A higher price to earnings ratio means a country’s stock market is more expensive. A lower number is less expensive. It’s the price you are paying for the earnings of the companies.

Average of Foreign Developed Stock Markets: 19 Average of Foreign Emerging Stock Markets: 17

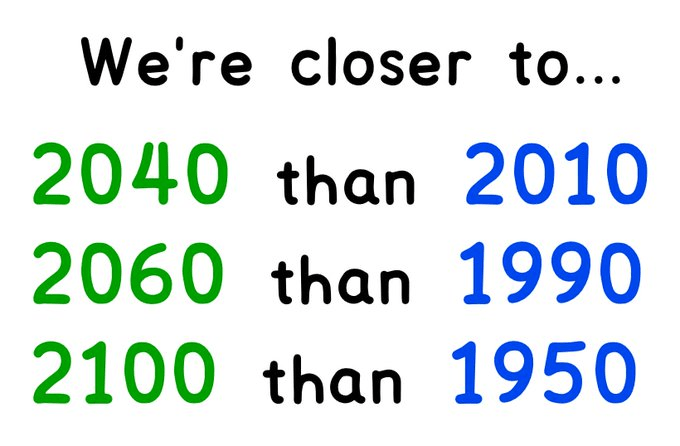

Some thoughts on time. Times we grew up envisioning as the far future aren’t so far away anymore. Even if lifespans stayed as they are now, many of today’s college students will live to see the 22nd century. Many of today’s babies will still be in the peak of their careers in the year 2100. And 2040, 2060, and 2100 are now closer to us than 2010, 1990, and 1950.

Likewise, much of what still feels like recent history is beginning to look a lot like ancient history. NSYNC’s “Tearing Up My Heart” came out closer to the moon landing than to today. E.T. hit theaters closer to the 1930s than to today. And Billy Joel’s “She’s Got a Way” was released nearer to World War I than the present moment.

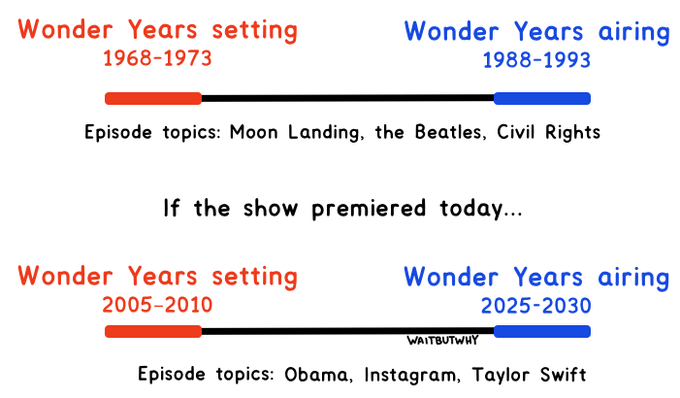

If Back to the Future were released today, Marty would be heading back to the ridiculously retro year 1995. His teenage parents would be doing hilariously old things like talking on big cell phones and hanging out in AOL chat rooms. And of course, no existential time crisis would be complete without The Wonder Years. The show aired from 1988-1993 and took place in the years 1968-1973. If the show debuted today, it would be set in 2005-2010 and cover nostalgic old things like Obama’s election, Instagram like counts, and Taylor Swift concerts.

___________________________________

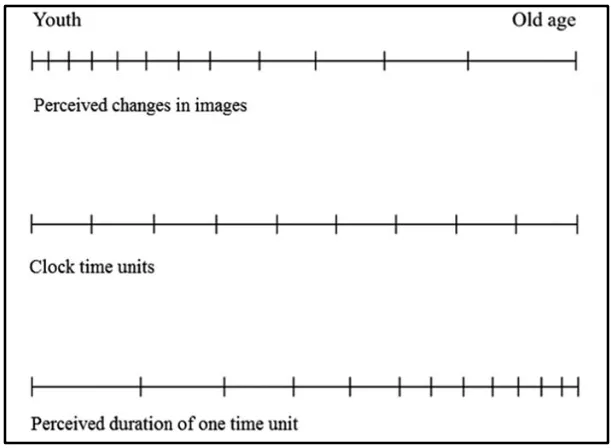

How to change our perception of time. Say the average lifespan is 80 years old. Then consider that time feels like it moves faster as we age. At age 40, the average person may be 50% through their biological life but they may have experienced 75% of what the brain will ever experience.

When you are looking back at the end of a childhood summer, it seems to have lasted for such a long time because everything was new. But when you’re looking back at the end of an adult summer, it seems to have disappeared rapidly because you haven’t written much down in your memory. So here is the take-home lesson. We have to seek novelty because this is what lays down new memories in the brain.

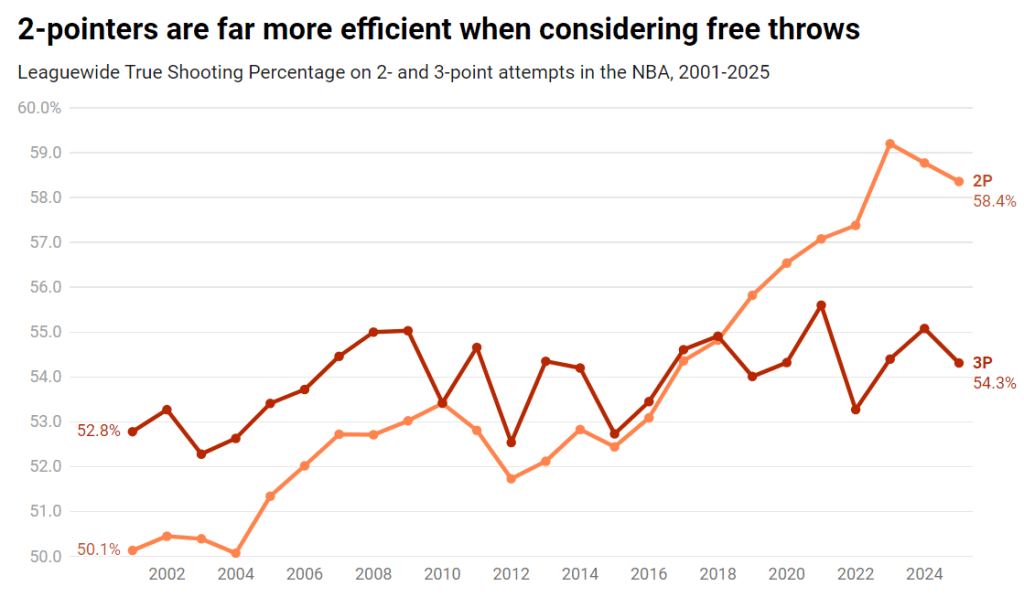

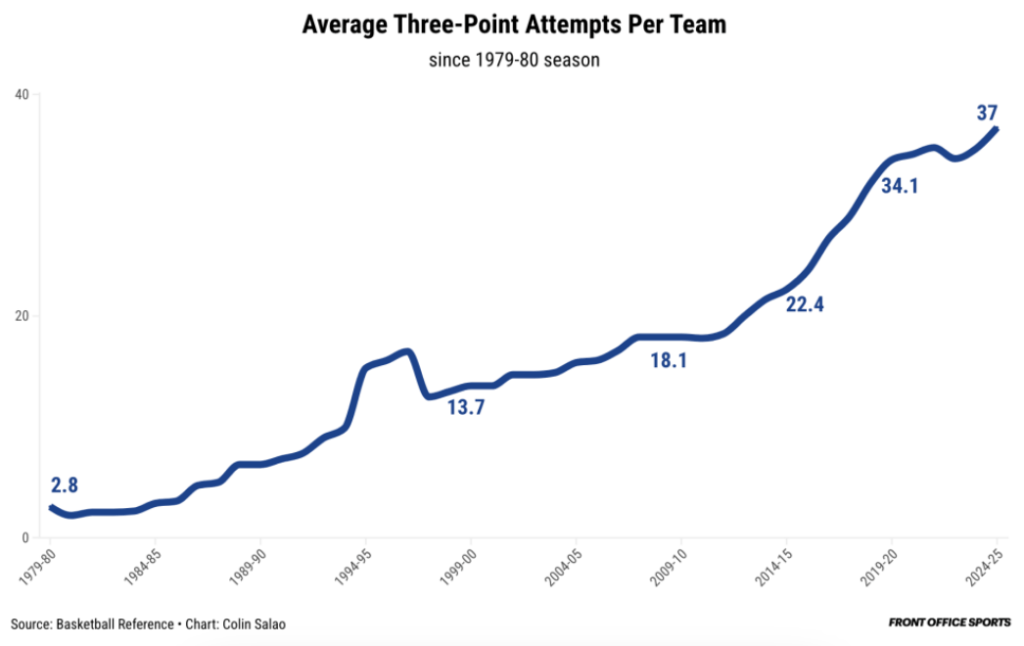

The argument for more NBA threes has always been the same: it’s math. The simple fact is that teams need only shoot 33 percent on 3-pointers to break even (in terms of points per shot attempt) against 50 percent on 2-pointers. But nothing stays static for long in professional sports. As the league’s brain trusts encouraged more and more threes, the efficiency of each shot type changed — and while 3-pointers have averaged a relatively steady level of points per field goal attempt for nearly two decades now, the 2-pointer has rapidly become more efficient, to the point that it has caught up to (if not surpassed) the efficiency of a 3-pointer:

This is even more the case when we consider that it’s much easier to get fouled attempting a 2-pointer than a 3-pointer.

Indian Americans own about half of all motels in the United States. Of them, 70% have the last name Patel.

People know whether or not they want to buy a house in just 27 minutes, but it takes 88 minutes to decide on a couch.

About 25% of the decline of casual sex among young men since 2007 can be explained by video games.

It takes twice as long to cook a chicken today compared to 100 years ago because twenty-first century chickens get less exercise.

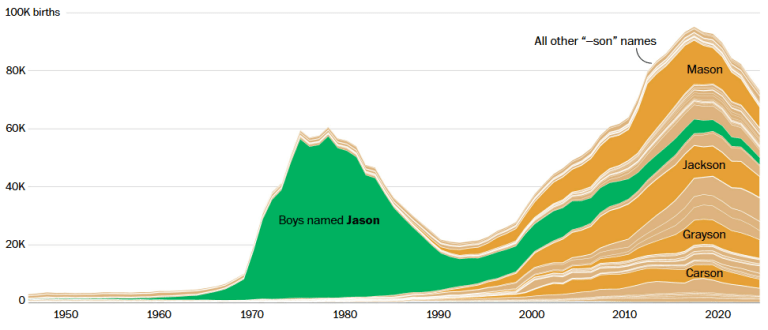

American baby names trends shifted from family names a century ago to popular names a generation ago to popular endings today. A generation of people named Jason has given way to babies with -son endings: Mason, Jackson, Grayson, and Carson. Today, 48% of the top 500 baby names share only ten endings.

________________________________________

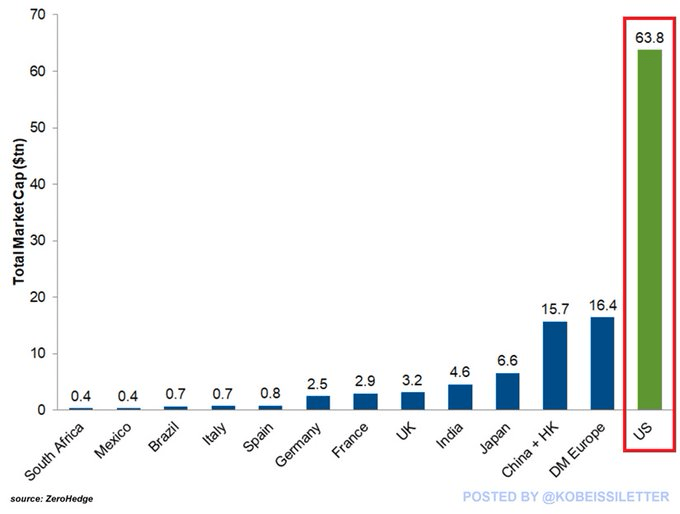

The U.S. stock market is now worth $64 trillion and rising by the hour.

The market cap has doubled in less than 5 years, and it added $10 trillion alone in 2024.

China, Hong and all of Europe’s stocks combined are now worth less than 50% of U.S stocks.

The U.S. Magnificent 7 alone are worth more than every single company in all of Europe.

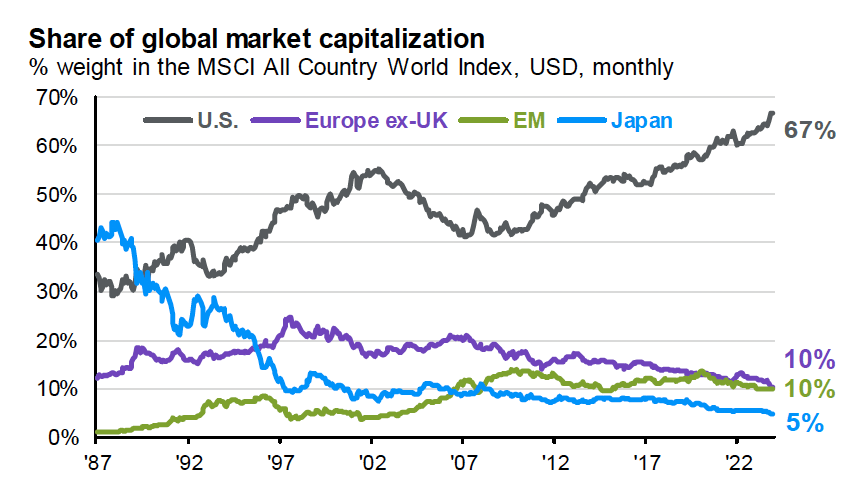

Zooming out to look at how we got here:

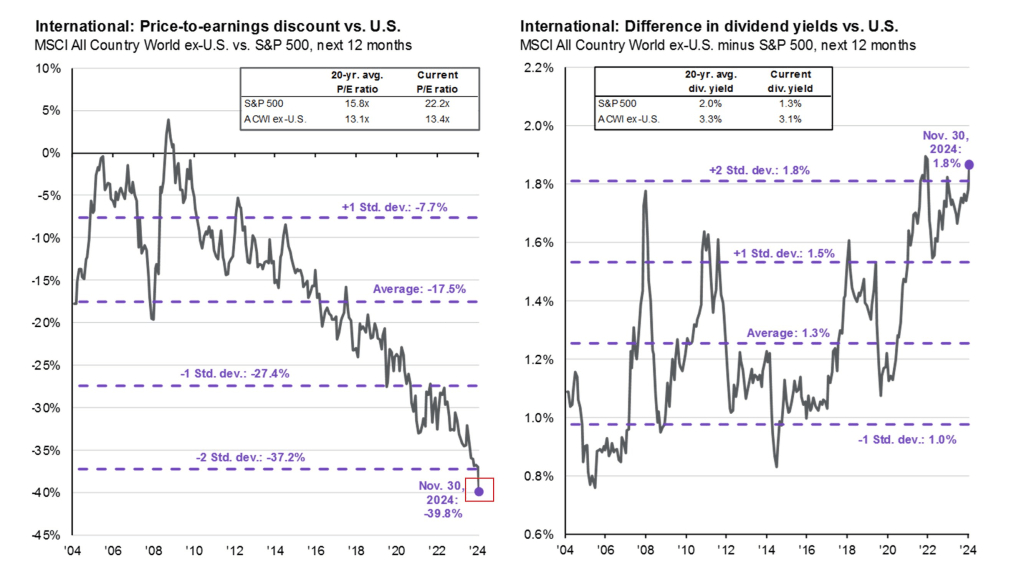

Dividends and share buybacks (total shareholder yield) in Europe and Japan are far more attractive than the U.S. A major reason for this is because you are paying an extraordinarily high price in U.S. stocks (vs. the rest of the world) for the yield you receive in return:

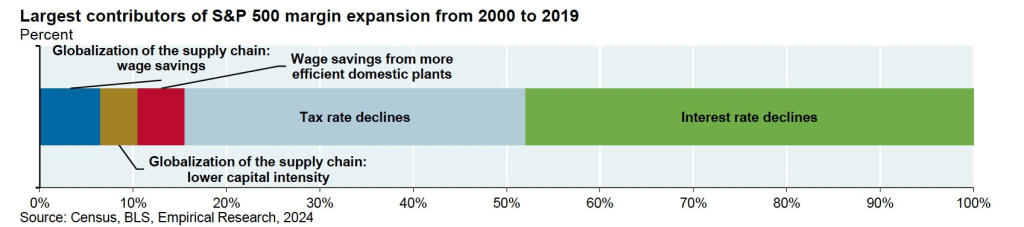

The largest contributors to the S&P 500’s (profit) margin expansion have come from taxes and interest rates declining. Let’s hope the U.S. government continues to have unlimited borrowing power at low interest rates to continue that trend forward:

U.S. Equities (letter to clients on January 2, 2035):

First, it turns out that investing in U.S. equities at a CAPE in the high 30s yet again turned out to be a disappointing exercise, Today the CAPE is down to around 20 (still above long-term average). The valuation adjustment from the high 30s to 20 means that despite continued strong earnings growth, U.S. equities only beat cash by a couple of percent per annum over the whole decade, well less than we expected.

International Equities (letter to clients on January 2, 2035):

Of course, after being left for dead by so many U.S. investors, the global stock market did better with non-U.S. stocks actually turning in historically healthy real returns (like 5-6% per annum over cash). It turned out that, just as we thought, the U.S. really did have the best companies (most profitable, most innovative, fastest growing) and this indeed continued in this last decade. But it also turned out that paying an epic multiple for the U.S. compared to the rest of the world mattered somewhat more than we thought, and international diversification, as we knew it would one day, did eventually work. It turns out there was indeed a price at which European stocks made sense. That was news to us. Luckily, we removed non-U.S. stocks from our benchmark back at the beginning of ’25 so this differential did not affect our benchmark-relative performance this last already painful decade, only our, well, you know, actual performance.

10 great lessons learned in 2024 including: walk more, meet in person, things take longer than you realize, and we overweight risk but underweight exponential outcomes (the value of asymmetric bets).

In individual sports the best players might have coaches, trainers, agents, and others supporting them, but in matches or tournaments it’s one player versus another, or one player versus the world. The player gets the credit for the win, and the player gets the blame for the loss. It’s why individual sports are agonizing even for the best in the world. Stock picking is an individual sport. You have no place to hide. The outcome is focused on you. It makes the wins intoxicating. Losing is excruciating. When stocks go down, we stop looking in the mirror and start blaming everything and everyone else.

____________________________________

Odometer fraud is shooting up: According to the latest data from CARFAX — 2.14 million cars may have had odometer rollbacks in 2024 — up 82,000 from last year and 18% since 2021. The reasons? Technology has made rolling back an odometer easier than ever — and is often done to dodge lease mileage fees or artificially inflate a car’s value. It takes seconds to do and costs the next buyer an average of $4,000 in lost value. Bottom line — if a “low-mileage” car deal seems too good to be true — it just might be.

_____________________________________

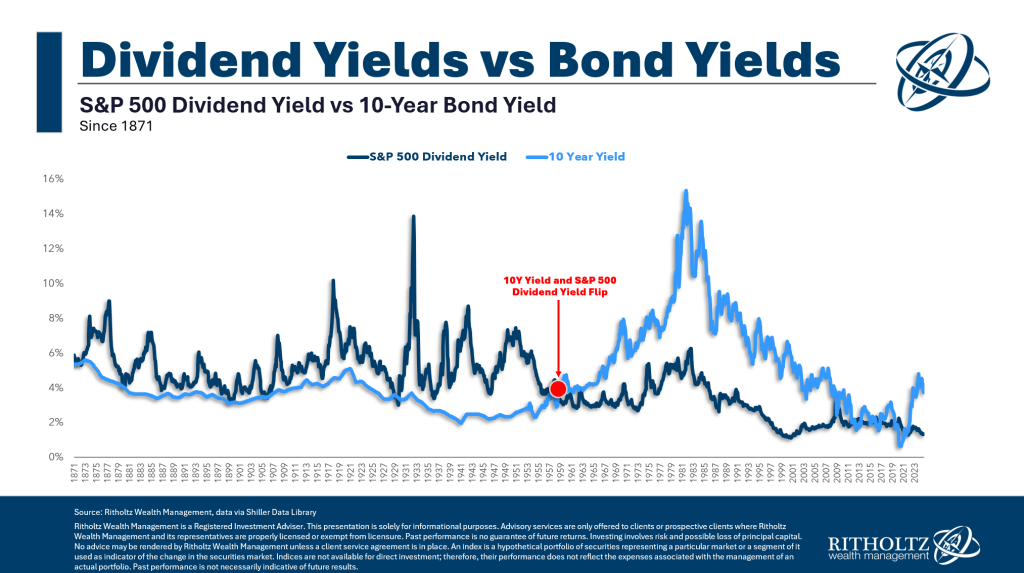

Until the 1950s, investors expected to earn more income from their stocks than bonds. The general idea was that stocks are riskier and thus need higher yields to attract investors. When dividend yields and bond yields converged it was a signal to sell stocks. Stock prices would then fall until dividend yields earned a premium over bonds again. It was a pretty good market signal too. The yields on stocks and bonds flipped for a month or two right before the Great Depression and many of the biggest bear markets of the late 19th century and early 20th century. But then a weird thing happened in the late-1950s…it stopped working. Bonds yields surpassed divided yields and didn’t look back for a very long time. In fact, they remained above stock market yields for 50 years until bond yields finally got low enough during the Great Financial Crisis.

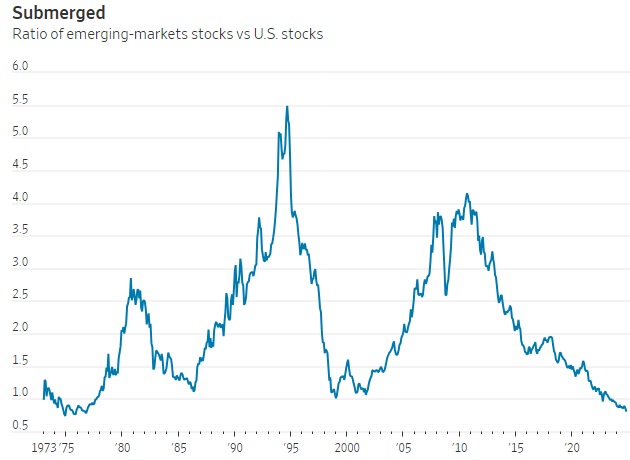

The ratio of emerging market stock performance relative to the United States is now at an all-time low:

Foreign investors have piled into U.S. stocks like never before. Foreign investors now allocate a record 59% of their assets to US equities. The share of US stocks in foreign financial holdings is now ~7 percentage points higher than it was at the 2000 Dot-Com Bubble peak.

Once you internalize a simple truth: that all behavior makes sense with sufficient information, the world looks a lot less crazy (although infinitely more complex). The problem is we rarely have access to the full set of variables driving someone’s decisions. Understanding this is not just an intellectual exercise. It’s a model for navigating the social, financial, and professional realms with insight to make sense of the world and get better outcomes from our teams and users, even have better relationships. In social contexts every interaction is imbued with subtext. Many assume others operate under the same rules they do, but each person carries a unique script shaped by their experiences and values. Instead of asking, ‘why are they acting like this’ we can try, ‘what might I not know about their world?

_________________________

Stocks don’t know that you own them. The market is never out to get you. When you personalize the market’s moves, you fall into the trap of trying to be right rather than trying to make money. Constantly worrying about outcomes that are completely out of your control, especially in the short term, is asking for trouble from Mr. Market. It’s bad enough that investors get dinged in their pocketbooks when they take losses. Don’t compound the issue by letting your ego make things far worse. You have to invest in the markets as they are, not as you wish them to be.

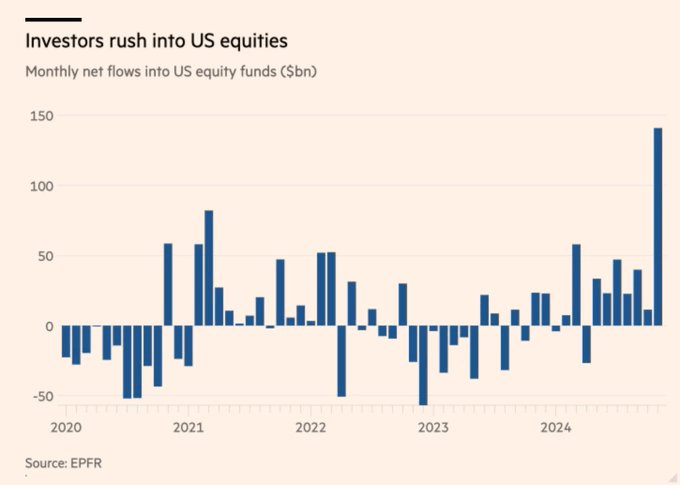

The monthly inflows into U.S. stocks in November were the highest since the peak of the tech bubble in 2000.

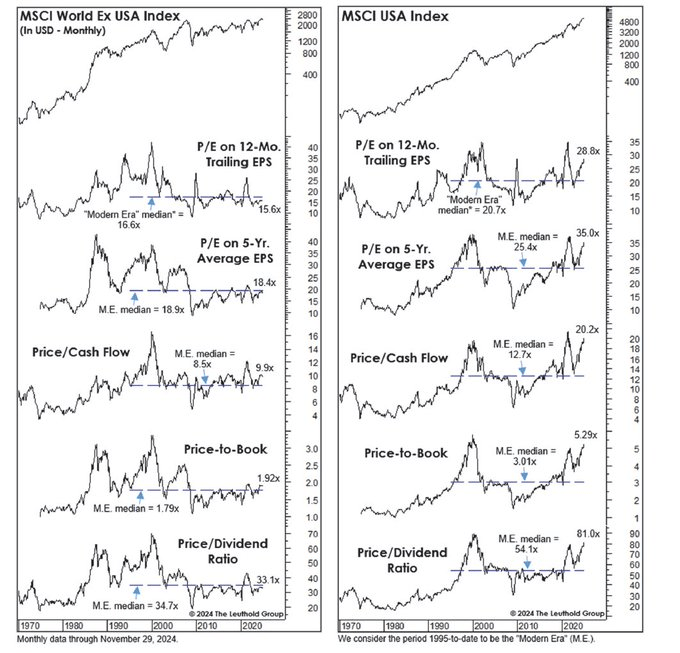

12-month forward P/E ratios relative to the last 20 years. The U.S. is off the chart expensive, even when including Wall Street analysis aggressive “forward” (estimates) of earnings over the coming year.

No matter how you measure it, foreign stocks trade at half the valuation of US stocks:

It’s not just multiple expansion that created the outperformance. The U.S. also experienced much stronger earnings vs. the rest of the world over the last 15 years (the denominator in the P/E ratio):

The percentage of respondents that expect U.S. stocks to rise over the next 12 months. New record-shattering levels of bullish excitement:

The market cap (price investors are paying to own the U.S. stock market) is rising much faster than the profits relative to the rest of the world:

Jonathan Haidt wrote one of the most important books of the year, The Anxious Generation, about how toxic and destructive social media is on children’s lives. His other major focus of the book is how much it helps young kids to have the ability to play freely without adult supervision.

Treat cognitive context shifts as “productivity poison.” The more you switch your attention from one target (say, a report you’re writing) to another (say, an inbox check), the more exhausted and dumber you become. Focus is like a superpower in most knowledge work jobs. Train this ability. Protect deep work on your calendar.

Your phone should be used as a tool, not a constant companion. To accomplish this: (1) keep your phone plugged into the same spot when at home (instead of having it with you); and (2) remove all apps from your phone where someone makes more money the more you use it. Most people don’t need to use social media. If you really need to use it — e.g., for professional purposes — use it on a web browser on your laptop, and spend at most an hour a week logged in, as that’s enough for 99% of legitimate uses. There are better ways to be entertained, find news, and connect with people. Kids under the age of 16 shouldn’t have unrestricted access to the internet. Their brains aren’t ready for it.

In building a meaningful and fulfilling life, it’s usually better to work backwards from a broad vision of your ideal lifestyle than it is to work forward toward a singular grand goal (e.g., a “dream job” or radical location change) that you hope will make everything better.

Generative AI won’t really change our daily lives in a massive way until it leaves the chatbot format and becomes more integrated into specific tools. The biggest technology story everyone is ignoring is the end of screens. Within the next decade, AR glasses will replace essentially every screen currently in our lives — phones, laptops, tablets, computer monitors, and televisions.

_____________________________

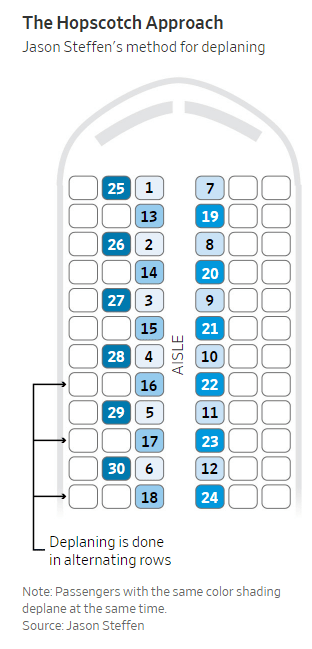

Jason Steffen, an astrophysicist and associate professor at the University of Nevada, Las Vegas, has studied the most efficient way to board a plane. That method involves boarding passengers in alternating rows. In one version, you begin with the traveler sitting in the window seat of the last row of the plane. The next person boards two rows away, and so on, switching between each side of the plane, and working from the window to the aisle seat.

Have we reached peak PreCheck? With more than 40 million people enrolled in the government’s Trusted Traveler program, passengers are wondering whether the expedited security program has become too popular – and too slow.

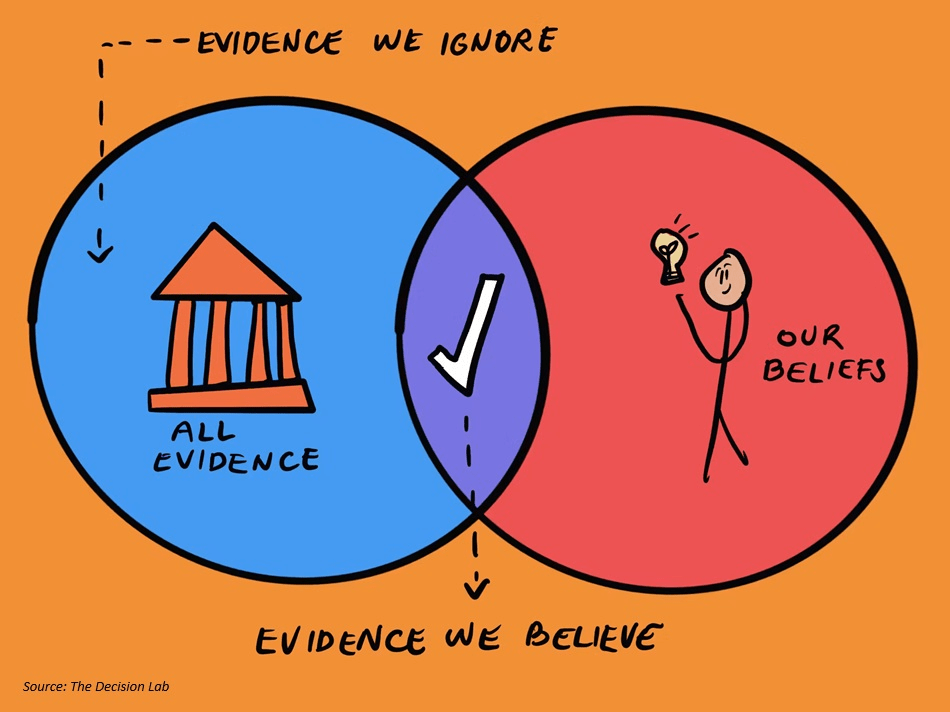

Confirmation bias is a deeply human tendency to favor evidence that supports what we already believe while ignoring or downplaying evidence that contradicts it, even when the consequences are expected to be terrible. In simple words, it’s like wearing special glasses that only let us see what we want to see. When we believe something, our brain naturally looks for information that proves we’re right and ignores anything that suggests we might be wrong. There are numerous ways this negatively impacts us with investing.

The anti-foreign-stock drumbeat has grown louder with each additional year that international markets underperform U.S. shares. Indeed, even though foreign stocks beat U.S. shares in the 1970s, 1980s and 2000s, there are folks today who argue there’s no reason to own foreign shares. Before you throw in the towel, ask yourself six questions:

1. If U.S. stocks had lousy returns for 15 years, would you abandon them?

2. If U.S. multinationals are a good substitute for investing abroad, why don’t they perform like large-cap foreign stocks?

3. Yes, foreign companies offer fewer legal protections and greater business risk. But isn’t this already reflected in share prices?

4. If foreign stocks are riskier, shouldn’t they offer higher returns?

5. If you’re an indexer happy to hold U.S. stocks according to their market value, shouldn’t you also be willing to allocate among countries on the same basis?

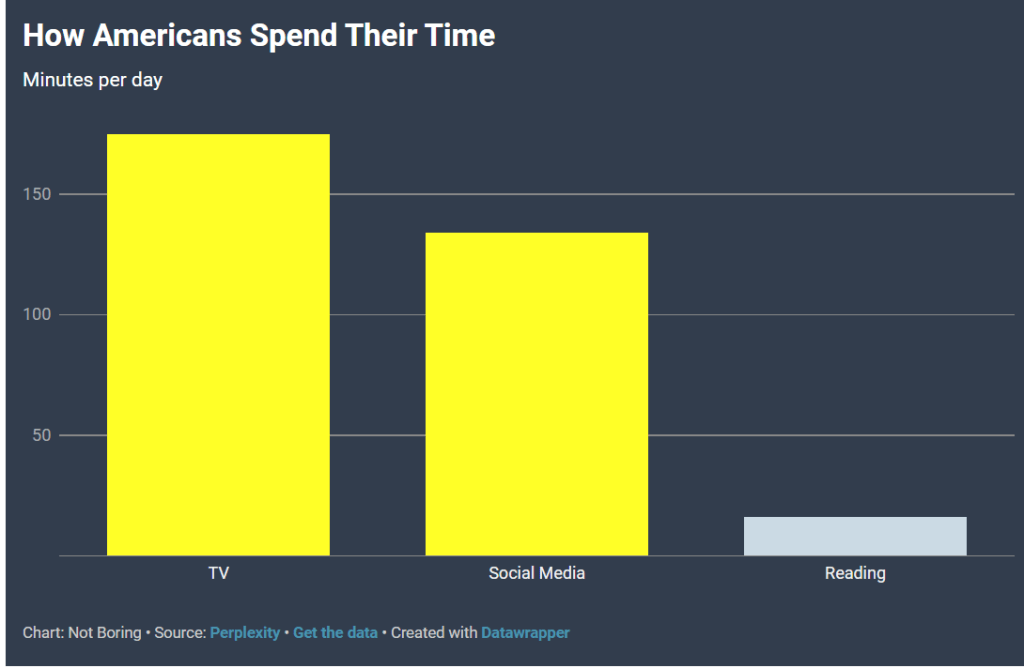

Americans aged 18 to 34 watch less than five hours of live and timeshifted TV per week.

50 percent of 18 to 24-year-olds in the U.S. say that they don’t watch any traditional TV!

At the other end of the scale, those aged 65 and older watch more than 40 hours on average.

________________________________________

The last time emerging markets were doing this badly the term “emerging markets” hadn’t been coined yet. That spells opportunity, and the greatest spoils might go to those investors who are the boldest and also willing to look past that poorly defined category. Emerging markets outperformed developed market stocks in the century’s first decade as commodity prices boomed and the tech and housing bubbles dented the U.S. market. Today, though, they are much cheaper as a multiple of earnings.

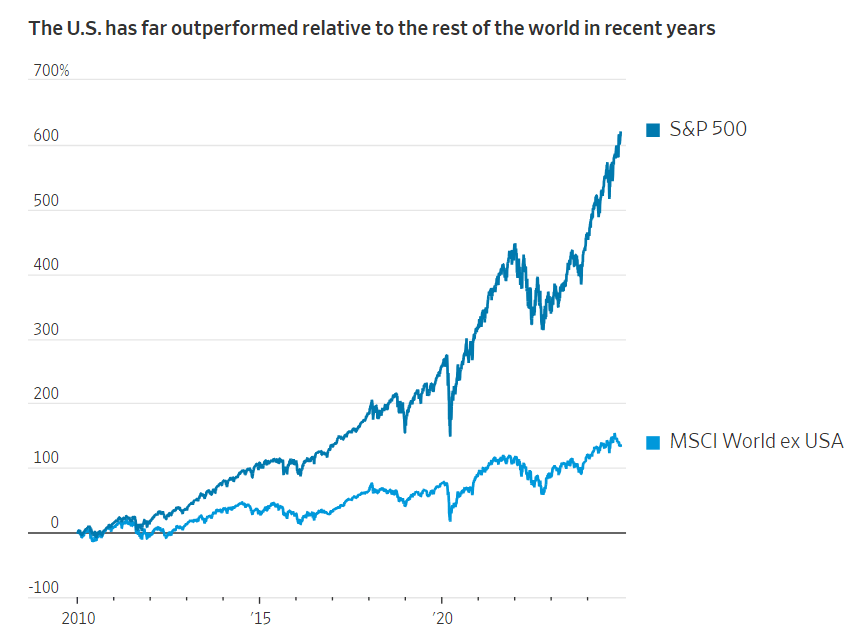

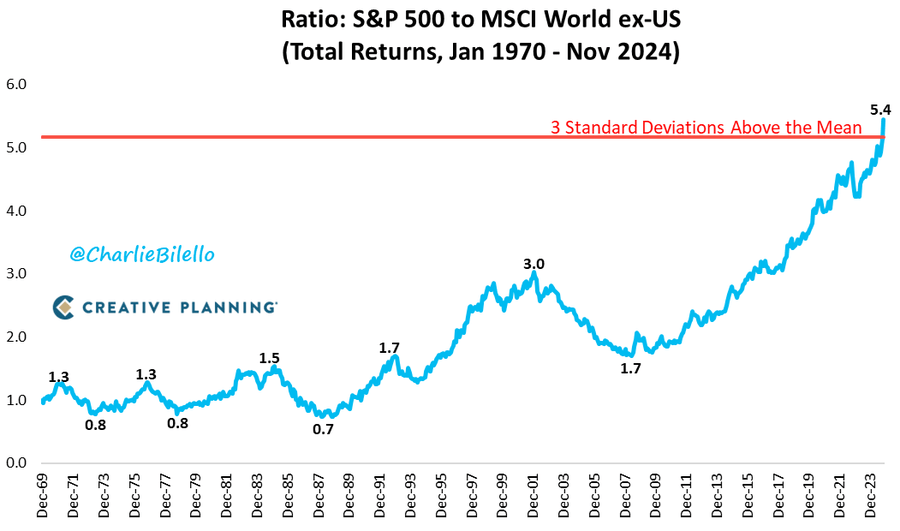

US stocks have been outperforming international stocks for 16 years running, and by a huge margin. The result: we’re now more than 3 standard deviations above the mean in terms of historical US outperformance.

A study found that A.I. chatbots defeated doctors at diagnosing illnesses, even the test group of doctors that were using a chatbot for assistance. ChatGPT-4, from the company OpenAI, scored an average of 90 percent when diagnosing a medical condition from a case report and explaining its reasoning. Doctors randomly assigned to use the chatbot got an average score of 76 percent. Those randomly assigned not to use it had an average score of 74 percent. The study showed more than just the chatbot’s superior performance. It unveiled doctors’ sometimes unwavering belief in a diagnosis they made, even when a chatbot potentially suggests a better one.

___________________________

The only thing worse than not making life-changing money is losing the life-changing money that you just made. Why is it so hard to hold on to the money we made? Because hitting a home run on an investment is euphoric. And beyond the dopamine rush, it strokes your ego, making you feel smart. Those good feelings cloud your judgement. Financial returns are a seductive feedback mechanism. When something you invest in goes up by a lot, you feel like a genius, and you want to experience that rush again. And because your last bet was correct, you grow more confident, so you decide to double down on another trade.

$500,000 Pay, Predictable Hours: How Dermatology Became the ‘It’ Job in Medicine. Americans’ newfound obsession with skin care has medical students flocking to this specialty. Medical residency applications for dermatology slots are up 50% over the past five years, with women flooding the zone. Dermatologists earn a median $541,000 a year. Pediatricians, by contrast, earn a median $258,000 annually. Given the infrequency of skin emergencies, far fewer dermatologists are on call at night and on weekends.

______________________________

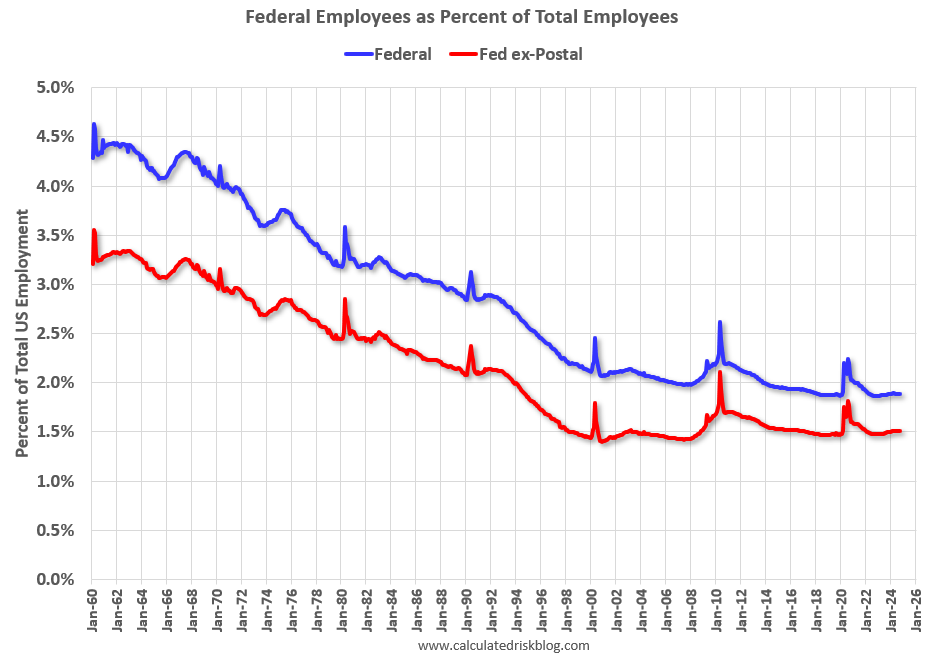

The new administration is talking about cutting the number of federal government employees. Federal employment was around 4.3% of total employment in 1960 and is now down to only 1.9%.

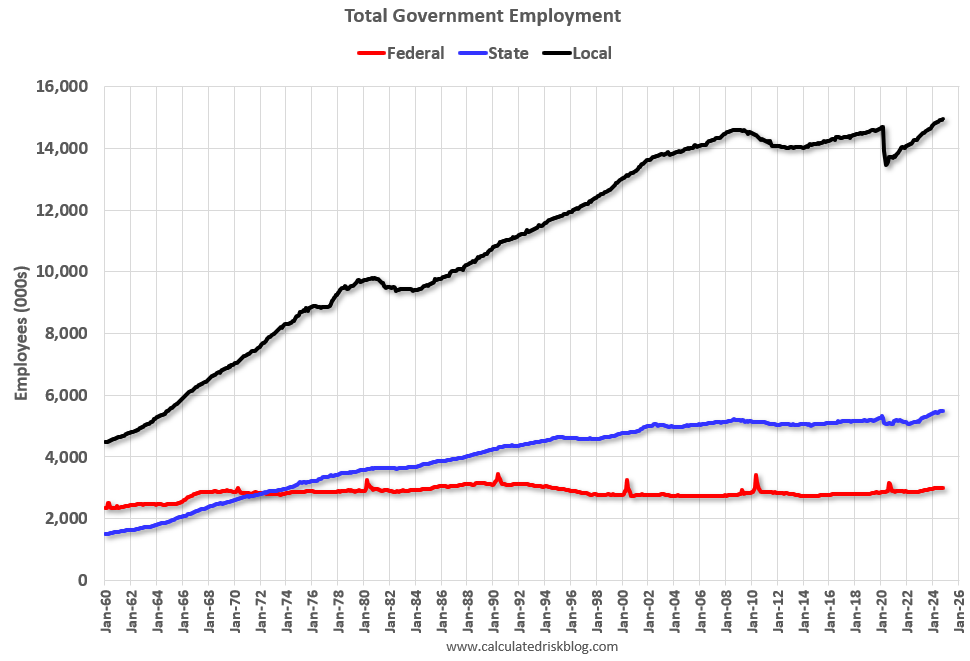

Most government employees are local (police officers, fire department, etc), followed by state employees. Approximately half of the state and local employees work in education (teachers!)

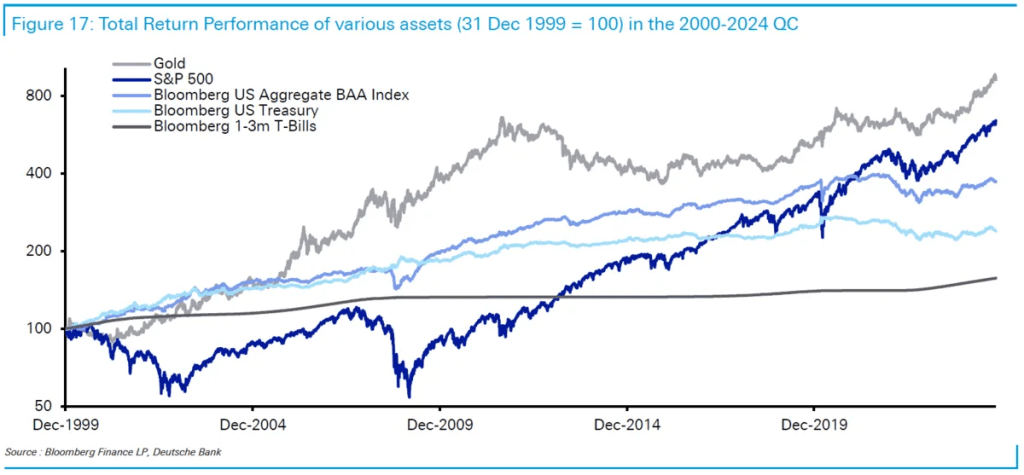

Should investors just give up on stocks outside America? Suppose you had invested in an index of American shares at a trough in 2009 and held on to it until today. Your portfolio would now be getting on for triple the size it would have been if you had instead picked a basket of stocks listed on the old continent (see chart below). Just about whenever American share prices crashed, European ones fell about as far or further; when American prices rocketed, European ones trailed them.

Investors greeted Donald Trump’s re-election by sending American share prices to record highs. European stocks have dropped by 4% since the morning of the result, and by 5% since a peak in September. They are not alone—stocks in much of Asia fell alongside them.

Firms listed in America now constitute nearly two-thirds of the value of MSCI’s broadest index of global stocks. American companies are valued eye-poppingly higher, relative to earnings, than non-American ones. The difference is often justified by their fatter profit margins, better management and stronger growth. Fair enough. However, another way of looking at the valuation gap is that, in order to get from earnings to share prices, the market scales them up by radically different multiples based on whether they are made inside or outside America. This is peculiar, and much harder to justify, suggesting that valuations may have fallen out of whack and may eventually be subject to a correction. With American shares more expensive than at almost any other time in history, that would hardly stretch belief.

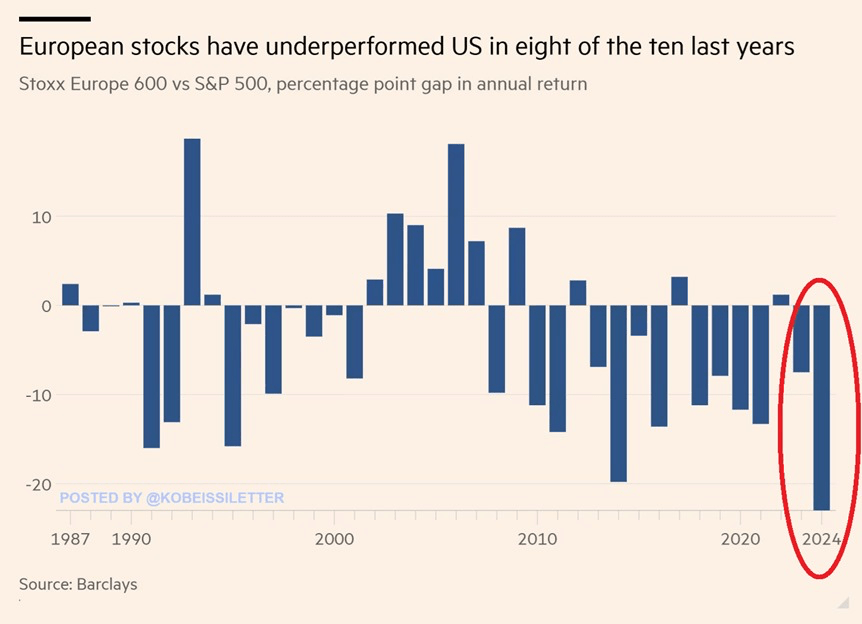

The Stoxx Europe 600 index has underperformed the S&P 500 by 21% this year, the most on record.

This comes as European stocks have returned only 3% year-to-date much below the 24% gain of US stocks.

The Stoxx Europe 600 index is now on track for its 8th year of underperformance out of the last 10.

Over the last decade, European equities have increased by just 50% much less than the S&P 500 return of 187%. As a consequence, the US stock market is now 4 TIMES larger than Europe.

In my psychotherapy practice, I have seen more and more people whom I call “Unhappy Achievers”—people who regularly achieve what they strive for, but still feel anxious, depressed, and empty. Those around them may believe they have it all together—and on the surface they do. But inexplicably, deep down, they often feel miserable. Here’s why:

Unhappy Achievers frequently have great jobs, attractive partners, and lifestyles that are the envy of their friends. They may notch win after win, believing the next achievement will finally allow them to relax. But any satisfaction they feel vanishes quickly, and they feel more compelled than ever to start on the next attempt to impress. Many Unhappy Achievers are socially successful and appear outgoing. They may even be seen as the “life of the party.” But they secretly feel exhausted when they’re surrounded by people and can only truly relax when they’re alone.

On top of this, Unhappy Achievers are often embarrassed to admit that they are struggling. Who could blame them? With so many people striving for material and professional success, who wants to admit that they feel unhappy, even anguished? And because it’s so counterintuitive, I’ve found that almost none of these Unhappy Achievers can make sense of why they feel the way they do. Too often, they feel that there’s simply something shameful and broken about them. And that makes them feel lonelier.

________________________________

There is ample evidence that memories are not saved in our brains but reconstructed whenever we need them. This is a very dynamic and highly flawed process and prone to a lot of errors. People can implant false memories in other people with relative ease, particularly if they are trusted members of their social circle. Indeed, our memories are so flawed that the value of eyewitness testimony in court trials is by now much diminished because we know how unreliable such testimonies are. One can influence memories even with perceived friends that one has never met.

As a hospice nurse, Julie McFadden spends her days caring for people near the ends of their lives. The job gives her a window into the regrets people most commonly express on their deathbeds, which she says offers insight into how people can live better, more fulfilling lives. McFadden says she hears these regrets most often from her hospice patients:

They wish they’d appreciated their health when they had it. “They didn’t understand how lucky they were to have a healthy body,” McFadden says. “That’s the No. 1 thing I hear.”

They wish they hadn’t worked their life away. Some people worked intensively throughout the years leading up to their retirement, leaving them with limited time to appreciate life.

They regret how they navigated their relationships. Her patients frequently expressed misgivings over not saying sorry when they should have, not reconnecting sooner to their estranged family member or friends.

They regret caring too much about what people thought. Not living the life they wanted, but living the life people around them wanted.

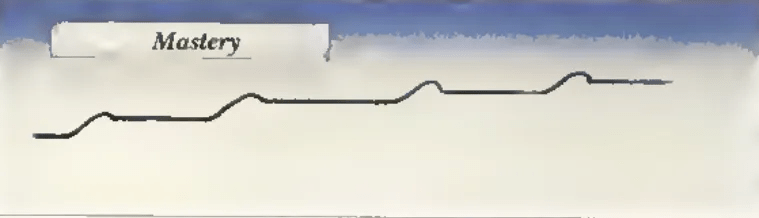

Life and business growth are often misunderstood. Many people envision progress as a straight, upward trajectory—steady, predictable, and consistent. But in reality, growth is non-linear. It is defined by long periods of minimal change or slow progress, where it may feel like little is happening. These are the periods of preparation, learning, and process—the times when the foundation for future success is quietly being built.

Then come the spikes: the moments of significant wins that redefine everything. In business, it might be a major sale, a breakthrough partnership, or an idea that suddenly scales. In life, it could be the birth of a child, meeting a lifelong partner, or a moment of clarity that changes your path. These “big wins” seem to happen all at once, but they are the result of the groundwork laid during those slower periods.

Understanding this rhythm is key to staying motivated. The quiet times are not wasted; they are essential. And the spikes, while transformative, only come to those who commit to the process. Growth is not linear—it’s a journey of patience, persistence, and faith in the moments that will ultimately reshape your life.

____________________________________

Data is mounting about the impact our attitudes and beliefs have on our health and longevity. Examining data from the Ohio Longitudinal Study of Aging and Retirement, a survey conducted from 1975 to 1995 that included views on aging; comparing early attitudes with death records, there is a striking correlation: People who reported positive age beliefs early on lived, on average, 7.5 years longer than those who had more negative beliefs. The advantage held even after controlling for age, gender, socioeconomic status, loneliness and health.

____________________________________

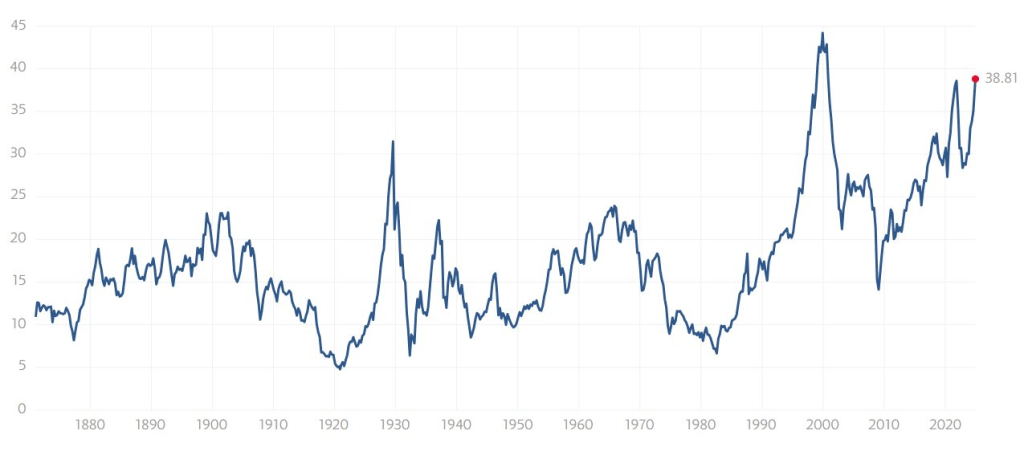

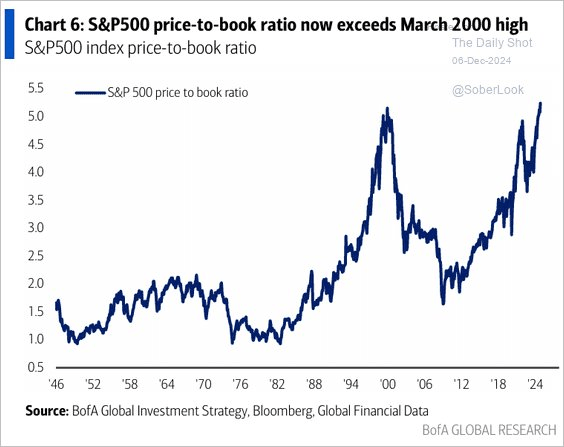

The average P/E ratio of the top 10 largest companies in the S&P 500 is now almost 50. The historical average trailing P/E ratio for stocks is 17.5 (the higher the number, the more expensive stocks are relative to their earnings).

New research shows that it is specific and salient memories that influence our investment decisions rather than the collective memories (aka ‘experience’) we have. It matters for our investment decisions (in the stock market for example) if we have a memory of a good or bad experience investing in stocks. But it also matters if this memory is of a personal experience or a more distant, impersonal memory. If we have personal experiences, it makes us ‘immune’ or rather less receptive to expert advice. We think we know best because we have first-hand experience with the situation.

_____________________________

The internet commoditized information, and the widespread availability of information has devalued it because you can now find some data point, anecdote, or statistic to support any possible viewpoint, creating an environment ripe for echo chambers and false signals, which we saw this election cycle. To cut through those false signals, you have to be careful in deciding which information to look for. You have to ask good questions.

The (Presidential election) polls made the mistake of asking the folks they were surveying who they were voting for, not accounting for inaccurate responses. As a result, they got faulty information. Théo’s method, asking who “your neighbors” are voting for, proved to be more accurate, as it reduced the risk that someone would change their answer to save face (they didn’t want to say they were voting for Trump, even though they were).

If you’re trying to decide if you’re bullish or bearish on a stock, you’ll find a million arguments supporting both stances. If you have a headache, you are only three WebMD searches away from convincing yourself that you’re having an aneurysm. The antidote to this abundance of information is distillation: figuring out which information is important and discarding the rest. But distillation is downstream of interrogation: if you ask the right questions, the information filters itself.

The cost of college is quietly going down. In-state tuition for a public university is down to $11,610 a year, compared to $12,140 a decade ago. After grant aid is applied, the average student would pay $2,480, a decrease from the 2014-2015 school year, when that amount totaled $4,140. For private schools, the net price is $16,510 a year, down from $19,330 back in 2006. Even sticker prices, the cost that is displayed by schools before any aid if applied, have mostly gone down in the last decade. The report said sticker prices in the last decade rose only 4 percent at private, nonprofit schools, decreased 4 percent at public four-year colleges and went down 9 percent at public two-year ones. The report also showed that student debt overall is down. Those graduating in debt with bachelor’s degrees are down 10 percent, or $5,600, from a decade ago, with the average debt among borrowers now at $27,100.

_______________________________

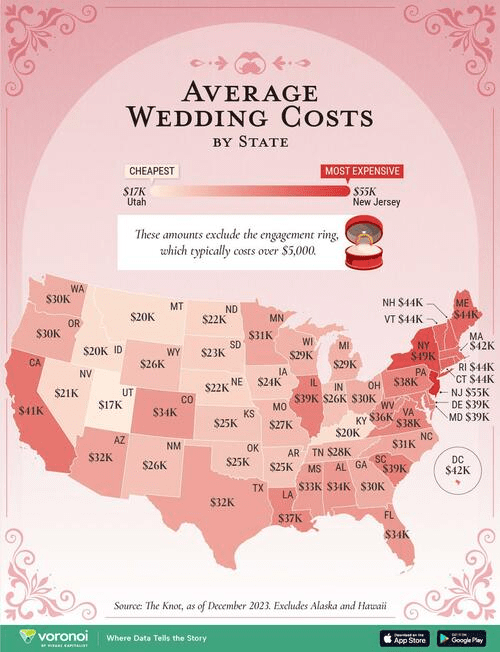

The terrifying average cost of weddings, by state, for any of the fathers of daughters out there:

How risky stocks are to a given investor depends upon which part of the life cycle he or she is in. For a younger investor, stocks aren’t as risky as they seem. For the middle-aged, they’re pretty risky. And for a retired person, they can be nuclear-level toxic. The reason why stocks aren’t very risky for a young person is that you have a lot of “human capital” (the ability to make money working) left. On the eve of retirement, you don’t have any of that. Stop playing when you’ve won the game.