In some ways I’m as productivity-obsessed as ever. What’s changed, and it’s a big change, is that I no longer take myself to be en route to some final state in which I’ll have discovered the best system, and can feel good about myself at last.

I’m convinced it’s a balm for much of what stresses us out: “the compulsion to closure,” which is the hope that all of this is leading up to some kind of permanent resolution. It isn’t. It’s better than that: you get to just be here, and do stuff.

The lack of resolution feels like a problem that needs solving. But have you considered the possibility that the only problem is your belief that such tensions might ever get resolved?

Living without hope of resolution is liberating because it removes a terrible weight from your actions and decisions – the weight that arises from the feeling that they must always be moving you toward some settled state. (Which often just leads to procrastination, since you’re unsure which action would be most helpful for getting you there.)

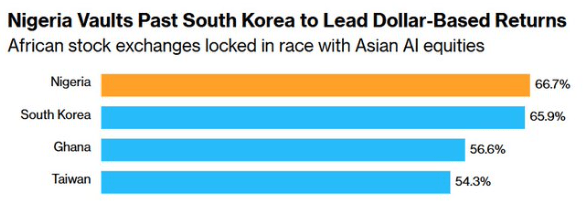

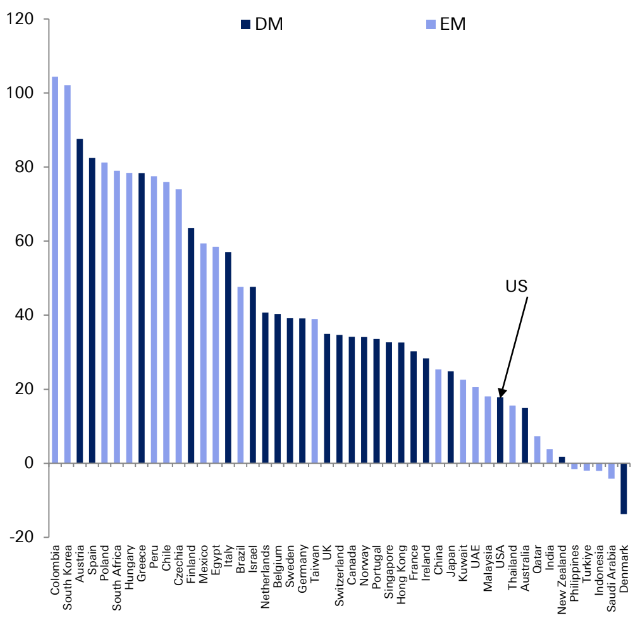

Nigeria now has the best performing stock market in the world, taking the lead over South Korea. As of the end of 2025, there were over 5,000 ETFs, mutual funds, and CEFs that focused on U.S. stocks. There used to be one ETF that invested in Nigerian stocks, but it closed back in 2023 because no one owned it.

__________________________________

2025 Returns:

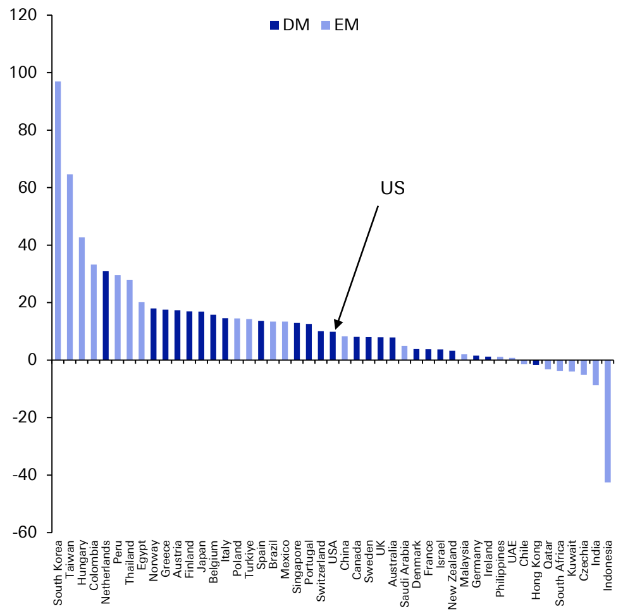

2026 Returns:

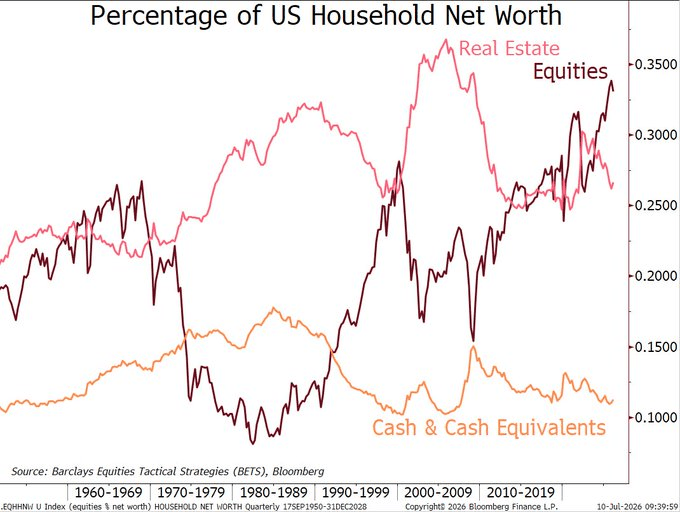

As U.S. stock prices continue to rise into the stratosphere, the percentage of U.S. household net work in stocks (equities) is higher than any point over the last 80 years.

The difference between forward earnings earnings (where analysts project S&P 500 stocks’ earnings will be a year from now) and trailing earnings (what S&P 500 stocks’ earnings actually were over the last year), has rocketed up to record bullish extremes.

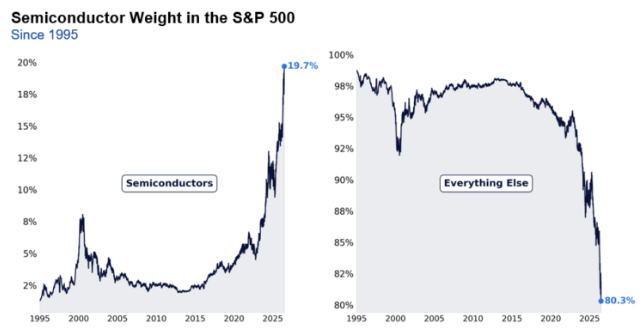

The defining story of the first half of 2026 was not a macro shock, it was the continued structural transformation of equity markets

Market concentration remains near historic highs. Passive investing continues to absorb capital at unprecedented rates. Retail investors have become a persistent source of demand. Leverage has migrated toward increasingly short-dated and concentrated exposures. Together, these forces are reshaping liquidity, price discovery, and the behavior of volatility.

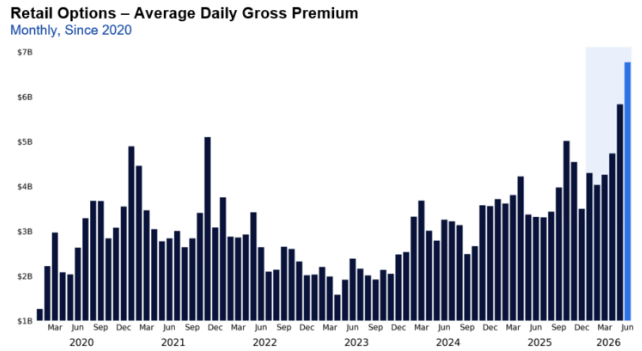

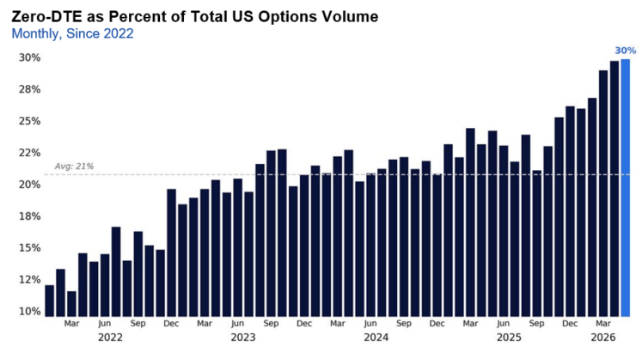

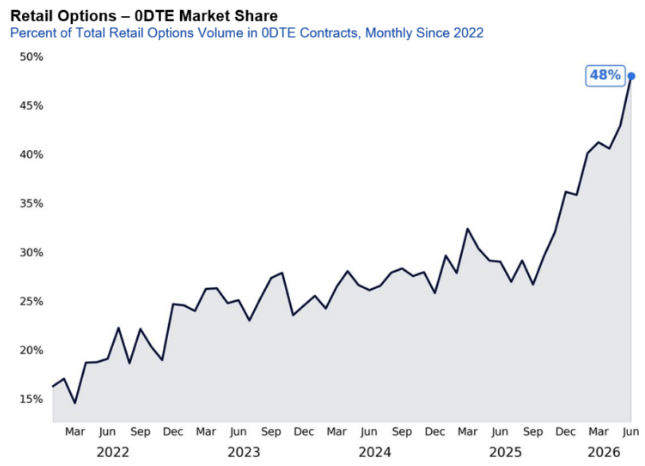

Retail investors have poured into stock options in 2026:

Unlike previous periods of elevated retail activity, today’s retail investor is increasingly concentrated in the same sectors driving benchmark performance, led by semiconductors and broad-based ETFs.

In June alone, retail traded approximately $1.9 billion of semiconductor options premium per day (6x the historical average) with about 75% of that activity concentrated in call options.

One out of every three listed options traded in the US now expires the same day, roughly doubling zero day options’ market share since daily expirations launched in 2022.

Following the introduction of Monday and Wednesday expirations in single stocks at the beginning of this year, nearly half of all retail options volume executed by Citadel Securities now trades in zero day contracts, up from 30% in 2025 and just 13% in 2021. Average time to expiry on Citade’s platform is less than 3 days.

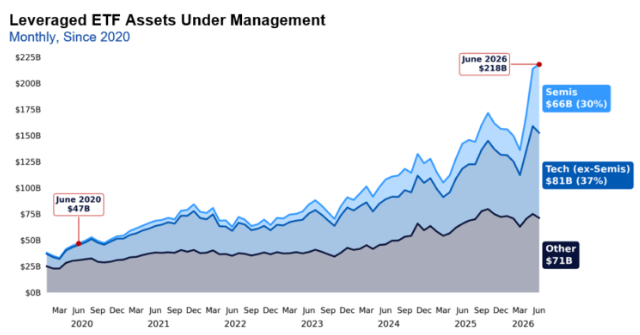

Investors chase what’s hot (semis and tech) with leveraged ETFs:

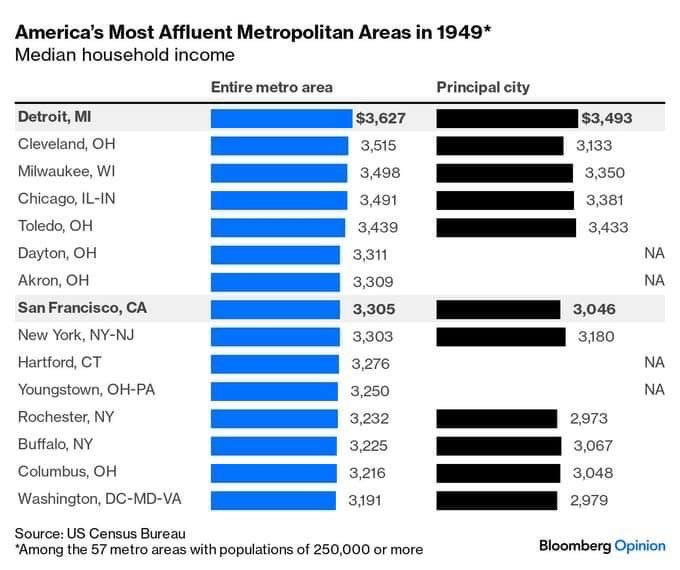

In 1949, four of America’s seven richest metro areas were in Ohio. Cleveland, Toledo, Dayton and Akron were out-earning New York, San Francisco and DC.

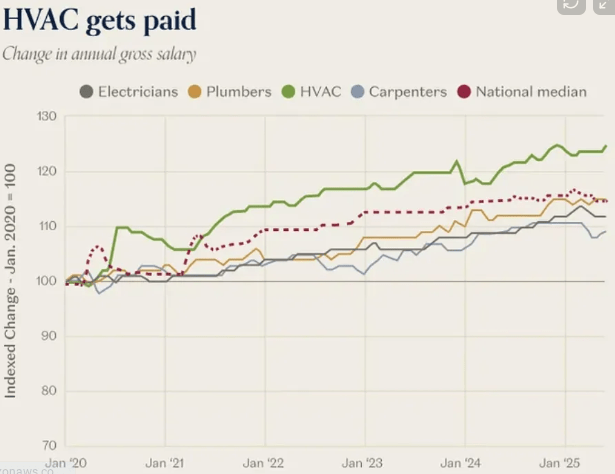

Weird things happen to economies when you have huge bursts of productivity that are concentrated in one industry. Obviously, it’s great for that industry, because when the cost of something falls while its quality rises, we usually find a way to consume way more of that thing – creating a huge number of new jobs and new opportunities in this newly productive area.

But there’s an interesting spillover effect. The more jobs and opportunities created by the productivity boom, the more wages increase in other industries, who at the end of the day all have to compete in the same labor market.

Our explosion of demand for data centers means there’s infinite work for HVAC technicians. So they get paid more (even though they themselves didn’t change), which means they charge more on all jobs (even the ones that have nothing to do with AI). Furthermore, the next generation of plumber apprentices might decide to do HVAC instead; so now plumbing is more expensive too. And so on.

Academics have published new research on the impact that Short Form Videos (SFV) like TikTok, Instagram Reels and Youtube shorts have on cognitive and mental health. The report systematically reviews and analyzes 71 studies involving over 98,000 participants.

SFV use is linked to poorer cognitive performance, with the strongest deficits in attention and inhibitory control, suggesting users struggle to focus and suppress impulses.

Frequent exposure to fast-paced, highly rewarding SFV content may rewire attention systems, fostering “rapid disengagement” from tasks that are slower or require sustained effort, reducing cognitive endurance over time.

SFV use is associated with poorer overall mental health, with the strongest links to stress and anxiety, indicating consistent emotional strain among heavier users.

Heavy SFV use reinforces impulsive engagement loops driven by dopamine rewards, contributing to compulsive scrolling and difficulty disengaging, patterns resembling behavioral addiction.

Short-form video consumption is associated with poorer sleep quality, especially when used at night, due to overstimulation and blue light disrupting melatonin, which can worsen mood and cognitive functioning.

Higher SFV use correlates with increased loneliness and reduced life satisfaction, as digital interactions replace real-world social connection for some users.

Negative effects occur across both youth and adults, meaning the cognitive and emotional risks of SFV use are not limited to developing brains; adults experience similar declines and mental health associations.

_______________________________

These days, it’s all stocks all the time, with reputable authorities calling on small investors to put everything they have saved into equities. Older investors are reminded of the mantra so common in 1999: “Every penny you don’t have invested in stocks will hurt you.”

More than a generation ago, financial historian Peter Bernstein wrote about investors’ “memory banks,” the market experience that accumulates in their hippocampi over their investing lives and molds their investment strategy. As he put it, looking back on the 1990s: “Most of the new participants in the market had no memory of what a bear market was like.”

And here we are today, almost seventeen years into a great bull market. Rather like 1999, also seventeen years into a long-term bull market, or 1966, once more seventeen years. Or 1873, sixteen years in, or 1837, eighteen years in, or 1893, twenty years in — to name a few of the notable tops over the past two centuries. Just long enough to produce empty memory banks in just enough investors.

Historically, valuations have been a useful (though not perfect) indicator of real returns over the following decade. Below, you’ll see historical CAPE readings (in black) for the U.S. market alongside their corresponding forward ten-year real returns (in green). The conclusion is straightforward: when valuations are low, future returns tend to be above average; when valuations are high, forward returns tend to be much more muted.

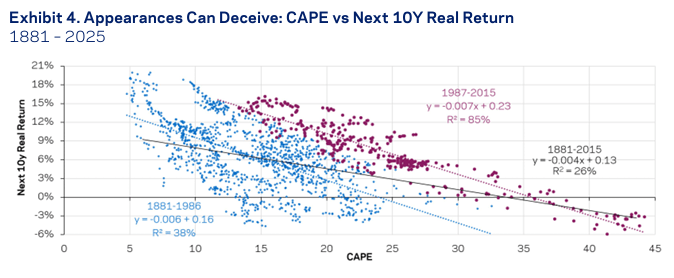

Right now, the U.S. market sits at a CAPE ratio of around 40. It’s nearly double the long-term average of roughly 20, and the second most expensive in history.

historically, when valuations have climbed to this level, the following decade hasn’t been kind to investors. Not once has a country that ended a year with a CAPE above 40 produced positive real returns over the next ten years. That’s not a personal opinion but what the data shows.

To get a sense of what current valuations might mean going forward, I ran a linear regression using historical CAPE data and forward ten-year real returns. The relationship is remarkably consistent: as valuations rise, future returns fall. At today’s valuation levels, the regression suggests an expected real return of -2.46% for the next decade. From a historical perspective, the last time we were at the CAPE reading we find ourselves in today, the market went on to lose -2.11% per year for the next ten years.

Valuation isn’t the only red flag flashing. Today, about 40% of the market is concentrated in its 10 largest companies. This is the most concentrated the market has ever been.

Concentration itself isn’t a bearish sign. What really matters is how concentration changes going forward. Rising concentration tends to coincide with strong market performance as leading firms continue to gain share and deliver growth. On the other hand, when concentration starts to fall, this means your largest players are underperfoming the rest of your portfolio, and that’s when returns have historically suffered. If the biggest names continue to pull away from the pack, the market could remain strong for a while. But if that leadership falters, history suggests the unwind can be painful.

Imagine you are a new college grad from a middle-class family. If you are lucky, you have no education debt, but many do. If you are lucky, you land a 100k+ job, but many don’t. Even if you are lucky, you still look up at astronomical asset prices (houses) and try to work out how you can maybe afford one in 20 years, with the understanding that they will only continue to go up in the meantime.

You are surrounded by online examples of success (usually fake or survivorship bias). Your attention span has been fried by TikTok and YouTube shorts. You simply don’t have the patience or discipline for the slow path.

So instead, you start taking outsized risks with your monthly paychecks – crypto, options, meme stocks, meme coins, sports betting. Your rationale is that this current amount could never buy a house, but if you win it might. And if you lose, you simply have to wait a week or two before you can reload and try again. This is “hyper-gambling.”

The obvious downside of taking repeated high-risk investments is that most will fail in this lottery strategy, and if you find yourself at the end of the tunnel with no diamonds to show for it, you will be even farther behind.

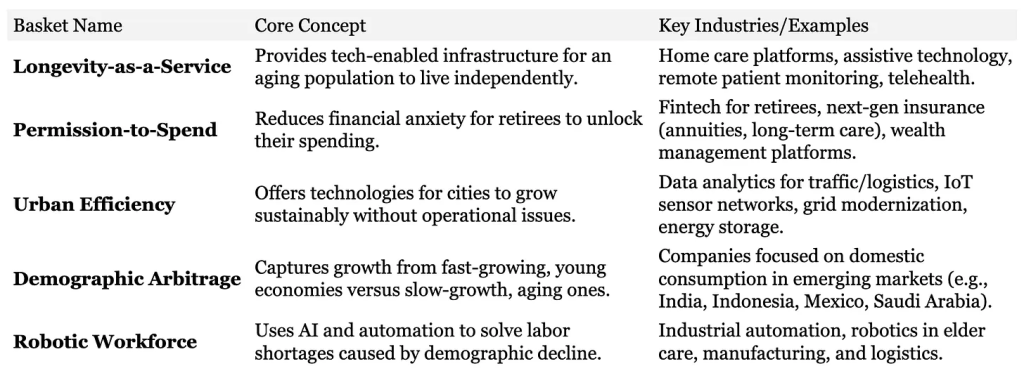

Between 2015 and 2050, the proportion of the global population over 60 is set to nearly double, climbing from 12% to 22%. The most extreme changes though, are happening at the upper end of the age spectrum. The number of individuals aged 80 or older is projected to triple between 2020 and 2050, reaching 426 million. This is exponential acceleration, and two-thirds of the world’s elderly will live in developing nations, up from just over half today.

Running parallel to the aging of the globe is a second, equally powerful human migration: the mass movement into cities. Today, 58% of the world’s 8 billion people live in urban areas. By 2050 this figure is projected to climb to 70%. Nearly 90% of this 2.5 billion-person increase in cities will occur in Asia and Africa. India, China, and Nigeria. are projected to account for over a third of all new urban dwellers globally.

President Clinton noted in his January 2000 State of the Union speech:

“We begin the new century with over 20 million new jobs; the fastest economic growth in more than 30 years; the lowest unemployment rates in 30 years; the lowest poverty rates in 20 years; the lowest African-American and Hispanic unemployment rates on record; the first back-to-back surpluses in 42 years; and next month, America will achieve the longest period of economic growth in our entire history.”

That wasn’t an exaggeration. But it marked the beginning of the worst decade for the U.S. stock market in modern times.

In January 2010, President Obama noted in his State of the Union speech:

“One in 10 Americans still cannot find work. Many businesses have shuttered. Home values have declined. Small towns and rural communities have been hit especially hard. And for those who’d already known poverty, life has become that much harder.”

That wasn’t an exaggeration. But it marked the beginning of one of the best 15 years (and counting) for the U.S. stock market in history.

In the last two decades, the share of American adults who say they exercise or play sports on any given day has increased by about 20 percent.

The share of Americans who say they don’t regularly work out or play sports, which SFIA calls the “inactivity rate,” has fallen by more than one-fifth since 2019.

Rich and young Americans exercise the most. Poor and older Americans work out the least. Among adults, income predicts activity better than age.

The increase in exercise minutes is significantly led by young people and women over 65, who increased their weekly workouts by about twice as much as men over 65.

No fitness activity saw a larger increase in participation between 2019 and 2024 than Pilates. Yoga and barre were close behind among the fastest-growing activities. Meanwhile, group cycling, cardio kickboxing, boot camps, and cross-training workouts like CrossFit got walloped by the pandemic, and they haven’t bounced back. In general, Americans seem to have traded sweaty group classes for gentler core work.

After persevering through a valley of tears since 2010, value investors are finally beginning to reap a fruitful harvest in developed international markets. Over the past five years, the value premium has returned to positive territory in international markets as value stocks have returned to outpacing growth stocks. Since July 2020, value has outperformed growth by 11.6% annualized in developed international markets:

Mastroianni: It seems like the takeaway from this research that has been done over the past 10 years or so is that people are way too negative about their own social abilities and the things that are likely to happen when they talk, especially to someone new. So, for instance, they underestimate how pleasant it’s going to be to talk to someone new. But even afterward, when we ask them, hey, how much did you like that person? They say oh, I like them a lot. And when we ask, how much did they like you? Oh, less than that. I ran one study with some friends of mine where we had people talking groups of three and we’re like, okay, how much did you like them? People would say 5 or 6 out of 7. And how much did they like you? People would say 4 or 5 out of 7. On average, people thought they were the least liked person in the conversation, which obviously can’t be true for each person.

Thompson: We are, on the one hand, the social animal. Yet we delude ourselves about the degree to which we’re a fun hang. We’re the social species and we’re the socially anxious species as well.

Mastroianni: Yeah, well, we’re the ones who care about it the most. And so we have the most to lose. And so we worry about it the most in part in the hopes that maybe it makes us better at doing it. The way I think about it is in our evolutionary history, we lived in groups. But how often did we meet someone who we literally had no connection to before? I can’t imagine it was all that often. But today it can happen literally every day. You get on the bus and it’s full of people that aren’t related to you. You don’t know them. They don’t know you. That’s a really weird thing to do.

____________________________________

Morgan Stanley surveyed all stocks trading on U.S. exchanges over a 40-year period, between 1985 and 2024. They found the median stock experienced a decline of 85% at one point or another. Worse yet, more than half of these stocks never fully recouped their losses. The median stock recovered to just 90% of its prior high-water mark. Among those stocks that were able to reclaim their prior highs, it was a long process—about five years, on average.

Those numbers only apply to the median stock, but suppose you had above-average stock-picking skills. How would things have turned out? If you had the foresight to pick the 20 best performing stocks over that 40-year period, at some point they still would have delivered an average agonizing draw-down of 72%.

It’s hard to remember, but Apple dropped 83% at one point. Nike once lost 66%. Even Nvidia, which was the best performing stock over the past 20 years through 2024, lost more than 90% at one point. And most notably, Amazon was once down 95% from its prior high.

Over the long term, share prices tend to move in tandem with corporate profits. When a company’s earnings increase, often its share price does too. The problem is that prices are only sometimes rational. Very often, stock prices disconnect from corporate earnings, and the gap can be significant.

This was first proven empirically Daniel Kahneman and Amos Tversky. In 1974, they published a paper that found investors exhibit an “availability heuristic.” That is, they tend to rely on the information that is most available. That’s a problem because the information that happens to be most available isn’t necessarily the information that’s the most accurate or even relevant. Often, the information that happens to come to mind is the information that’s most vivid. In other words, extreme information or news becomes most memorable, and thus drives decision-making.

___________________________

ChatGPT users may want to think twice before turning to their AI app for therapy or other kinds of emotional support. Sam Altman, OpenAI’s CEO:

“People talk about the most personal sh** in their lives to ChatGPT. People use it — young people, especially, use it — as a therapist, a life coach; having these relationship problems and [asking] ‘what should I do?’ And right now, if you talk to a therapist or a lawyer or a doctor about those problems, there’s legal privilege for it. There’s doctor-patient confidentiality, there’s legal confidentiality, whatever. And we haven’t figured that out yet for when you talk to ChatGPT. This could create a privacy concern for users in the case of a lawsuit, because OpenAI would be legally required to produce those conversations today.“

The 1990s were a turning point for country’s mainstream acceptance, driven by two mutually reinforcing phenomena:

Improved Telecommunication Infrastructure: The Telecommunications Act of 1996 enabled American media companies to consolidate regional stations into national networks, facilitating country radio play outside of rural strongholds. Simultaneously, enhanced geographic radio coverage brought consistent access to under-served rural listeners. Together, these infrastructure improvements fostered a virtuous cycle: greater airplay propelled more country songs onto the charts, which in turn drove even more airplay.

Country Crossover Successes: Country crossovers like Garth Brooks, Shania Twain, and Tim McGraw blended conventional genre staples with accessible pop and rock influences, broadening the format’s appeal beyond its traditional fanbase.

______________________________________

Something unusual—and incredibly fast—is happening with teenagers running the 100-meter around the world. From Japan to the U.K., young speedsters are posting eye-popping times in track’s most prestigious event. What’s driving these turbocharged athletes who aren’t old enough to vote?

Peter Bernstein liked to say that investors have memory banks: the market returns collectively earned by people of similar age. Experience shapes expectations. The problem is that your memory bank can deceive you in dangerous ways. Your experience of the past is a reasonable guide to the future only if the future turns out to resemble the portion of the past that you’ve lived through. And it often doesn’t. It’s worth looking at a few investing beliefs that your memory bank might hold—and asking whether they’re still valid.

_______________________________

How much longer will emerging markets be undervalued and hated?

________________________________

Nasdaq Price to Earnings valuations are at the very high end of their historical range. That means they are extremely expensive.

While countries like the United States and India are extremely expensive relative to the rest of the world, the global stock market as a whole has seen its P/E ratio rise dramatically from the early 2010s.

_______________________________

Looking at Enterprise Value (EV) divided by sales, we’re not above the 2000 and 2021 bubble peak for global stocks:

The Federal Reserve did a study that looked into the financial habits of Canadians whose neighbors won the lottery. The neighbors of people who struck it rich were more likely to increase their spending, take on more debt, put more money into speculative investments, and eventually file for bankruptcy. And the larger the winnings, the more likely that others in that neighborhood would go bankrupt.

It’s in our flawed nature to compare ourselves to others, particularly people we see and interact with every day. Money insecurity leads us to compete and not appreciate what we have. Also true, though, is that the research shows one thing for certain: The Joneses aren’t very happy.

An examination of 259 different independent samples found that materialism was “associated with significantly lower well-being” and was a poor way of meeting psychological needs. The researchers’ findings suggest that this association holds across different demographics, participants, and cultural factors. Another meta-analysis of 92 studies found that those pursuing goals of growth, community, giving, and health experienced significantly higher levels of well-being than those pursuing the Jones-y goals of wealth, fame, or beauty.

You’ll never be content trying to keep up with the Joneses because there is an endless supply of them to keep up with. There are always people spending more money, taking nicer trips, buying bigger houses and making more money than you are.

There was another classic psychological study that compared lottery winners with people who were paralyzed in an accident. Surprisingly, the lottery winners weren’t significantly happier than the average person and actually reported less enjoyment from everyday experiences. The big win seemed to raise their expectations, which made small daily pleasures feel less satisfying.

In contrast, many accident victims rated themselves as moderately happy, despite their life-altering injuries. While thinking about their past lives sometimes made them feel worse, they still found deep meaning and enjoyment in ordinary things because they appreciated them more. After major life changes, people adjust their expectations. Lottery winners adjusted upward and felt less satisfied. Accident victims adjusted downward and found more value in the little things.

Nothing was the same after June 28, 1914. The assassination of Archduke Franz Ferdinand triggered a chain of events that led to WWI and closed the NYSE for months. One month to the day of the assassination, Austria-Hungary declared war. Three days later, Henry Noble, president of the NYSE, closed the exchange. Other regional U.S. exchanges in Chicago, Baltimore, San Francisco, Philadelphia, and other cities followed suit. Most major exchanges around the world closed too.

Noble knew that wars demanded funds. Foreign investors could make a run on the exchange, selling securities to raise cash. The cash could then be converted into gold and shipped back to Europe. That put the U.S., being on the gold standard, in a tricky spot. Depleting the U.S. gold reserves would put faith in the dollar and adherence to the gold standard at risk.

June 28, 1914 – Archduke Ferdinand assassinated. Dow closes the next day at 57.9.

July 28, 1914 – Austria-Hungary declares war on Serbia – World War 1 begins: Dow closed 55.3.

July 30, 1914 – Dow closes 51.7.

July 31, 1914 – NYSE & regional U.S. exchanges close the markets

December 12, 1914 – NYSE reopens stock market with trading limitations.

December 14, 1914 – Dow closes 56.8.

December 14, 1915 – Dow closes 98.3.

When the stock market reopened December 12, 1914, investors had four and a half months to reassess the business environment in war time. And business was good. Over the next 12 months, the Dow soared 73% (Dec. 14, 1914, to Dec. 14, 1915, not including dividends). The U.S. became the main food and war supplier for the Allies war effort. Companies like U.S. Steel and DuPont saw profits explode 5x and 10x respectively, in a year. Dividend payments did the same. WWI is the perfect example of why geopolitical events are hard to predict. The market reacts in unexpected ways during scary confusing times.

______________________________

Reciprocity is a deeply human thing, and it applies directly to the nature of interest. If you show someone that you’re interested in them, they will reciprocate that curiosity by revealing what makes them so interesting. Believing that someone is boring is a failure of recognizing jthat fact. Boredom is almost always the result of a lack of curiosity, or the inability to see anything or anyone through the lens of a question. In a way, boredom is arrogance. It’s the acceptance of the belief that nothing is worth your interest because you already know what you need to about yourself, others, and the world. A curious mind is a humble one, as a prerequisite for curiosity is the acceptance that there is more to life than what you think you already know.

____________________________

We are a story-driven species. From cave walls to balance sheets, we look for narratives that explain the world and our place in it. And nowhere is this tendency more dangerous than when we only learn from the winners. When we allow survival alone to imply superiority. When the fact that someone or something made it through becomes enough proof that they knew what they were doing.

This is the essence of survivorship bias, and in the world of investing, it distorts almost everything. Consider the stock market, which is full of visible winners. We often hear stories of stocks that went 20x, fund managers who outperformed for a decade, companies that pivoted into success, and investors who became celebrities.

What about the others? The ones who didn’t make it? They’re barely mentioned, rarely studied, and almost never remembered. And so, the narrative we inherit is hopelessly incomplete.

Then there’s the most seductive arena of all: success stories. Business books, biographies, and podcast interviews are all proudly built on the same question: “How did you do it?”But that question, when asked only of survivors, creates a dangerous narrative. It turns randomness into wisdom and luck into method.

A founder who succeeded against all odds is praised for her vision, her grit, and her intuition. But what about the 100 others who had the same qualities and failed? What about the timing, the macro conditions, the investor interest, the random tailwinds that no one could have planned? None of that gets included in the final story. And so we start to think: this is how success works. This is the roadmap. Just do what she did.

Minimum Levels Of Stress, a phenomenal new article by one of my favorite authors; Morgan Housel.

A day after the September 11th terrorist attacks, every member of Congress stood on the steps of the U.S. Capitol and sang God Bless America. Could you imagine that happening today? It’s easy to say no, given how nasty politics has become. But if America faced an existential crisis like 9/11 again, I think you’d see the same kind of unity return. There’s a long history of enemies putting their differences aside when facing a big, devastating threat. People get serious when shit gets real. If that sounds like wishful thinking to you, let me propose a reason why: Part of the reason today’s world is so petty and angry is because life is currently pretty good for a lot of people.

There are no domestic wars. Unemployment is low. Household wealth is at an all-time high. Innovation is astounding.

As the world improves, our threshold for complaining drops. In the absence of big problems, people shift their worries to smaller ones. In the absence of small problems, they focus on petty or even imaginary ones. Most people – and definitely society as a whole – seem to have a minimum level of stress. They will never be fully at ease because after solving every problem the gaze of their anxiety shifts to the next problem, no matter how trivial it is relative to previous ones. Free from stressing about where their next meal will come from, worry shifts to, say, a politician being rude. Relieved of the trauma of war, stress shifts to whether someone’s language is offensive, or whether the stock market is overvalued.

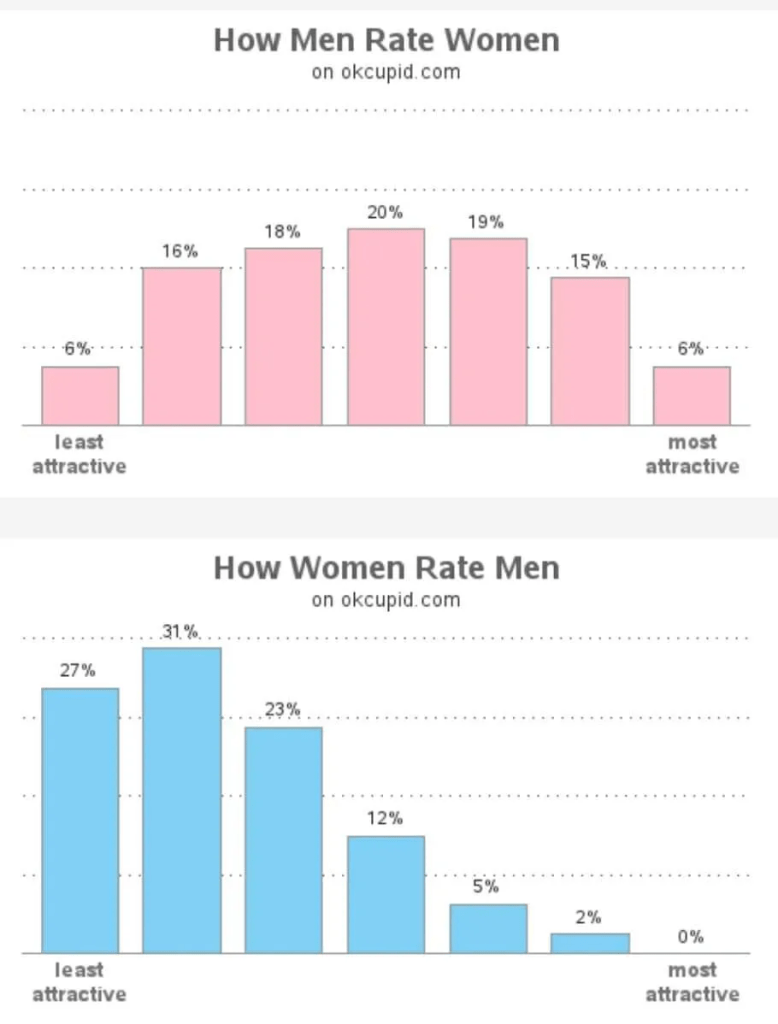

A summary and thoughts on the data from the author:

The typical woman is disgusted by the typical man

The typical woman is moderately disgusted by the median man

The typical woman is strongly disgusted by the bottom quarter of men

Men should stop taking rejection so personally. When the typical women rejects you, the problem isn’t so much that she finds you unappealing. The problem is that the typical woman finds almost all men unappealing.

Men should try harder to be less disgusting.

Women should try harder to be less disgusted. Most women eventually accept a guy who isn’t visibly attractive. Much of the reason is that superficially unappealing guys win them over with charm, humor, and devotion.

It’s not hard to use evolutionary psychology to explain why the typical man disgusts the typical woman: Since women’s maximum reproductive capacity is strictly limited, they’re evolved to be hypergamous, with a strong preference for mating with the best of the best.

__________________________________

Numerous studies show a strong relationship between stock market valuation and long-term subsequent returns. Since 1979, global stock market indices have been valued on average at a Shiller-CAPE of 20 and a price-to-book ratio (PB) of 1.9. Investors who invested at attractive valuations in recent decades were able to achieve above-average returns over the following 10-15 years. Those who bought at high valuations, on the other hand, were generally disappointed in the long term.

Here’s a look at where countries stand today. The lower left are the least expensive countries/stock markets and the upper right are the most expensive. You can see that India is off the charts expensive while the United States is in another solar system based on how overvalued it is.

What long-term stock market returns can investors expect in the 20 most important stock markets based on valuation?

Based on CAPE and PB, Latin America and Asia currently show the lowest valuations, particularly in Brazil, Korea and China. These equity markets are currently trading at a CAPE of 9-12 and a PB of 0.9-1.4.

Historically, comparably attractive valuations have been followed by above-average returns of 9-11% (in real terms) over the next 10-15 years.

In general, the emerging markets (with the exception of India) are currently valued much more attractively than the developed markets. Historically, comparable valuations in the emerging markets have been followed by annual returns of 7.7%, while the developed markets are expected to achieve rather low returns of 2.5%.

The low return expectations of the developed equity markets are caused by the extremely high US valuation: with a CAPE of 35.4 and a P/B ratio of 5.1, the US market is trading at around twice the level of recent decades. In the last 140 years, such high valuations have been followed by long-term returns of only 0.1% p.a.

Among the developed markets, Germany, Italy, Japan, Singapore, Spain, Norway and the UK still appear attractive. Investors here can expect annual returns of 7-8% in the long term here.

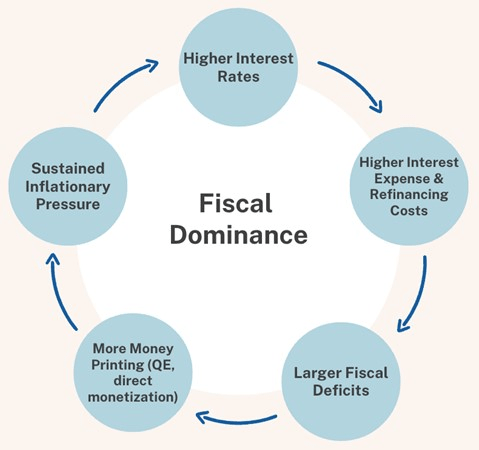

Why government spending is now more important than bank/private sector lending

Why central bank tools become ineffective at combating inflation in this new environment

Why DOGE will fail to reach its goals on cutting government spending

Why the stock market, not labor markets, have become the dominant driver of tax revenues

What to own/invest in to navigate the through the years ahead

___________________________

A phenomenal Q&A with Russell Napier, market strategist and historian, discussing how the global economy and financial markets will look in the months and years ahead.

___________________________

Forget about making a New Year’s resolution. Have you tried imagining your deathbed? It’s called a Premortem. It’s a habit that began for Ron as a response to the death of his parents in the 1990s. His mother was at peace with herself when she died, he says. But his father was “racked with regret and remorse” about decisions he made and the opportunities he missed. What he took away from their experiences was the last lesson that his parents would teach him—and the most profound of them all. Don’t wait until the end to decide if you are proud of your life. Do it before it’s too late. Do it while you can still do something about it. To him, there is nothing macabre or even remotely depressing about ruminating on death. In fact, he finds it to be oddly inspiring.

______________________________

There’s one particular, very achievable commitment in mind that will help you become happier and improve your health and effectiveness: This year, start getting up early.

Our brain exhibits greater functional connectivity in the mornings. This, we might assume, facilitates better performance of complex tasks.

It tends to enable the achievement of other popular goals. The goal-directed brain regions—such as the hippocampus and orbitofrontal cortex—work better at this time than later in the day.

One habit that is easier to adopt first thing in the morning is exercise. Clear data exist to show that when people intend to exercise early in the day, they are significantly less likely to experience “intention failure” than if they plan to exercise later.

People who get up early enjoy a more positive mood throughout the day compared with those who rise late.

______________________________

All the major Wall Street brokerage and bank strategists failed to anticipate how well the market would do in 2024. Only part of the problem is that they are bad at predictions; the bigger issue is that they do it all. It’s kinda like Phrenology, the pseudoscience feeling bumps on people’s skull to predict their personality traits. It’s not that there are better or worse phrenologists, but rather, why was anyone doing phrenology? Think about how variable the future is. Random events can and will completely derail the best laid plans we may make. Even the most well-ordered, thoughtful forecasts turn to mush when randomness strikes. And randomness is served up daily.

____________________________________

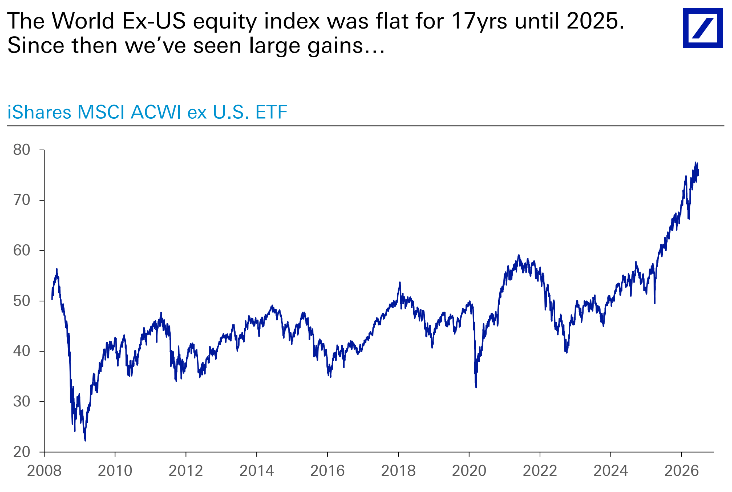

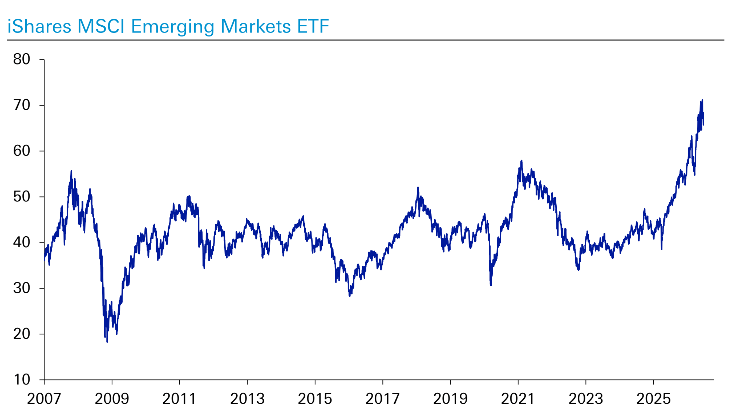

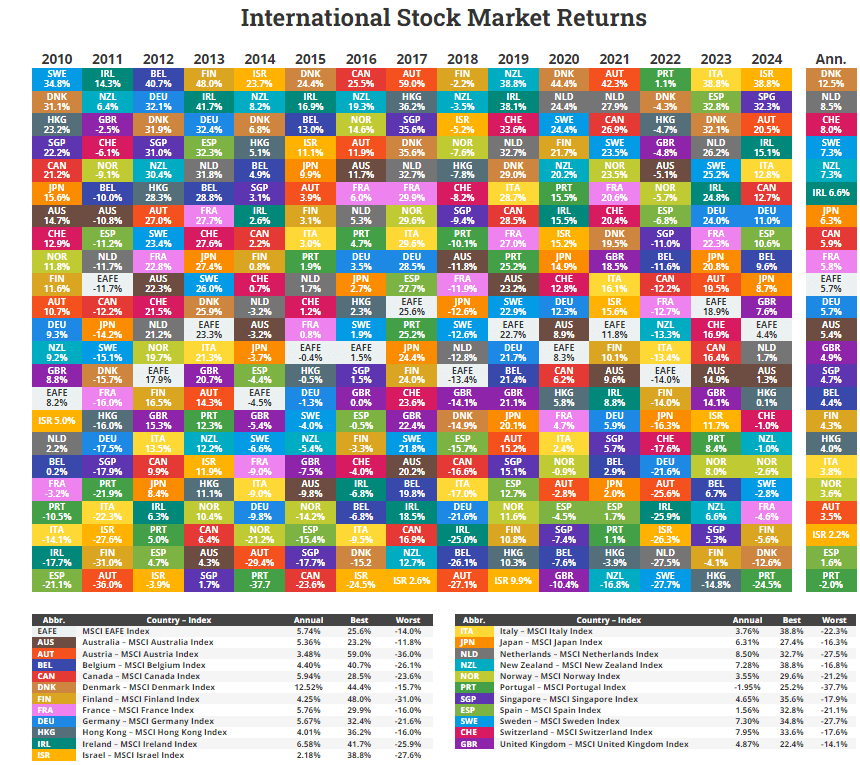

It’s a big world out there. The U.S. makes up a little less than half of the global market cap. By avoiding international stock markets, you cut out half of the investment opportunities. Why limit yourself?