For years, AI had been improving steadily. Big jumps here and there, but each big jump was spaced out enough that you could absorb them as they came. Then, on February 5th, two major AI labs released new models on the same day: GPT-5.3 Codex from OpenAI, and Opus 4.6 from Anthropic (the makers of Claude, one of the main competitors to ChatGPT).

These new AI models aren’t incremental improvements. This is a different thing entirely. And here’s why this matters to you, even if you don’t work in tech.

The AI labs made a deliberate choice. They focused on making AI great at writing code first… because building AI requires a lot of code. If AI can write that code, it can help build the next version of itself. A smarter version, which writes better code, which builds an even smarter version. Making AI great at coding was the strategy that unlocks everything else. That’s why they did it first.

And now they’re moving on to everything else.

The experience that tech workers have had over the past year, of watching AI go from “helpful tool” to “does my job better than I do”, is the experience everyone else is about to have. Law, finance, medicine, accounting, consulting, writing, design, analysis, customer service.

AI is now intelligent enough to meaningfully contribute to its own improvement. It’s now building itself. Dario Amodei, the CEO of Anthropic, says AI is now writing “much of the code” at his company, and that the feedback loop between current AI and next-generation AI is “gathering steam month by month.” He says we may be “only 1–2 years away from a point where the current generation of AI autonomously builds the next.”

Each generation helps build the next, which is smarter, which builds the next faster, which is smarter still.

This is different from every previous wave of automation. AI isn’t replacing one specific skill. It’s a general substitute for cognitive work. It gets better at everything simultaneously. When factories automated, a displaced worker could retrain as an office worker. When the internet disrupted retail, workers moved into logistics or services. But AI doesn’t leave a convenient gap to move into. Whatever you retrain for, it’s improving at that too.

Nothing that can be done on a computer is safe in the medium term. If your job happens on a screen (if the core of what you do is reading, writing, analyzing, deciding, communicating through a keyboard) then AI is coming for significant parts of it. The timeline isn’t “someday.” It’s already started.

Eventually, robots will handle physical work too.

___________________________

In 2007, John Arnold became the youngest American billionaire, and he now focuses on philanthropy. He recently visited China and posted some of his thoughts:

- The speed to add manufacturing capacity is stunning. Permitting takes weeks. A factory making sophisticated equipment is built in 12 months. An auto plant took 16 months from groundbreaking to first production. Slack in labor market makes it easy to staff and flex employment.

- The US and China have significantly decoupled since early 2020. The # of flights between the two countries is down roughly 70%. Two long-term residents I spoke with said the # of American expats is down 50-75% from the peak. The # of Americans studying in China is down ≈90%.

- Universities and government research labs are at least as tightly woven into the startup ecosystem as in the US, and in many cases more so. Their mission and incentive structures explicitly include commercialization, not just research.

- China awards 1.3 million engineering undergraduate degrees each year vs 130,000 in the US.

- Intense competition leads to widespread overcapacity and low profitability across many industries. Once an industry is deemed strategic, provincial governments deploy subsidies and other supports as they compete to turn local firms into hubs and capture the associated jobs.

- I don’t know if Chinese manufacturers will ever make money but I came away not wanting to invest in any manufacturing business in the rest of the world.

- You see American fast food everywhere. There are 12k KFCs (vs 4k in the US), 6k McDonalds, 7k Starbucks, 4k Pizza Huts.

- Tier 2-4 cities are very quiet. Few cars on the road. Don’t see many people. Factory workers live in dorms on campus. Other workers are in gated compounds that are self-contained neighborhoods. Food delivery and e-commerce have replaced dining out and shopping.

- China is one of only handful of countries with highly educated workforce, robust access to capital, and strong entrepreneurial culture. Only the US and China meet those conditions and have scale.

- As industries become more complex, scale matters more than ever. Large countries can fund frontier R&D, support dense talent markets, amortize infrastructure, and create robust supply chains. Few countries can be cost competitive in high value-add manufacturing.

- While the supply chain on transmission and grid infrastructure is backed up in the US, there is spare capacity in China.

- A security check including bag x-ray is required to enter subway stations, at least in major cities. It’s interesting that most Western countries that are more dangerous do not do this, presumably for speed and cost.

- There were fewer cranes than I expected, presumably reflecting the collapse of China’s real estate market.

- Lower density cities still had most housing in high-rise residential buildings, usually built in complexes of 10-50 identical buildings. I guess it’s the most practical way to house people in a city growing quickly but the aesthetic damage is real.

- Robotic coffee shops are taking off in China first even though wages are much higher in the US.

_____________________________

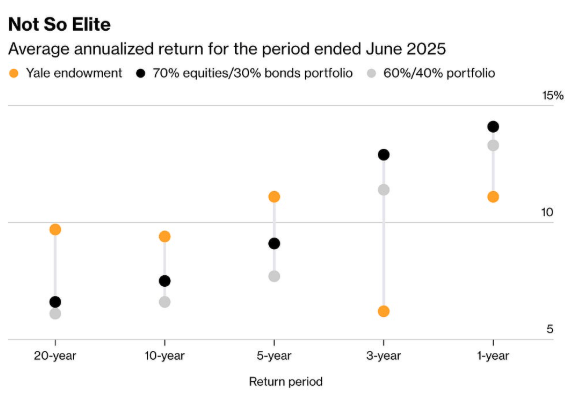

The Yale model, investing in private companies, worked in the ’80s and ’90s for one simple reason — there wasn’t a tidal wave of capital chasing deals. Buyouts were done at reasonable entry prices.

Today, small and mid-size businesses are being acquired at sky-high valuations, often with little margin for error. High entry prices make outsized returns harder to achieve (even with leverage, even with financial engineering).

____________________________

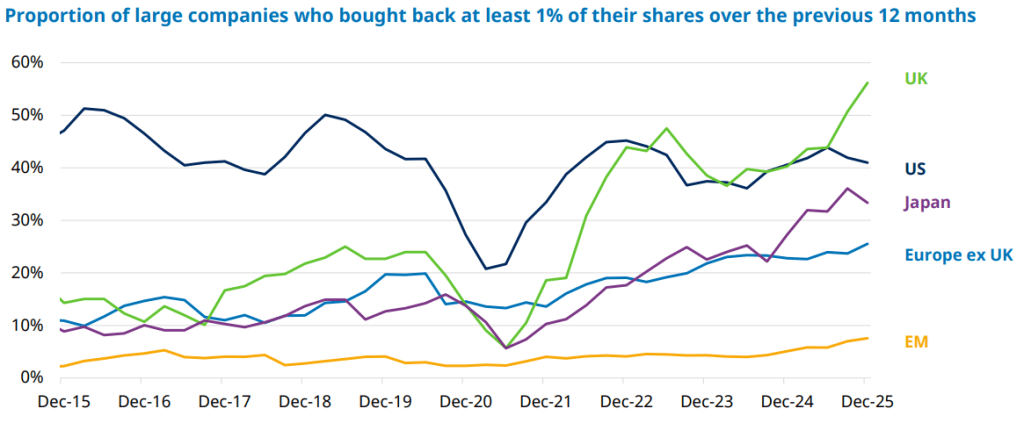

Europe and Emerging Market countries have not embraced stock buybacks, yet.

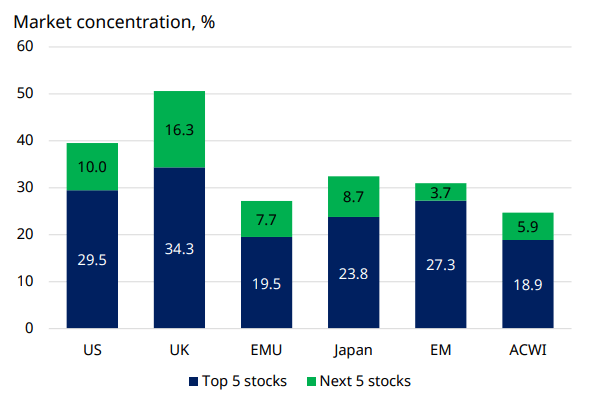

Market concentration for the largest stocks is everywhere in the world, not just the United States:

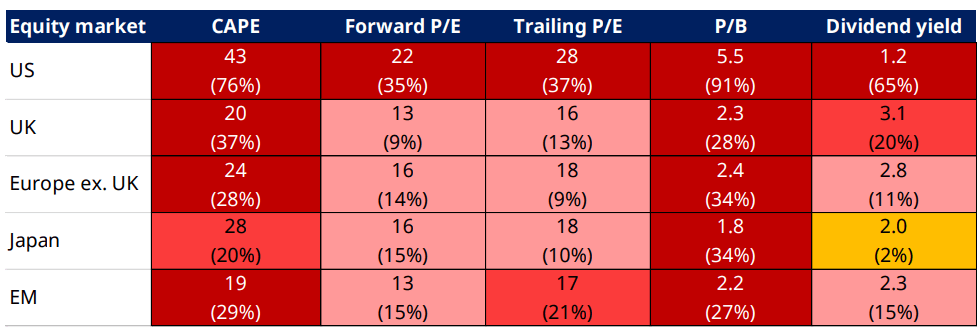

U.S. valuations are still well above the rest of the world, even as the rest of the world outperformed the U.S. in 2025:

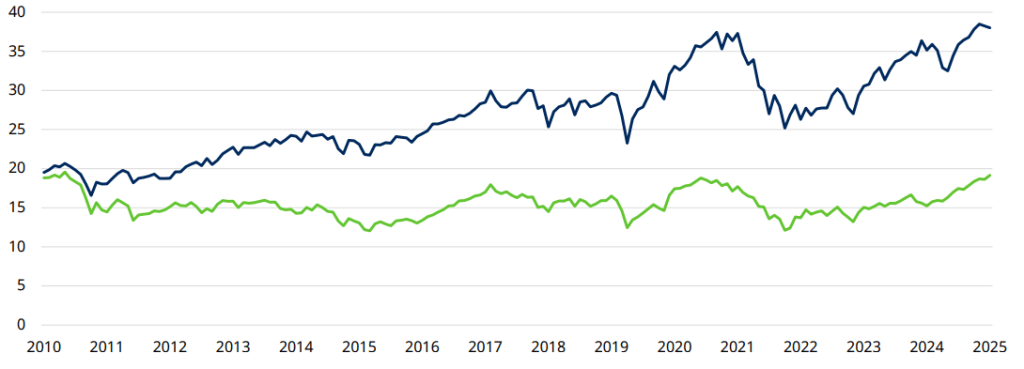

The CAPE ratio of the U.S. vs. the rest of the world:

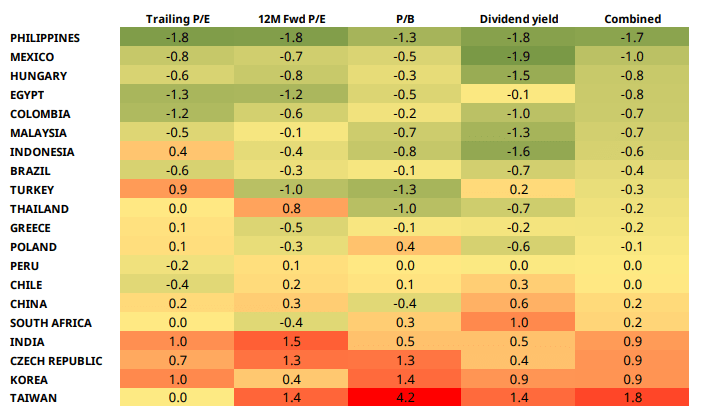

Most emerging market countries are still extremely cheap, but some have moved into the more expensive red zone:

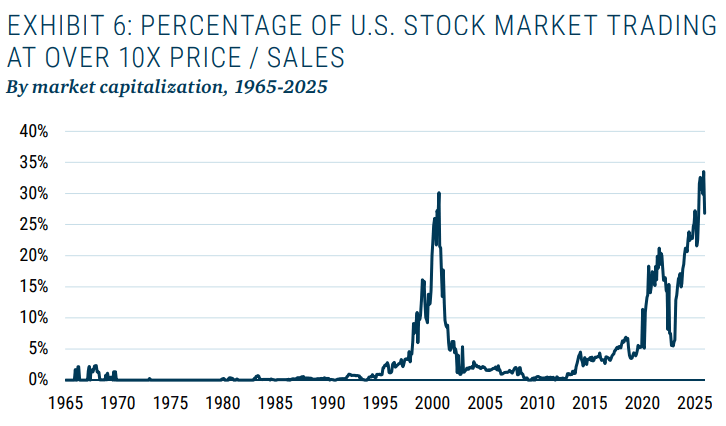

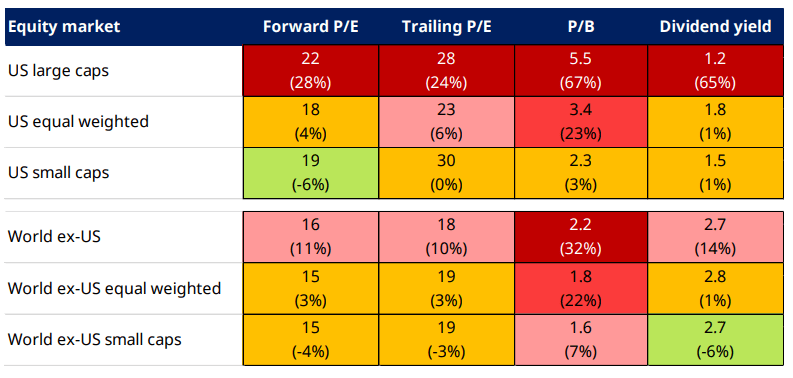

Within the United States, it’s the large cap stocks that are extremely expensive:

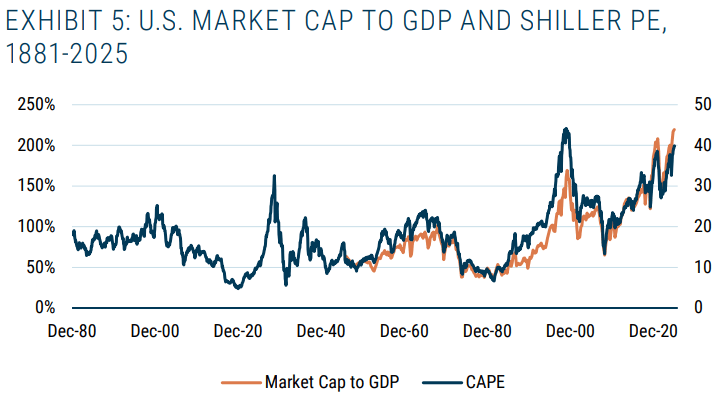

Another valuation metric in historical comparison: