Your hippocampus doesn’t encode days that feel identical. If this Tuesday looks like last Tuesday, your brain files them as a single compressed memory. The second day never gets its own folder.

This is why decades feel like they disappeared. The hippocampus uses novelty as its filter for “worth storing.” Repetitive routines trigger temporal compression. Same commute, same desk, same dinner, same bedtime: the brain deduplicates the whole sequence into one entry. You lived 365 days. You filed 40.

As people move through continuous experience, the hippocampus and medial prefrontal cortex fire in discrete bursts at moments the brain flags as “something changed.” Each burst becomes a retrievable memory later. In stretches with no boundaries, the bursts flatten. Participants with more boundaries in a given period remembered more of it afterward. Segmentation literally builds memory.

Sleep is the second mechanism. During slow-wave sleep, the hippocampus replays the day’s episodes and transfers them to the neocortex for long-term storage. This is when memory actually gets filed. Cut sleep short and encoding efficiency drops. Chronic sleep debt means experiences you had never complete the transfer. The memory existed. It just never made it to disk.

The third mechanism is where dopamine meets attention. Novel stimuli trigger the ventral tegmental area to release dopamine into the hippocampus, which gates what gets encoded. Mind-wandering does the opposite. When your default mode network takes over (phone scrolling, rumination, email during dinner), the hippocampus stops tagging the present. You were at the wedding. Your hippocampus was in your inbox.

The fix comes straight out of the mechanism. New locations, new food, new people, new routes home. The brain needs boundaries to build memories. Go to bed earlier so replay actually runs. Put the phone down when something is happening so the dopamine signal can fire.

The more forgettable the day, the shorter the decade.

__________________________

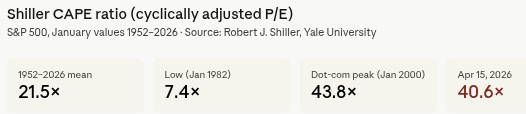

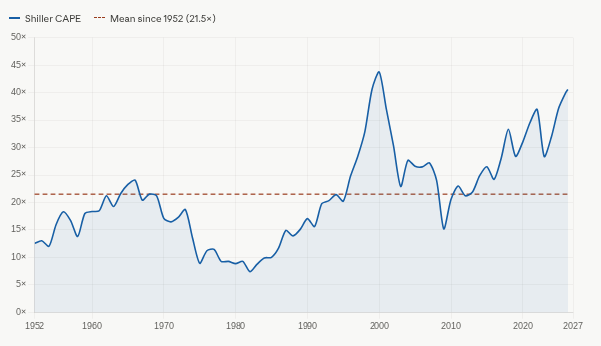

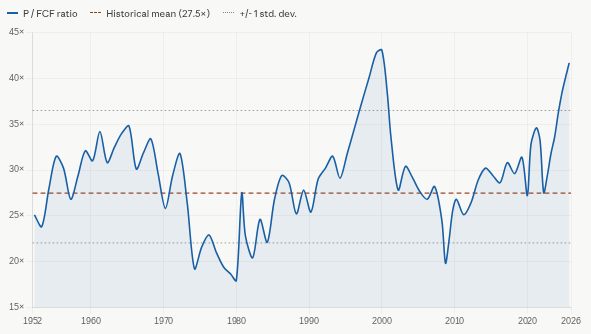

Traditional valuation metrics like the Shiller CAPE (price-to-earnings) ratio have been screaming “overvalued” for most of this century, but there has been almost no mean reversion since 2008 for U.S. stocks:

Why?

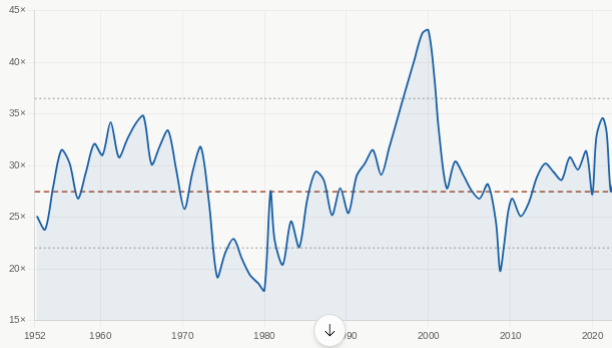

When you swap earnings for free cash flow (sales minus input costs, labor, taxes, and capex — basically what’s actually available to pay owners), the picture changes dramatically. Until recently, the price-to-free-cash-flow ratio bounced around but had no long-term upward drift:

Two structural shifts explain the divergence:

- Labor share has declined ~8 percentage points of GDP since 1980. Less of the pie goes to workers, more goes to firm owners. This boosted earnings.

- Capex has been relatively weak as a share of firm value. Firms (especially big tech) generated massive earnings without heavy reinvestment, so cash flow grew even faster than earnings.

However, that clean free-cash-flow story is under pressure right now. Some of these companies have gone from huge positive FCF to zero or negative FCF, taking on debt to fund it. Big tech has flipped from cash-generating machines to massive spenders on AI data centers, chips, and energy infrastructure.

The chart below is the same as above, but extends the data adding the last few years:

Bullish case: This is 1-2 years of heavy investment that will produce a new plateau of even higher cash flows, and AI further reduces labor share.

Bearish case: AI isn’t “free money” — even adopter firms (not just the hyperscalers) will need serious capex to implement it, and the payoff is uncertain.

Full podcast discussion on this topic on an episode of Odd Lots this week.

__________________________

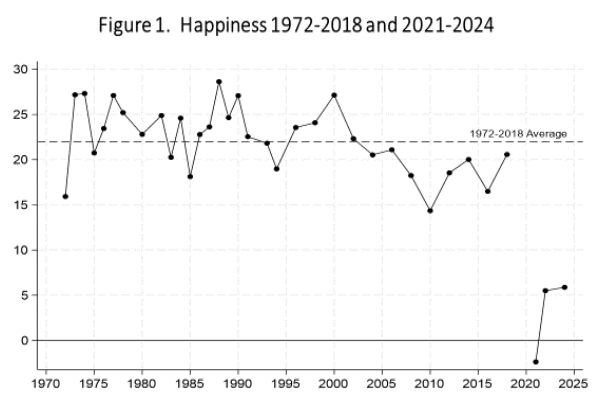

There was a sudden, sharp and historically unprecedented decline in self-reported happiness in the US population. It occurred during 2020, the year of the Covid pandemic, and mainly persists through 2024.

This happiness crash spread across nearly all typical demographics and geographies. The happiest groups pre-Covid (e.g., whites, high income, well-educated and politically/ideologically right-leaning) tend to show the largest happiness reductions.

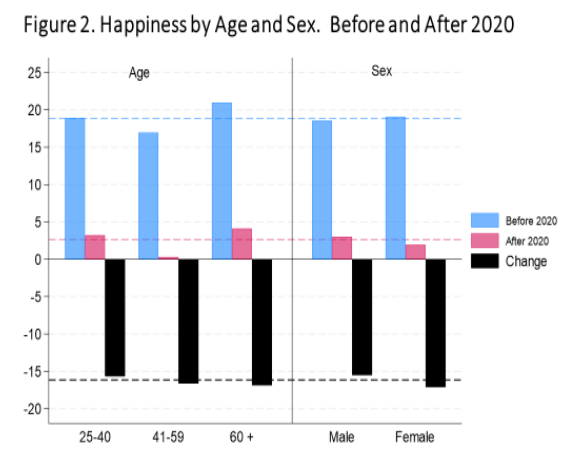

The glaring exception is marital status, which has consistently been an important marker for happiness. The already wide happiness premium for marriage has, if anything, become slightly wider. With both married and unmarried reporting large declines in happiness the country has become segregated: slightly over half-the married adults-remain happy on balance; the unmarried, nearly half, are now distinctly unhappy.