Private equity (PE) firms have been buying up about 10% of US life insurance companies since 2020. They’re then using the insurance companies’ money (called the “float” – money from premiums that hasn’t been paid out yet) to make risky loans to struggling businesses.

They’re using a private ratings agency to label these risky loans as safer than they actually are. This fake safety rating lets them:

Hold less cash in reserve (normally you need more reserves for risky investments)

Legally invest in things they otherwise couldn’t

Many of these loans are going bad – about 10% are already defaulting. The companies that borrowed the money are often unprofitable startups (especially software companies) that can’t actually pay back their debts. Some are even “zombie companies” kept alive artificially.

How the Fed raising rates in 2023 amplified this problem:

Fed Raises Rates → Government Borrowing Costs Go Up

When the Fed raised interest rates, it became more expensive for the US government to borrow money

The government pays interest on its debt, so higher rates mean higher interest payments

This caused the government’s budget deficit to balloon by 3% of GDP in 2023

Bigger Deficit → More Treasury Bonds Issued

To cover this bigger deficit, the government had to issue more Treasury bonds

These bonds became “fresh collateral” – basically, new assets that could be used as backing for loans

The RRP Money Gets Unlocked

There was $2.5 trillion sitting in something called the Fed’s “Reverse Repo Program” (RRP) – think of it as a parking lot for cash

Normally this money just sits there safely

But with all these new Treasury bonds available, financial institutions could use them to borrow against in “repo markets” (short-term lending markets)

PE Firms Borrow This Money

The private equity firms and their various entities (the “layers of the leverage cake”) were able to tap into this massive pool of money

They used it to fund more and more risky loans through the insurance companies

Instead of letting the economy cool down (which is what rate hikes are supposed to do), the Fed accidentally created a situation where trillions of dollars flowed into this problematic private equity scheme.

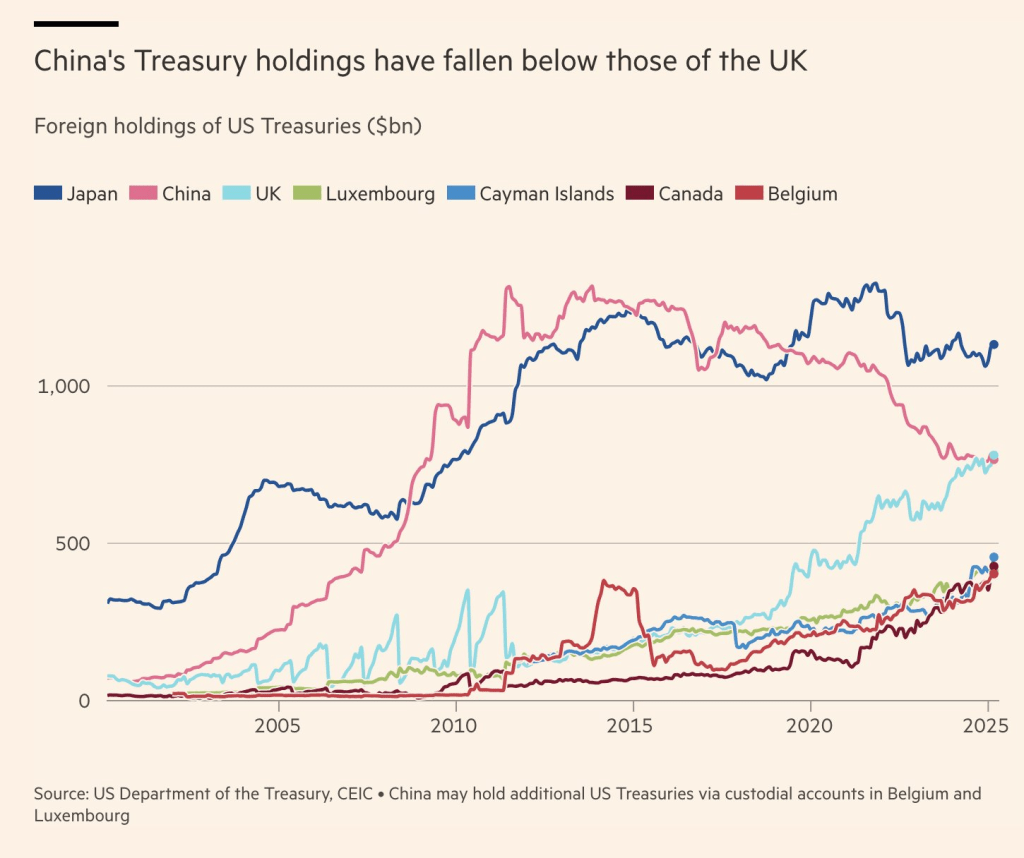

Who Gets Hurt: Foreign banks and insurance companies:

Foreign Institutions Bought the Debt

These PE firms and BDCs (Business Development Companies – investment funds that make these risky loans) didn’t just use insurance company money

They also borrowed money from banks and sold bonds/securities to investors

Foreign banks and insurance companies in countries like Japan and Germany were major buyers of these securities

Why Foreign Buyers?

Japanese and German institutions are from “surplus creditor nations” – countries that save a lot and invest globally

They’re always looking for places to invest their money

US securities seemed attractive, especially ones with good (fake) credit ratings

They’re Holding the Bad Loans

When these loans start defaulting (which the author says is already happening at 10%+), the value of those securities plummets

The foreign banks and insurers who bought them will take massive losses

They Don’t Know Yet

Stocks of these foreign financial institutions are “at all time highs”

Meanwhile, US-listed PE firms and BDCs have already collapsed in value

This suggests the foreign institutions haven’t realized their investments are worthless yet – the losses are hidden in complex financial structures

Foreign banks and insurers thought they were buying safe, well-rated US investments. Instead, they’re holding bags of loans to failing startups and zombie companies. When they finally discover this (mark their books to reality), their stock prices will crash too. It’s like they bought what they thought were AAA-rated bonds, but they’re actually subprime loans in disguise.

In Summary: This is as a massive, ticking time bomb of bad debt hidden inside insurance companies, enabled by sketchy ratings and Fed policy.

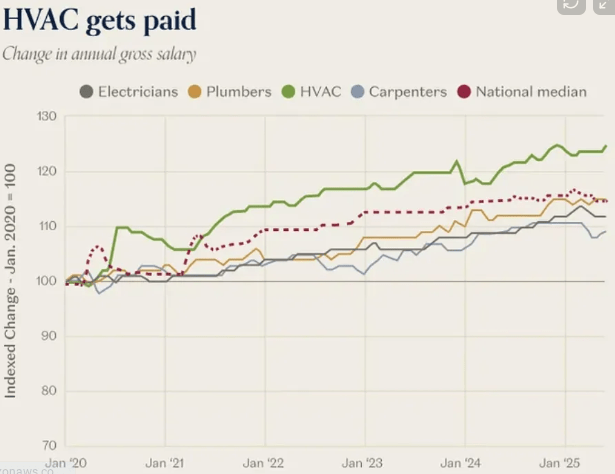

Weird things happen to economies when you have huge bursts of productivity that are concentrated in one industry. Obviously, it’s great for that industry, because when the cost of something falls while its quality rises, we usually find a way to consume way more of that thing – creating a huge number of new jobs and new opportunities in this newly productive area.

But there’s an interesting spillover effect. The more jobs and opportunities created by the productivity boom, the more wages increase in other industries, who at the end of the day all have to compete in the same labor market.

Our explosion of demand for data centers means there’s infinite work for HVAC technicians. So they get paid more (even though they themselves didn’t change), which means they charge more on all jobs (even the ones that have nothing to do with AI). Furthermore, the next generation of plumber apprentices might decide to do HVAC instead; so now plumbing is more expensive too. And so on.

Academics have published new research on the impact that Short Form Videos (SFV) like TikTok, Instagram Reels and Youtube shorts have on cognitive and mental health. The report systematically reviews and analyzes 71 studies involving over 98,000 participants.

SFV use is linked to poorer cognitive performance, with the strongest deficits in attention and inhibitory control, suggesting users struggle to focus and suppress impulses.

Frequent exposure to fast-paced, highly rewarding SFV content may rewire attention systems, fostering “rapid disengagement” from tasks that are slower or require sustained effort, reducing cognitive endurance over time.

SFV use is associated with poorer overall mental health, with the strongest links to stress and anxiety, indicating consistent emotional strain among heavier users.

Heavy SFV use reinforces impulsive engagement loops driven by dopamine rewards, contributing to compulsive scrolling and difficulty disengaging, patterns resembling behavioral addiction.

Short-form video consumption is associated with poorer sleep quality, especially when used at night, due to overstimulation and blue light disrupting melatonin, which can worsen mood and cognitive functioning.

Higher SFV use correlates with increased loneliness and reduced life satisfaction, as digital interactions replace real-world social connection for some users.

Negative effects occur across both youth and adults, meaning the cognitive and emotional risks of SFV use are not limited to developing brains; adults experience similar declines and mental health associations.

_______________________________

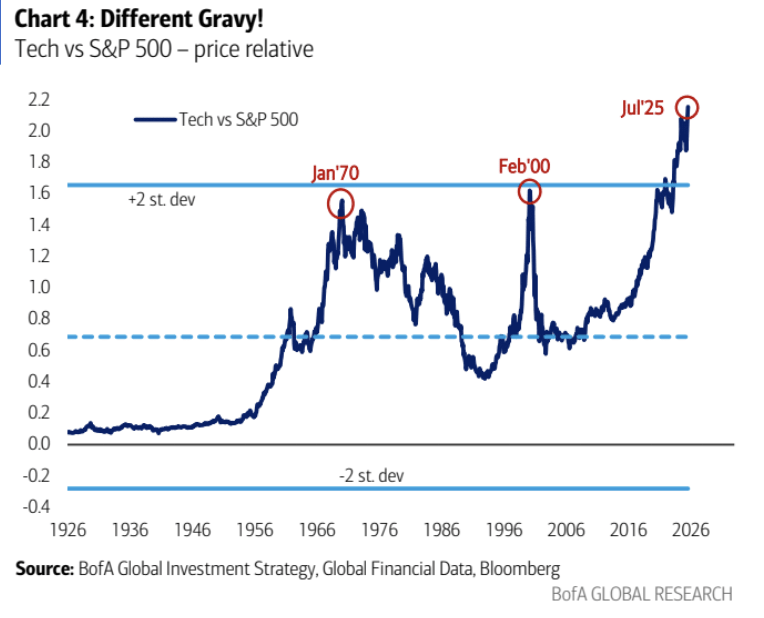

These days, it’s all stocks all the time, with reputable authorities calling on small investors to put everything they have saved into equities. Older investors are reminded of the mantra so common in 1999: “Every penny you don’t have invested in stocks will hurt you.”

More than a generation ago, financial historian Peter Bernstein wrote about investors’ “memory banks,” the market experience that accumulates in their hippocampi over their investing lives and molds their investment strategy. As he put it, looking back on the 1990s: “Most of the new participants in the market had no memory of what a bear market was like.”

And here we are today, almost seventeen years into a great bull market. Rather like 1999, also seventeen years into a long-term bull market, or 1966, once more seventeen years. Or 1873, sixteen years in, or 1837, eighteen years in, or 1893, twenty years in — to name a few of the notable tops over the past two centuries. Just long enough to produce empty memory banks in just enough investors.

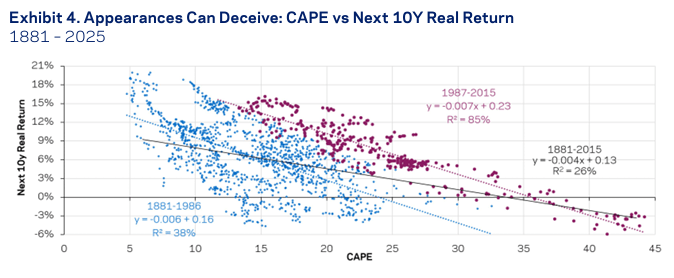

Historically, valuations have been a useful (though not perfect) indicator of real returns over the following decade. Below, you’ll see historical CAPE readings (in black) for the U.S. market alongside their corresponding forward ten-year real returns (in green). The conclusion is straightforward: when valuations are low, future returns tend to be above average; when valuations are high, forward returns tend to be much more muted.

Right now, the U.S. market sits at a CAPE ratio of around 40. It’s nearly double the long-term average of roughly 20, and the second most expensive in history.

historically, when valuations have climbed to this level, the following decade hasn’t been kind to investors. Not once has a country that ended a year with a CAPE above 40 produced positive real returns over the next ten years. That’s not a personal opinion but what the data shows.

To get a sense of what current valuations might mean going forward, I ran a linear regression using historical CAPE data and forward ten-year real returns. The relationship is remarkably consistent: as valuations rise, future returns fall. At today’s valuation levels, the regression suggests an expected real return of -2.46% for the next decade. From a historical perspective, the last time we were at the CAPE reading we find ourselves in today, the market went on to lose -2.11% per year for the next ten years.

Valuation isn’t the only red flag flashing. Today, about 40% of the market is concentrated in its 10 largest companies. This is the most concentrated the market has ever been.

Concentration itself isn’t a bearish sign. What really matters is how concentration changes going forward. Rising concentration tends to coincide with strong market performance as leading firms continue to gain share and deliver growth. On the other hand, when concentration starts to fall, this means your largest players are underperfoming the rest of your portfolio, and that’s when returns have historically suffered. If the biggest names continue to pull away from the pack, the market could remain strong for a while. But if that leadership falters, history suggests the unwind can be painful.

A few highlights from one of the best articles I’ve read this year discussing the private equity/credit bubble:

The golden age of Private Equity – at least from the standpoint of investor returns (FUM and thus fees to sponsors were significantly lower) – was during 1980-2000, and at a slight stretch, to around the time of the Great Financial Crisis in 2008. During this era, PE delivered legitimately good returns – in some cases outstandingly so. What enabled it was that it was still a niche industry where there was a limited amount of capital chasing deals, while the backdrop was conductive.

In contrast to the 1980-2000s, private equity funds from the 2010s began paying a premium to public market valuations for (typically) small, subscale and illiquid businesses. The problem was that the same thing that always happens when too much money floods into an area happened – bidding competition heated up, target prices rose, and the opportunity that previously existed rapidly disappeared (though the vehicles’ high fee structures of course remained firmly intact). Not surprisingly, since the 2010s, and perhaps as far back as 2006, outcomes have dramatically changed, and PE has delivered generally disappointing returns and underperformed listed equities, and the magnitude of that underperformance has significantly worsened since 2022.

Warren Buffett has scrutinized PEs return calculations and found them to be “well, they’re not calculated in a manner that I would regard as honest.” All kinds of tricks can be and are used to inflate apparent relative returns. PE will often lock up commitments from investors years in advance, and only “call” the funds much later after a deal is done. The IRR calculations only include the period during which the funds are working, but investors need to keep cash in reserve as it can be called at any time, meaningfully diluting effective returns to investors.

The much bigger elephant in the room – the PE industry is currently “marking to model” and is sitting on a vast number of assets it is unable to sell – even in a bull market – because the marks are unrealistic. This will be meaningfully inflating claimed trailing returns, which remain mostly unrealized.

If you look at who private equity companies hire, it is typically ex investment bankers. These guys are deal makers and spreadsheet jockeys, not operational people, and there is no reason to believe they have any unique insights on the intricacies of running small, niche businesses, where specialized skills and decades of domain experience generally count for a lot more than general smarts.

Not to mention that as the industry has mushroomed in size, the average quality of the average hire has meaningfully degraded. Investment bankers also generally lack investment acumen. They are deal makers – a different skill set entirely.

Going even a step further – it’s probable that private equity ownership not only fails to deliver operational improvements, but very likely on net makes the operational performance of companies worse, particularly in the long term. The most obvious means by which this occurs is by saddling investees with significant levels of debt, as well as implementing wholesale asset stripping (such selling and leasing back real estate) and cutting operational costs and capital expenditures to the bone. They frequently don’t just cut the fat, but the muscle as well.

If you are apt to under invest and run the business for maximum cash extraction in the near term, jacking up prices, lowering service quality, squeezing employees, alienating customers and opening the door to competitor inroads – it may improve near term cash generation, but it often comes at the cost of long-term value degradation.

PE has now taken over a large portion of Las Vegas, for instance, and visitors routinely complain of high prices, poor customer service, and the removal of perks such as free drinks that previously endeared visitors to the strip. Visitation has been waning, and people complain Vegas has lost its charm, and has become overpriced and soulless, a victim of “corporate greed.”

This is far from the only example. Employees and customers of PE backed hospitals and dental practices often complain of declining service standards, high prices, and a significant increase in unnecessary treatments unethically prescribed to boost near term utilization/billing.

The fair value of the combined $5 trillion of assets held in the US Private Equity/Credit industry is probably worth only about 60% of that in reality – a $2 trillion hole. When that hole is exposed, it will change economic behavior, and likely to a noticeable degree.

(1) The number of 55+ yard field goals has increased by 3x since just 2022:

(2) Between longer field goals and the dynamic kickoff, the field has basically been shortened by 10-15 yards.

(3) Quarterback passer ratings are tied for their highest-ever at 93.6:

(4) For the first time in NFL history, quarterbacks as a collective are gaining enough rushing yards to outweigh the yards they lose from sacks:

(5) Analytics have teams successfully attempting and completing fourth down conversions:

(6) Rushing plays on 4th-and-short are being attempted (and succeeding) at extremely high rates. The tush push effect:

_______________________

If you’ve ever received a spammy text falsely alerting you to an unpaid toll or failed delivery, it might have come from a so-called Phishing-as-a-Service network that Google is now trying to take down. In just 20 days, Google alleges, Lighthouse was used to spin up 200,000 fraudulent websites to attract over a million potential victims. It estimates that somewhere between 12.7 million and 115 million credit cards in the US were compromised by the scam.

Hyperscalers (Microsoft, Amazon, Google, Oracle, IBM) believe they might build God within the next few years. That’s one of the main reasons they’re spending billions on AI, soon trillions. They think it will take us just a handful of years to get to AGI—Artificial General Intelligence, the moment when an AI can do nearly all virtual human tasks better than nearly any human.

They think it’s a straight shot from there to super-intelligence—an AI that is so much more intelligent than humans that we can’t even fathom how it thinks. A God. The arguments to claim we’re about to make gods are:

AI expertise is growing inexorably. Threshold after threshold, discipline after discipline, it masters it, and then beats humans at it.

We’re now tackling the PhD level.

In the current trajectory, we should reach AI Researcher levels soon.

Once we do, we can automate AI research and turbo-boost it.

If we do that, super-intelligence should be around the corner.

Imagine you are a new college grad from a middle-class family. If you are lucky, you have no education debt, but many do. If you are lucky, you land a 100k+ job, but many don’t. Even if you are lucky, you still look up at astronomical asset prices (houses) and try to work out how you can maybe afford one in 20 years, with the understanding that they will only continue to go up in the meantime.

You are surrounded by online examples of success (usually fake or survivorship bias). Your attention span has been fried by TikTok and YouTube shorts. You simply don’t have the patience or discipline for the slow path.

So instead, you start taking outsized risks with your monthly paychecks – crypto, options, meme stocks, meme coins, sports betting. Your rationale is that this current amount could never buy a house, but if you win it might. And if you lose, you simply have to wait a week or two before you can reload and try again. This is “hyper-gambling.”

The obvious downside of taking repeated high-risk investments is that most will fail in this lottery strategy, and if you find yourself at the end of the tunnel with no diamonds to show for it, you will be even farther behind.

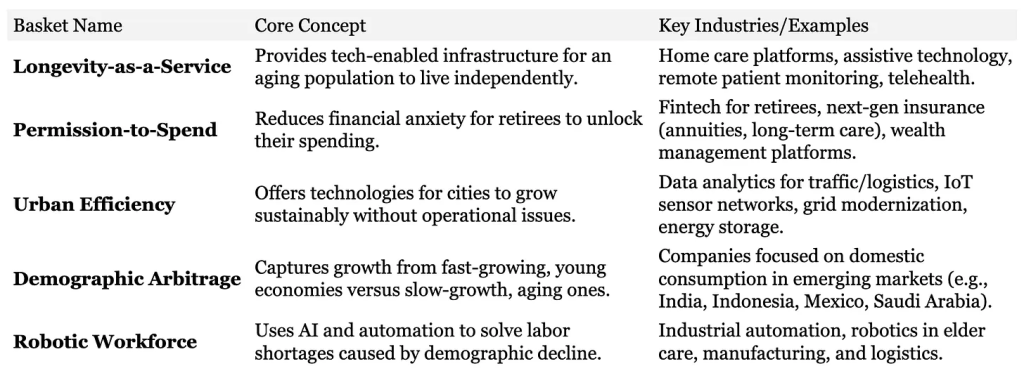

Between 2015 and 2050, the proportion of the global population over 60 is set to nearly double, climbing from 12% to 22%. The most extreme changes though, are happening at the upper end of the age spectrum. The number of individuals aged 80 or older is projected to triple between 2020 and 2050, reaching 426 million. This is exponential acceleration, and two-thirds of the world’s elderly will live in developing nations, up from just over half today.

Running parallel to the aging of the globe is a second, equally powerful human migration: the mass movement into cities. Today, 58% of the world’s 8 billion people live in urban areas. By 2050 this figure is projected to climb to 70%. Nearly 90% of this 2.5 billion-person increase in cities will occur in Asia and Africa. India, China, and Nigeria. are projected to account for over a third of all new urban dwellers globally.

President Clinton noted in his January 2000 State of the Union speech:

“We begin the new century with over 20 million new jobs; the fastest economic growth in more than 30 years; the lowest unemployment rates in 30 years; the lowest poverty rates in 20 years; the lowest African-American and Hispanic unemployment rates on record; the first back-to-back surpluses in 42 years; and next month, America will achieve the longest period of economic growth in our entire history.”

That wasn’t an exaggeration. But it marked the beginning of the worst decade for the U.S. stock market in modern times.

In January 2010, President Obama noted in his State of the Union speech:

“One in 10 Americans still cannot find work. Many businesses have shuttered. Home values have declined. Small towns and rural communities have been hit especially hard. And for those who’d already known poverty, life has become that much harder.”

That wasn’t an exaggeration. But it marked the beginning of one of the best 15 years (and counting) for the U.S. stock market in history.

In the last two decades, the share of American adults who say they exercise or play sports on any given day has increased by about 20 percent.

The share of Americans who say they don’t regularly work out or play sports, which SFIA calls the “inactivity rate,” has fallen by more than one-fifth since 2019.

Rich and young Americans exercise the most. Poor and older Americans work out the least. Among adults, income predicts activity better than age.

The increase in exercise minutes is significantly led by young people and women over 65, who increased their weekly workouts by about twice as much as men over 65.

No fitness activity saw a larger increase in participation between 2019 and 2024 than Pilates. Yoga and barre were close behind among the fastest-growing activities. Meanwhile, group cycling, cardio kickboxing, boot camps, and cross-training workouts like CrossFit got walloped by the pandemic, and they haven’t bounced back. In general, Americans seem to have traded sweaty group classes for gentler core work.

After persevering through a valley of tears since 2010, value investors are finally beginning to reap a fruitful harvest in developed international markets. Over the past five years, the value premium has returned to positive territory in international markets as value stocks have returned to outpacing growth stocks. Since July 2020, value has outperformed growth by 11.6% annualized in developed international markets:

Mastroianni: It seems like the takeaway from this research that has been done over the past 10 years or so is that people are way too negative about their own social abilities and the things that are likely to happen when they talk, especially to someone new. So, for instance, they underestimate how pleasant it’s going to be to talk to someone new. But even afterward, when we ask them, hey, how much did you like that person? They say oh, I like them a lot. And when we ask, how much did they like you? Oh, less than that. I ran one study with some friends of mine where we had people talking groups of three and we’re like, okay, how much did you like them? People would say 5 or 6 out of 7. And how much did they like you? People would say 4 or 5 out of 7. On average, people thought they were the least liked person in the conversation, which obviously can’t be true for each person.

Thompson: We are, on the one hand, the social animal. Yet we delude ourselves about the degree to which we’re a fun hang. We’re the social species and we’re the socially anxious species as well.

Mastroianni: Yeah, well, we’re the ones who care about it the most. And so we have the most to lose. And so we worry about it the most in part in the hopes that maybe it makes us better at doing it. The way I think about it is in our evolutionary history, we lived in groups. But how often did we meet someone who we literally had no connection to before? I can’t imagine it was all that often. But today it can happen literally every day. You get on the bus and it’s full of people that aren’t related to you. You don’t know them. They don’t know you. That’s a really weird thing to do.

____________________________________

Morgan Stanley surveyed all stocks trading on U.S. exchanges over a 40-year period, between 1985 and 2024. They found the median stock experienced a decline of 85% at one point or another. Worse yet, more than half of these stocks never fully recouped their losses. The median stock recovered to just 90% of its prior high-water mark. Among those stocks that were able to reclaim their prior highs, it was a long process—about five years, on average.

Those numbers only apply to the median stock, but suppose you had above-average stock-picking skills. How would things have turned out? If you had the foresight to pick the 20 best performing stocks over that 40-year period, at some point they still would have delivered an average agonizing draw-down of 72%.

It’s hard to remember, but Apple dropped 83% at one point. Nike once lost 66%. Even Nvidia, which was the best performing stock over the past 20 years through 2024, lost more than 90% at one point. And most notably, Amazon was once down 95% from its prior high.

Over the long term, share prices tend to move in tandem with corporate profits. When a company’s earnings increase, often its share price does too. The problem is that prices are only sometimes rational. Very often, stock prices disconnect from corporate earnings, and the gap can be significant.

This was first proven empirically Daniel Kahneman and Amos Tversky. In 1974, they published a paper that found investors exhibit an “availability heuristic.” That is, they tend to rely on the information that is most available. That’s a problem because the information that happens to be most available isn’t necessarily the information that’s the most accurate or even relevant. Often, the information that happens to come to mind is the information that’s most vivid. In other words, extreme information or news becomes most memorable, and thus drives decision-making.

___________________________

ChatGPT users may want to think twice before turning to their AI app for therapy or other kinds of emotional support. Sam Altman, OpenAI’s CEO:

“People talk about the most personal sh** in their lives to ChatGPT. People use it — young people, especially, use it — as a therapist, a life coach; having these relationship problems and [asking] ‘what should I do?’ And right now, if you talk to a therapist or a lawyer or a doctor about those problems, there’s legal privilege for it. There’s doctor-patient confidentiality, there’s legal confidentiality, whatever. And we haven’t figured that out yet for when you talk to ChatGPT. This could create a privacy concern for users in the case of a lawsuit, because OpenAI would be legally required to produce those conversations today.“

The 1990s were a turning point for country’s mainstream acceptance, driven by two mutually reinforcing phenomena:

Improved Telecommunication Infrastructure: The Telecommunications Act of 1996 enabled American media companies to consolidate regional stations into national networks, facilitating country radio play outside of rural strongholds. Simultaneously, enhanced geographic radio coverage brought consistent access to under-served rural listeners. Together, these infrastructure improvements fostered a virtuous cycle: greater airplay propelled more country songs onto the charts, which in turn drove even more airplay.

Country Crossover Successes: Country crossovers like Garth Brooks, Shania Twain, and Tim McGraw blended conventional genre staples with accessible pop and rock influences, broadening the format’s appeal beyond its traditional fanbase.

______________________________________

Something unusual—and incredibly fast—is happening with teenagers running the 100-meter around the world. From Japan to the U.K., young speedsters are posting eye-popping times in track’s most prestigious event. What’s driving these turbocharged athletes who aren’t old enough to vote?

Peter Bernstein liked to say that investors have memory banks: the market returns collectively earned by people of similar age. Experience shapes expectations. The problem is that your memory bank can deceive you in dangerous ways. Your experience of the past is a reasonable guide to the future only if the future turns out to resemble the portion of the past that you’ve lived through. And it often doesn’t. It’s worth looking at a few investing beliefs that your memory bank might hold—and asking whether they’re still valid.

_______________________________

How much longer will emerging markets be undervalued and hated?

________________________________

Nasdaq Price to Earnings valuations are at the very high end of their historical range. That means they are extremely expensive.

While countries like the United States and India are extremely expensive relative to the rest of the world, the global stock market as a whole has seen its P/E ratio rise dramatically from the early 2010s.

_______________________________

Looking at Enterprise Value (EV) divided by sales, we’re not above the 2000 and 2021 bubble peak for global stocks:

“When (Charlie Munger and I) were born the odds were over 30-to-1 against being born in the United States. Just winning that portion of the lottery, enormous plus. We wouldn’t be worth a damn in Afghanistan. We won it partially in the era in which we were born by being born male. We won it in another way by being wired in a certain way, which we had nothing to do with, that happens to enable us to be good at valuing businesses. And you know, is that the greatest talent in the world? No. It just happens to be something that pays off like crazy in this system.”

If you had invested from 1960 to 1980 and beaten the market (the S&P 500) by 5% each year, you would have made less money than if you had invested from 1980-2000 and under-performed the market by 5% every year. When you start investing can be more important than anything else.

_______________________________________

For years, 529 accounts were synonymous with college savings plans. But recent updates have given the accounts a makeover. They’ve become education savings accounts, not just college savings accounts. The latest change allows the accounts to be used to help pay for a broader range of post-high school credentials, like certification in specialties like auto mechanics or food safety,and related expenses.

Population ageing and decline is one of the most powerful forces in the world, shaping everything from economics to politics and the environment. It it implies the goal is the same today as it was in the past: finding ways to encourage couples to have more children. A closer look at the data suggests a whole new challenge.

Take the US as an example. Between 1960 and 1980, the average number of children born to a woman halved from almost four to two, even as the share of women in married couples edged only modestly lower. There were still plenty of couples in happy, stable relationships. They were just electing to have smaller families.

When you ask people, “What builds wealth?” you get a wide variety of answers. Some will tell you it’s mindset. Some will say work ethic. Some will say it’s spending. And a host of other explanations. If you could have just one piece of information on somebody to predict their future wealth, what would it be? Would you ask for their IQ? Whether they went to college? How about their parents’ education level?

The answer is the most obvious and straightforward: For someone of working age, their income is the best leading indicator of wealth. What leads to higher income? Hard work, connections, and luck are important, but high earners tend to follow one of four distinct paths. These paths won’t guarantee success, but they are where high incomes tend to cluster:

Sales and Persuasion

Technical/Analytical Skills

Advanced Degrees/Credentials

Entrepreneurship and Business Building

______________________________

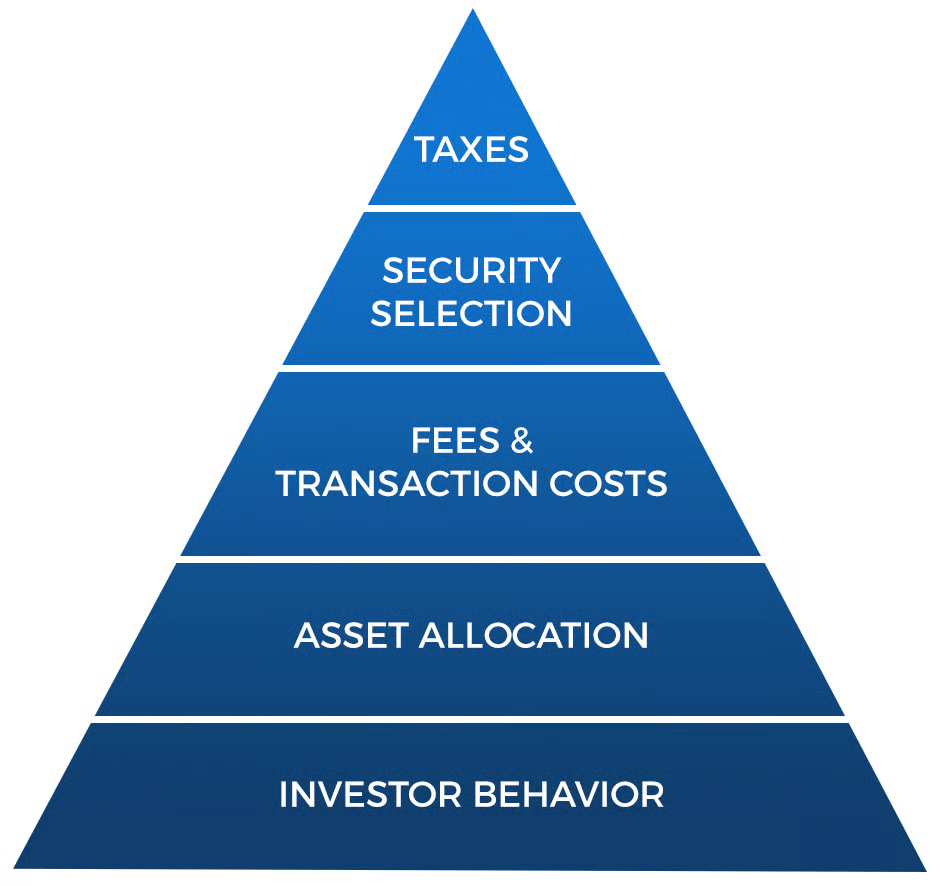

Some investing skills have to be mastered before any other skills matter at all. There is a hierarchy of needs.

At the foundation of this hierarchy are the boring but essential behaviors: living below your means, having an emergency fund, staying invested during downturns, and picking a reasonable asset allocation. These things aren’t exciting. They won’t get you likes. But they will carry you through decades of compounding.

Higher up the hierarchy are things like choosing the right stocks or funds and minimizing fees. These are useful, but only after the foundation is strong. Otherwise, you’re just rearranging furniture in a house with shaky walls.

The Federal Reserve did a study that looked into the financial habits of Canadians whose neighbors won the lottery. The neighbors of people who struck it rich were more likely to increase their spending, take on more debt, put more money into speculative investments, and eventually file for bankruptcy. And the larger the winnings, the more likely that others in that neighborhood would go bankrupt.

It’s in our flawed nature to compare ourselves to others, particularly people we see and interact with every day. Money insecurity leads us to compete and not appreciate what we have. Also true, though, is that the research shows one thing for certain: The Joneses aren’t very happy.

An examination of 259 different independent samples found that materialism was “associated with significantly lower well-being” and was a poor way of meeting psychological needs. The researchers’ findings suggest that this association holds across different demographics, participants, and cultural factors. Another meta-analysis of 92 studies found that those pursuing goals of growth, community, giving, and health experienced significantly higher levels of well-being than those pursuing the Jones-y goals of wealth, fame, or beauty.

You’ll never be content trying to keep up with the Joneses because there is an endless supply of them to keep up with. There are always people spending more money, taking nicer trips, buying bigger houses and making more money than you are.

There was another classic psychological study that compared lottery winners with people who were paralyzed in an accident. Surprisingly, the lottery winners weren’t significantly happier than the average person and actually reported less enjoyment from everyday experiences. The big win seemed to raise their expectations, which made small daily pleasures feel less satisfying.

In contrast, many accident victims rated themselves as moderately happy, despite their life-altering injuries. While thinking about their past lives sometimes made them feel worse, they still found deep meaning and enjoyment in ordinary things because they appreciated them more. After major life changes, people adjust their expectations. Lottery winners adjusted upward and felt less satisfied. Accident victims adjusted downward and found more value in the little things.

Nothing was the same after June 28, 1914. The assassination of Archduke Franz Ferdinand triggered a chain of events that led to WWI and closed the NYSE for months. One month to the day of the assassination, Austria-Hungary declared war. Three days later, Henry Noble, president of the NYSE, closed the exchange. Other regional U.S. exchanges in Chicago, Baltimore, San Francisco, Philadelphia, and other cities followed suit. Most major exchanges around the world closed too.

Noble knew that wars demanded funds. Foreign investors could make a run on the exchange, selling securities to raise cash. The cash could then be converted into gold and shipped back to Europe. That put the U.S., being on the gold standard, in a tricky spot. Depleting the U.S. gold reserves would put faith in the dollar and adherence to the gold standard at risk.

June 28, 1914 – Archduke Ferdinand assassinated. Dow closes the next day at 57.9.

July 28, 1914 – Austria-Hungary declares war on Serbia – World War 1 begins: Dow closed 55.3.

July 30, 1914 – Dow closes 51.7.

July 31, 1914 – NYSE & regional U.S. exchanges close the markets

December 12, 1914 – NYSE reopens stock market with trading limitations.

December 14, 1914 – Dow closes 56.8.

December 14, 1915 – Dow closes 98.3.

When the stock market reopened December 12, 1914, investors had four and a half months to reassess the business environment in war time. And business was good. Over the next 12 months, the Dow soared 73% (Dec. 14, 1914, to Dec. 14, 1915, not including dividends). The U.S. became the main food and war supplier for the Allies war effort. Companies like U.S. Steel and DuPont saw profits explode 5x and 10x respectively, in a year. Dividend payments did the same. WWI is the perfect example of why geopolitical events are hard to predict. The market reacts in unexpected ways during scary confusing times.

______________________________

Reciprocity is a deeply human thing, and it applies directly to the nature of interest. If you show someone that you’re interested in them, they will reciprocate that curiosity by revealing what makes them so interesting. Believing that someone is boring is a failure of recognizing jthat fact. Boredom is almost always the result of a lack of curiosity, or the inability to see anything or anyone through the lens of a question. In a way, boredom is arrogance. It’s the acceptance of the belief that nothing is worth your interest because you already know what you need to about yourself, others, and the world. A curious mind is a humble one, as a prerequisite for curiosity is the acceptance that there is more to life than what you think you already know.

____________________________

We are a story-driven species. From cave walls to balance sheets, we look for narratives that explain the world and our place in it. And nowhere is this tendency more dangerous than when we only learn from the winners. When we allow survival alone to imply superiority. When the fact that someone or something made it through becomes enough proof that they knew what they were doing.

This is the essence of survivorship bias, and in the world of investing, it distorts almost everything. Consider the stock market, which is full of visible winners. We often hear stories of stocks that went 20x, fund managers who outperformed for a decade, companies that pivoted into success, and investors who became celebrities.

What about the others? The ones who didn’t make it? They’re barely mentioned, rarely studied, and almost never remembered. And so, the narrative we inherit is hopelessly incomplete.

Then there’s the most seductive arena of all: success stories. Business books, biographies, and podcast interviews are all proudly built on the same question: “How did you do it?”But that question, when asked only of survivors, creates a dangerous narrative. It turns randomness into wisdom and luck into method.

A founder who succeeded against all odds is praised for her vision, her grit, and her intuition. But what about the 100 others who had the same qualities and failed? What about the timing, the macro conditions, the investor interest, the random tailwinds that no one could have planned? None of that gets included in the final story. And so we start to think: this is how success works. This is the roadmap. Just do what she did.

Barry: You’ve covered human behavior and human nature, what led you to say, I wanna write a new book about the art of spending money?

Morgan: I didn’t call this book The Science of Spending Money because I don’t think that exists. Science implies that there is like a, a one size fits all rule for, for you and I, and that’s not the case. I call it the artist spending money because art is subjective. It is often contradictory. It is different from person to person, and that’s really what spending is. So much good ink has been spilled on how to invest, how to grow your career, how to earn more money, but very little on spending money.

Barry: There’s been a lot of academic research: Does money make you happier?

Morgan: What a lot of the research shows is that if you are already a happy person, money can make you happier. But if you are a depressed person – or a miserable person, whatever it might be – that it will not, and it’s easy to just kind of contextualize this into a real person’s life of if you are in a bad marriage and you hate your career and you have a two hour commute and just go on down the list, you’re an alcoholic, you’re obese. If you take that person and you give them more money, will they be happier? The answer is no, of course not, because all of those other aspects of their life are gonna override whatever money can do for them.

But if you also take somebody who’s in a great marriage loves their career, they’re happy, they’re healthy, they sleep eight hours, they have a good set of friends – and you give that person more money, there’s a good chance that they’re gonna use that money to just leverage what they’re already doing. To spend more time with the friends who they already love, to spend more time getting healthier and eating good food.

Barry: One of the interesting things in the academic literature that I recall seeing a few years ago was when they draw these charts of money potentially making people happier, Divorce is a giant red flag. People in the middle of a divorce or people who have recently been divorced, that’s a really challenging road to haul, isn’t it?

Morgan: I think what it comes down to is that having more money is so quantifiable that we use it as a crutch for all of our problems. For example, if I said I would have a better life if I was a 10% better dad. What does that even mean? What does a 10% better Dad mean? There’s no way to quantify it, but if I said I would have a better life if my salary went up by 10%, you can easily quantify that, wrap your head around it. So we chase that and we assume that that’s gonna be the solution to all of our ills. Becoming a better dad might make me a happier, better person, but since it’s impossible to quantify, I just ignore it and pretended that it doesn’t exist.

Barry: You alluded to impressing others. How should people avoid spending money for status and symbolism as opposed to bringing themselves satisfaction and happiness?

Morgan: It is so easy to overestimate how much other people are looking at your stuff, your house, your cars……they’re not paying any attention. They’re busy worrying about themselves and thinking about themselves. And so when you frame it like that – it’s not to say don’t use your money to gain attention – it’s use it to gain attention from the very small core group of people who you want to love you. There’s a great quote from Warren Buffett where he says, “The definition of success in life is when the people who you want to love you do love you.”

Barry: The person driving down the street in the loud Lamborghini or the person around the corner from you with a giant house? You are only seeing one half of the balance sheet. You’re only seeing their assets. Did they pay cash for that or did they go deep into debt in order to buy a house or a car to show off for the neighbors? Talk about that a little bit.

Morgan: Wealth is what you don’t see. Wealth is the cars that you didn’t purchase and the giant house that you didn’t buy. That’s what wealth is. It is money that you didn’t spend that you can now save for either for future consumption or for independence today. I can see your car, I can see your house, I can see your watch and your clothes. I cannot see your bank account or your brokerage statement. So the most important part of wealth – literally in my view, the definition of wealth is invisible to everybody.

Think about physical fitness. You can see somebody’s physique, it’s right there. And so you know who to admire and who to chase. “Oh, that, that person’s in great shape. I should ask them what they do. I should ask them their diet and try to mimic what they do.” But if you see somebody with a mansion or a Ferrari or whatever it is, you don’t know they got that by success. That may be the picture of a leverage. It’s possible they haven’t slept in two weeks because they’re wondering how they’re gonna make their next Ferrari lease payment. And so we have a fake view of who we’re chasing and what we should do, because wealth that we’re chasing is invisible.

During the month following Lehman Brothers’ September 2008 implosion, then Federal Reserve Chairman Ben Bernanke testified to the House Committee on the Budget on Monday, October 20, 2008. He reminded members that the Federal Reserve’s charter was to maintain high employment and low inflation. The Fed, he also reminded, was not authorized to manage the stability of the financial system or keep credit markets flowing; it was not the FOMC’s charge to address any of the myriad issues that had endangered the financial system’s functioning.

A fiery speech from someone (maybe Rand Paul?) led to a vote against Bernanke’s funding and authority request. He would not be getting the tools necessary to unfreeze credit and keep the banking system operating.

Sayeth Mr. Market: “Hold My Beer.”

The sell-off began immediately after the vote; over the next five trading days, from recent highs, the S&P 500 fell 13.9%, the Nasdaq was right behind it at 13.5%, and the Russell 2000 crashed 18%. MOSTLY IN ONE WEEK. Congress reconvened and passed both the necessary authority and the dollars that the Fed chairman had requested. By November 4th, all of the losses had been made up and then some.

Don’t fix the credit markets, and put corporate revenue and payrolls at risk? FAFO.

______________________________

Behind a paycheck, the largest source of income for the 1% highest earners in the U.S. isn’t being a partner at an investment bank or launching a one-in-a-million tech startup. It is owning a medium-size regional business. Many of them are distinctly boring and extremely lucrative, like auto dealerships, beverage distributors, grocery stores, dental practices and law firms.

The analysis of anonymized tax data from 2000 through 2022 suggests the importance of such business ownership to the U.S. economy has grown. The share of income that ownership generates has increased to 34.9% in 2022 from 30.3% in 2014 for the top 1% earners. It has increased even more at the topmost levels. The top 0.1% highest-earners saw 43.1% of their income come from such business ownership in 2022, compared with 37.3% in 2014. (The minimum income threshold in 2022 to qualify for the top 0.1% of earners was $2.3 million).

The growth of this growth can be attributed in large part to tax cuts in recent decades for such business owners and low interest rates that have boosted company valuations. The number of such business owners worth $10 million or more, adjusted for inflation, has more than doubled since 2001, to 1.6 million as of 2022. The growth has been in S-corporations and partnerships, where the profits and losses of the business flow through to the owners or partners; the business itself doesn’t pay taxes. The typical medium-size business they studied has annual sales of $20 million and 100 employees.

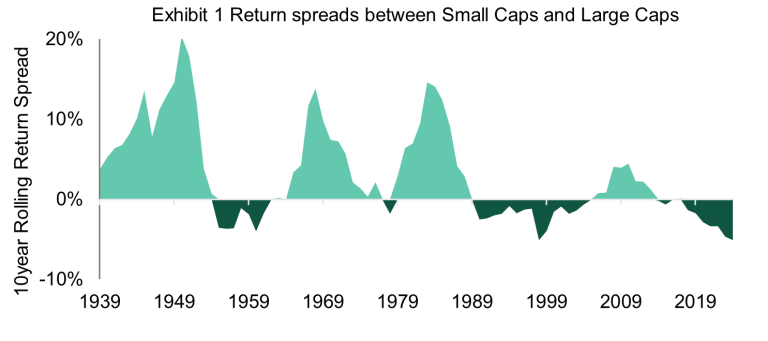

Small-cap underperformance has historical precedent — but cycles turn. We’re in the 12th year of a small-cap lagging cycle, longer than average. Historical data suggests a reversal is near.

Higher interest rates are reigniting migration. With rates expected to stay elevated, small-cap stocks are more likely to graduate to large caps — boosting overall performance potential.

Valuation and quality favor small caps. Compared to the weakest segment of large caps, small-cap stocks offer stronger return on assets and more attractive price-to-book ratios, contradicting the view that only low-quality names remain in the space.

_____________________________

The MSCI ACWI index includes large and mid-sized companies from 23 developed countries (like the U.S., UK, Japan) and 24 emerging markets (like China, India, Brazil). It covers about 85% of the available stocks around the world. The number of stocks in the MSCI ACWI that do business globally has risen to 80% (which is why the global stock market did not respond well to the recent tariff announcements).

About 70% of Nevada gaming revenue is from slot machines and the majority of players are locals. In 2024, Nevada casino games won $15.6 billion from players with $10.5 billion coming from slot machines. It’s a jarring figure when put into perspective with other forms of entertainment (here’s a comparison: the entire US box office in 2024 was $8.5 billion).

Slot machines are the new crack cocaine of high-tech gambling. The most addicted players don’t even play to win. Rather, they play to be in a trancelike state called the “machine zone” where daily worries, social demands, and even bodily awareness fade away.

Meanwhile, the North Star metric for casinos is maximizing the players “time on device” by designing technology with a deep understanding of human psychology. If this all sound somewhat familiar, it’s because the exact same playbook has been used to make our smartphone apps as addictive as possible.

Recency bias – When you give more weight or importance to recent events.

Loss aversion – The most important concept in finance. Losses hurt twice as bad as gains feel good.

Confirmation bias – Seeking opinions or data that agree with one’s pre-existing beliefs.

Anchoring – When a default starting point influences your conclusions.

Hindsight Bias – The assumption that the past was easier to foresee than it actually was.

Endowment Bias – When you place a higher value on something you possess.

Gambler’s Fallacy – When you see patterns where none exist in sequences of random events.

Illusion Of Control – The belief that you have control over uncontrollable outcomes.

Sunk Cost Fallacy – When your decisions are determined by investments that have already been made.

___________________________

Studies show that decision makers exhibit a “memory premium:” they tend to things they can remember vs. ones they can’t, even when the latter are objectively better. The memory premium is associative, subject to interference and repetition effects, and decays over time. Even as decision makers gain familiarity with the environment, the memory premium remains economically large. The ease with which past experiences come to mind plays an important role in shaping choice behavior.

When you go to the doctor, you’re probably the one answering most of the questions. Yet it’s essential to make sure you’re asking plenty of your own. We need to get someone to fund a bazillion-dollar PSA to tell people to be bolder when they talk to their doctors. I see this over and over again: People aren’t asking any questions, never mind the right ones. We asked experts to share the questions you should ask your doctor to help you get well or stay that way:

“What are my treatment options, and how do they compare?”

“If this were your family member, what would you do?”

“What should I do if my symptoms get worse or don’t improve?”

“How many people with my condition have you treated?”

“Are there any new treatments, clinical trials, or emerging research that apply to my condition?”

“What screenings should I get?”

“What vitamins and supplements might be helpful?”

“When can I expect my test results, and how will I receive them?”

“Can you explain that in a way that’s easier to understand?”

In the spring of 2023, a London banker-turned-bookmaker reached out to a few contacts with an audacious request: Can you help me take down the Texas lottery? Bernard Marantelli had a plan in mind. He and his partners would buy nearly every possible number in a coming drawing. There were 25.8 million potential number combinations. The tickets were $1 apiece. The jackpot was heading to $95 million. If nobody else also picked the winning numbers, the profit would be nearly $60 million.

Marantelli flew to the U.S. with a few trusted lieutenants. They set up shop in a defunct dentist’s office, a warehouse and two other spots in Texas. The crew worked out a way to get official ticket-printing terminals. Trucks hauled in dozens of them and reams of paper. Over three days, the machines—manned by a disparate bunch of associates and some of their children—screeched away nearly around the clock, spitting out 100 or more tickets every second. Texas politicians later likened the operation to a sweatshop.

Trying to pull off the gambit required deep pockets and a knack for staying under the radar—both hallmarks of the secretive Tasmanian gambler who bankrolled the operation. Born Zeljko Ranogajec, he was nicknamed “the Joker” for his ability to pull off capers at far-flung casinos and racetracks. Adding to his mystique, he changed his name to John Wilson several decades ago. Among some associates, though, he still goes by Zeljko, or Z.

Minimum Levels Of Stress, a phenomenal new article by one of my favorite authors; Morgan Housel.

A day after the September 11th terrorist attacks, every member of Congress stood on the steps of the U.S. Capitol and sang God Bless America. Could you imagine that happening today? It’s easy to say no, given how nasty politics has become. But if America faced an existential crisis like 9/11 again, I think you’d see the same kind of unity return. There’s a long history of enemies putting their differences aside when facing a big, devastating threat. People get serious when shit gets real. If that sounds like wishful thinking to you, let me propose a reason why: Part of the reason today’s world is so petty and angry is because life is currently pretty good for a lot of people.

There are no domestic wars. Unemployment is low. Household wealth is at an all-time high. Innovation is astounding.

As the world improves, our threshold for complaining drops. In the absence of big problems, people shift their worries to smaller ones. In the absence of small problems, they focus on petty or even imaginary ones. Most people – and definitely society as a whole – seem to have a minimum level of stress. They will never be fully at ease because after solving every problem the gaze of their anxiety shifts to the next problem, no matter how trivial it is relative to previous ones. Free from stressing about where their next meal will come from, worry shifts to, say, a politician being rude. Relieved of the trauma of war, stress shifts to whether someone’s language is offensive, or whether the stock market is overvalued.

A summary and thoughts on the data from the author:

The typical woman is disgusted by the typical man

The typical woman is moderately disgusted by the median man

The typical woman is strongly disgusted by the bottom quarter of men

Men should stop taking rejection so personally. When the typical women rejects you, the problem isn’t so much that she finds you unappealing. The problem is that the typical woman finds almost all men unappealing.

Men should try harder to be less disgusting.

Women should try harder to be less disgusted. Most women eventually accept a guy who isn’t visibly attractive. Much of the reason is that superficially unappealing guys win them over with charm, humor, and devotion.

It’s not hard to use evolutionary psychology to explain why the typical man disgusts the typical woman: Since women’s maximum reproductive capacity is strictly limited, they’re evolved to be hypergamous, with a strong preference for mating with the best of the best.

__________________________________

Numerous studies show a strong relationship between stock market valuation and long-term subsequent returns. Since 1979, global stock market indices have been valued on average at a Shiller-CAPE of 20 and a price-to-book ratio (PB) of 1.9. Investors who invested at attractive valuations in recent decades were able to achieve above-average returns over the following 10-15 years. Those who bought at high valuations, on the other hand, were generally disappointed in the long term.

Here’s a look at where countries stand today. The lower left are the least expensive countries/stock markets and the upper right are the most expensive. You can see that India is off the charts expensive while the United States is in another solar system based on how overvalued it is.

What long-term stock market returns can investors expect in the 20 most important stock markets based on valuation?

Based on CAPE and PB, Latin America and Asia currently show the lowest valuations, particularly in Brazil, Korea and China. These equity markets are currently trading at a CAPE of 9-12 and a PB of 0.9-1.4.

Historically, comparably attractive valuations have been followed by above-average returns of 9-11% (in real terms) over the next 10-15 years.

In general, the emerging markets (with the exception of India) are currently valued much more attractively than the developed markets. Historically, comparable valuations in the emerging markets have been followed by annual returns of 7.7%, while the developed markets are expected to achieve rather low returns of 2.5%.

The low return expectations of the developed equity markets are caused by the extremely high US valuation: with a CAPE of 35.4 and a P/B ratio of 5.1, the US market is trading at around twice the level of recent decades. In the last 140 years, such high valuations have been followed by long-term returns of only 0.1% p.a.

Among the developed markets, Germany, Italy, Japan, Singapore, Spain, Norway and the UK still appear attractive. Investors here can expect annual returns of 7-8% in the long term here.