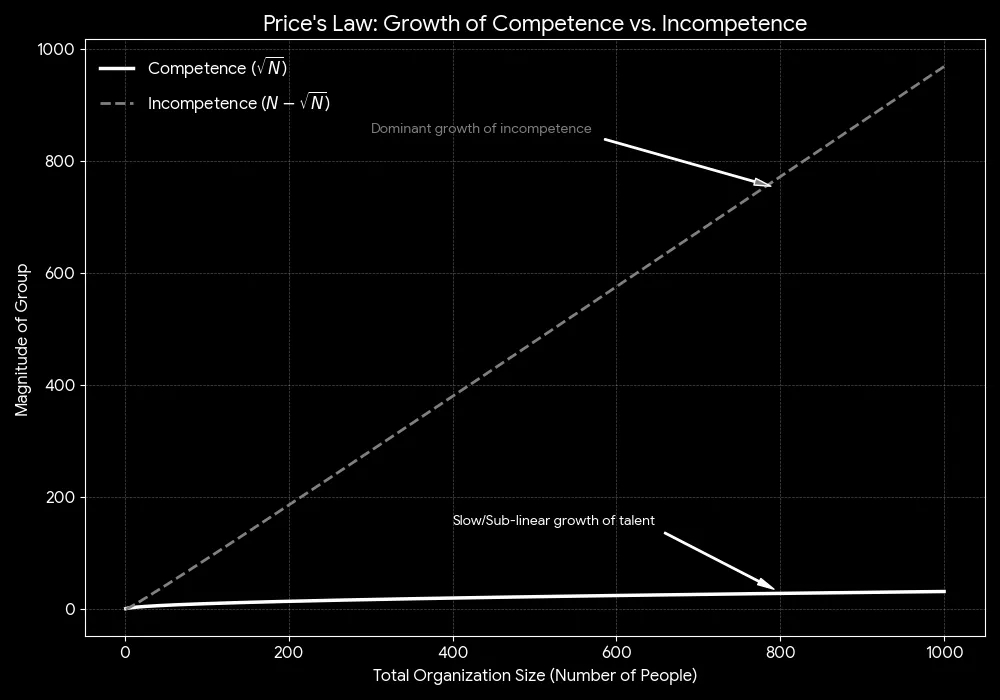

In 1963, a physicist named Derek Price was studying scientific publications, trying to understand why some researchers dominated their fields while others published and got zero attention. He found that the square root of the number of people in a domain does 50% of the work. Here’s what that looks like in practice:

- In a company with 100 employees, 10 people produce half the output

- In a field with 10,000 scientists, 100 produce half the meaningful research

- On a team of 25, 5 people carry the entire operation

It wasn’t exclusive to research papers—this pattern showed up everywhere he looked.

- Of the 30 million businesses in the United States, about 5,500 (the square root) generate half the total economic output.

- Spotify has about 11 million artists, but 50% of all streams are generated by only 3,300 artists.

- In astrophysics, the square root of stars in a galaxy produce half the light.

- In creative fields like YouTube, very few channels account for the vast majority of both views and ad revenue.

Price’s Law violates our egalitarian instincts. We want to believe everyone contributes equally, that effort equals outcome, that hard work is the great equalizer, but reality is far from it.

You need (1) skill, (2) consistency, (3) opportunity, and (4) luck all compounding in the same direction. Most people have one or two of those ingredients. The square root has all four.

Price’s Law reveals that equality of outcome and equality of opportunity cannot coexist in complex systems. Even if you give everyone the same resources, the same training, the same chance, outcomes will still stratify eventually. Some people will compound their advantages. Most won’t.

What does this mean in practice?

- You have dozens of skills, but √n of them drive half your value in the marketplace. The reason why we spend so much time trying to be “well-rounded” is because we’ve been lied to.

- If you work 40 hours a week, about 6 of those hours actually matter. The other 34 are maintenance, “busywork,” meetings that could’ve been emails, and a whole lot of goofing around.

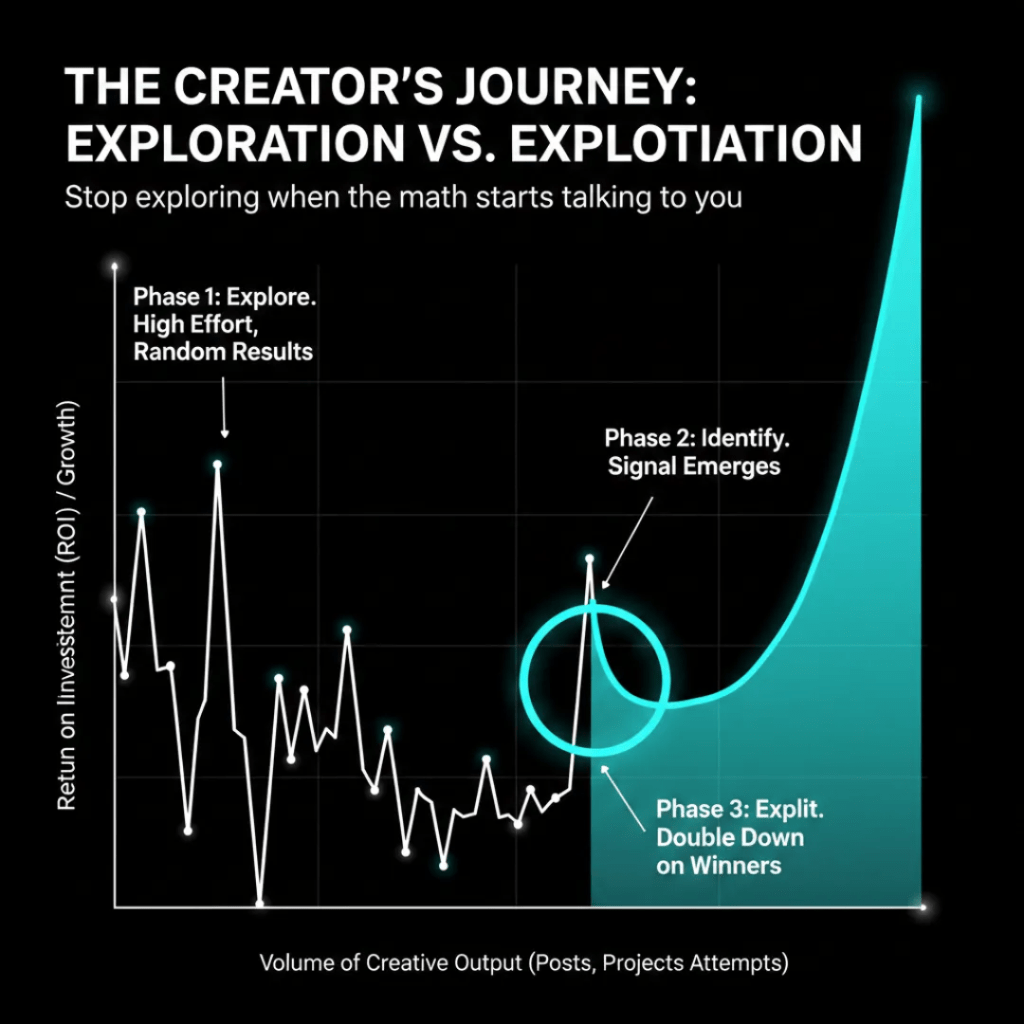

The paradox (why we still need to do the other 90%): you can’t know which skills are your multipliers without trying a bunch of skills. You can’t know which relationships matter without meeting a lot of people.

- The early game is exploration. You’re planting seeds everywhere, seeing what grows. Price’s Law hasn’t kicked in yet because you don’t have enough data.

- The middle game is identification. Patterns are emerging. “Oh, this is what works.” That’s your √n.

- The late game is exploitation. You double down on the winners. You cut out the losers. You focus your energy towards the best bets.

Explore the noise until you have signal. Then exploit that.

_______________________________

As of April 2026, Nike stock sat below US$45 – a market capitalisation of US$68 billion, its lowest level in over a decade, and a fall of more than 75% from the US$280 billion the company commanded at its 2021 peak.

How does what was once considered one of the widest consumer brand moats in the world, built over half a century, erode over the course of a few short years?

A good starting point is January 2020, when John Donahoe took over as Nike’s new CEO. The board wanted a digital-first operator, and Donahoe had the résumé – ServiceNow, eBay, and Bain – even if he was one of the few leaders in Nike’s history not to have risen through its operating ranks.

Several major strategic shifts followed, each departing from what had worked for Nike for decades – yet each looked like a logical transformational move to take Nike into the 2020s. The financial pay-offs were immediate: gross margins expanded, SGA came down, and return on ad spend looked sharper quarter by quarter. Wall Street loved it.

Yet each of these moves shared a common mechanism: they improved short-term financial metrics by drawing down assets that had taken decades to build. In effect, Nike was not just transforming its business – it was monetising its moat. We will examine each in turn.

______________________________________

The number of patients in their 30s and 40s with late-stage cancer in their lower digestive tract is surgin. It’s not just that these patients are decades younger than what had been typical for colorectal cancer; the tumors themselves are also more stubborn to treat.

Even though young patients are treated with more aggressive chemo or more surgery, patients’ outcomes are not necessarily better. The disease has become the top cancer killer among people under 50, even as death rates decline in older age groups.

Doctors suspect that the gut’s microbiome is a key actor behind these forms of cancer in particular. Patient advocates say it’s critical that more people, especially young adults with a family history of these cancers, get diagnostic testing.Genetics plays some role in colorectal cancers; as many as a fifth of patients have hereditary markers. But genetics do not explain what drives the vast majority (80%) of cases.

Thirty-plus years ago almost zero patients were in clinics under the age of 50 with colon cancer. Now it is almost half. There are other changes in disease pattern with earlier onset tumors that tend to show up differently; more tumors are found near the rectum, lower in the tract.

Experts suspect several factors may be leading to these more frequent, virulent cancers:

- Ultra-processed foods

- Plastics and chemicals that can leach into water and our bodies

- As a population, we are not as active as we used to be.

_________________________

This, of course, has consequences. Here are six:

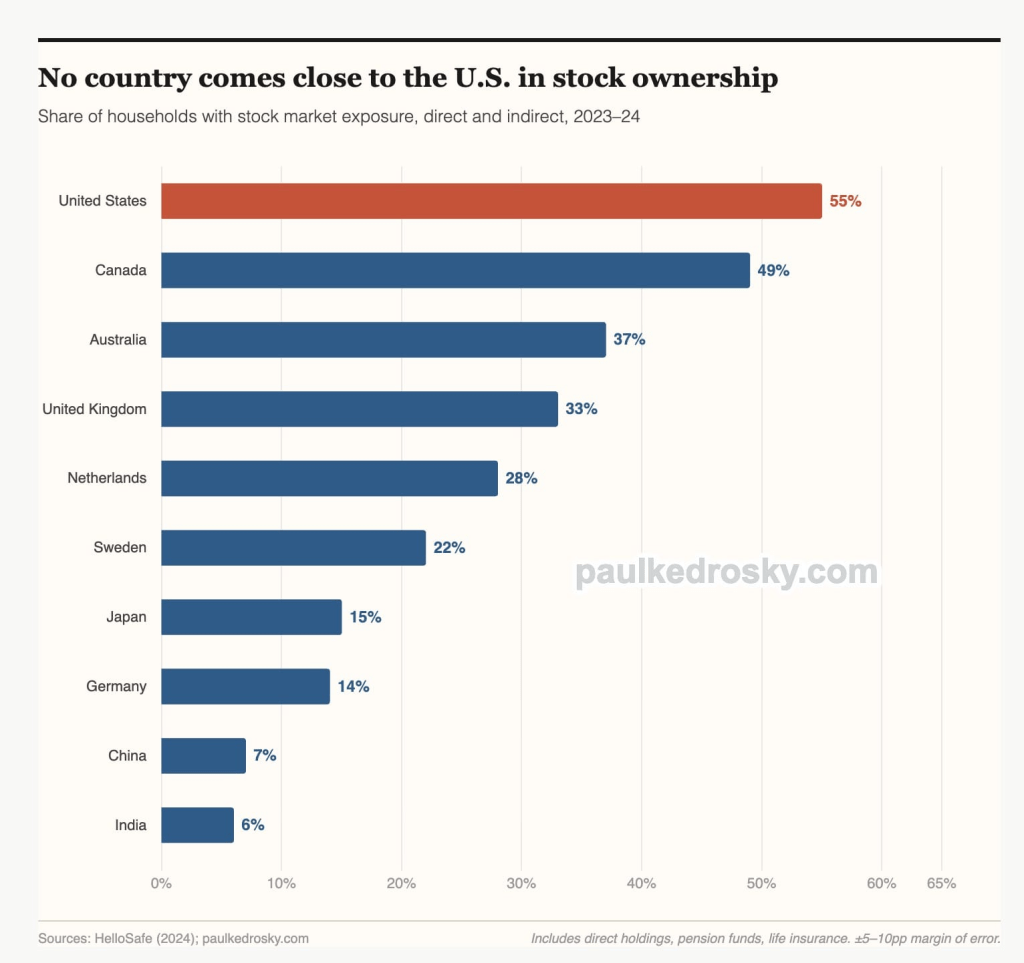

- Monetary policy transmission is direct. When the Fed lowers (raises) rates, US households buy (sell) stocks. No other central bank has this much control over consumer sentiment and spending via markets. The wealth effect makes policy both more powerful and harder to control.

- Markets and politics. When 60% of households own stocks, markets drive elections. Politicians and central bankers in the US hate crashes almost as much as they hate high gas prices. This holds down volatility and encourages wacky risk-taking.

- Passive indexing makes it worse. Most of that 60% own stocks through 401(k)s and IRAs invested in index funds. This means a huge share of American household wealth is concentrated in the same ~500 companies, weighted by market cap. Diversification is an illusion at the aggregate level. Everyone is long NVIDIA, whether they know it (or want it) or not.

- Retirement security is market performance. The US shifted from defined benefit to defined contribution pensions over the last 40 years. A sustained bear market is no longer just a financial event — it’s a retirement crisis.

- Inequality is amplified. The 60% figure is misleading because the bottom half of that cohort owns virtually no stock. The top 10% hold ~90% of equity wealth.

- Contagion from US markets is a virus. Because US households are so deeply exposed, a domestic equity crisis hits consumer spending, which then spreads worldwide through trade. The US market is the world’s risk-off/risk-on switch, and the household exposure ratio is part of why.