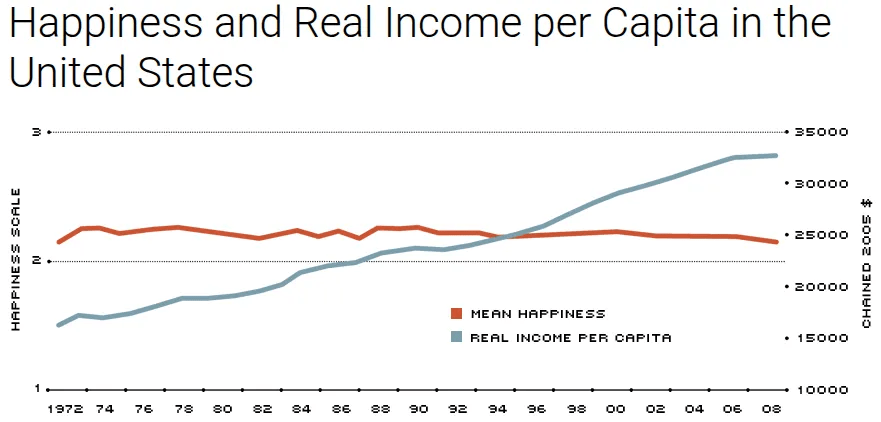

In what’s now known as the Easterlin paradox, wealthier individuals report greater happiness at any given moment, but average happiness does not rise as societies get richer.

Our long-held belief that money can’t buy happiness appeared to be validated by research suggesting happiness plateaued around $75,000 a year. Further research found something more nuanced: happiness rose with income up to about $100,000 — and then leveled off. For others, happiness continued to rise. And for the happiest group, it even accelerated.

If you become rich, you’re still the same you but just richer. Wealth can offer many blessings, but it can’t exorcise any demons. I imagine it like arriving at a tropical getaway only to discover you can’t take off your winter coat — sealed tight by past experiences, trauma or misplaced expectations.

_________________________

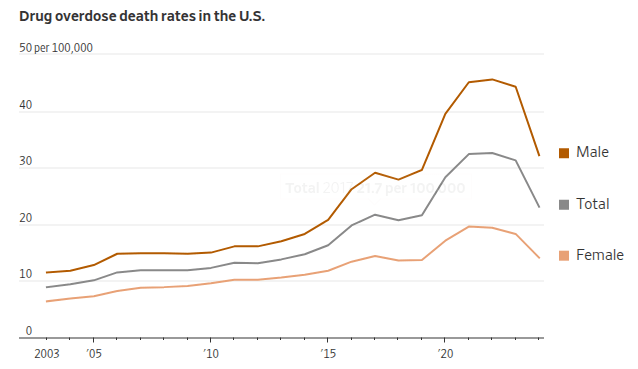

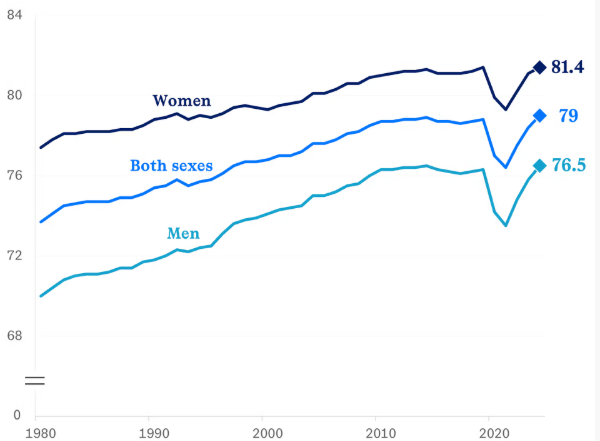

Life expectancy in the U.S. reached a record high in 2024, according to figures released by the federal government this week.

Heart disease, cancer and unintentional injuries remained the top-three leading causes of deaths. Drug overdose deaths decreased by more than 26% between 2023 and 2024, marking the largest year-to-year drop in those types of fatalities recorded by the federal government.