Being Content vs. Being Complacent. Complacency is when you lack or deny awareness of potential dangers. It prevents growth. Contentment is feeling satisfied — at peace with what you have today. But it doesn’t stop growth. You can be content while still wanting to be better.

__________________________________

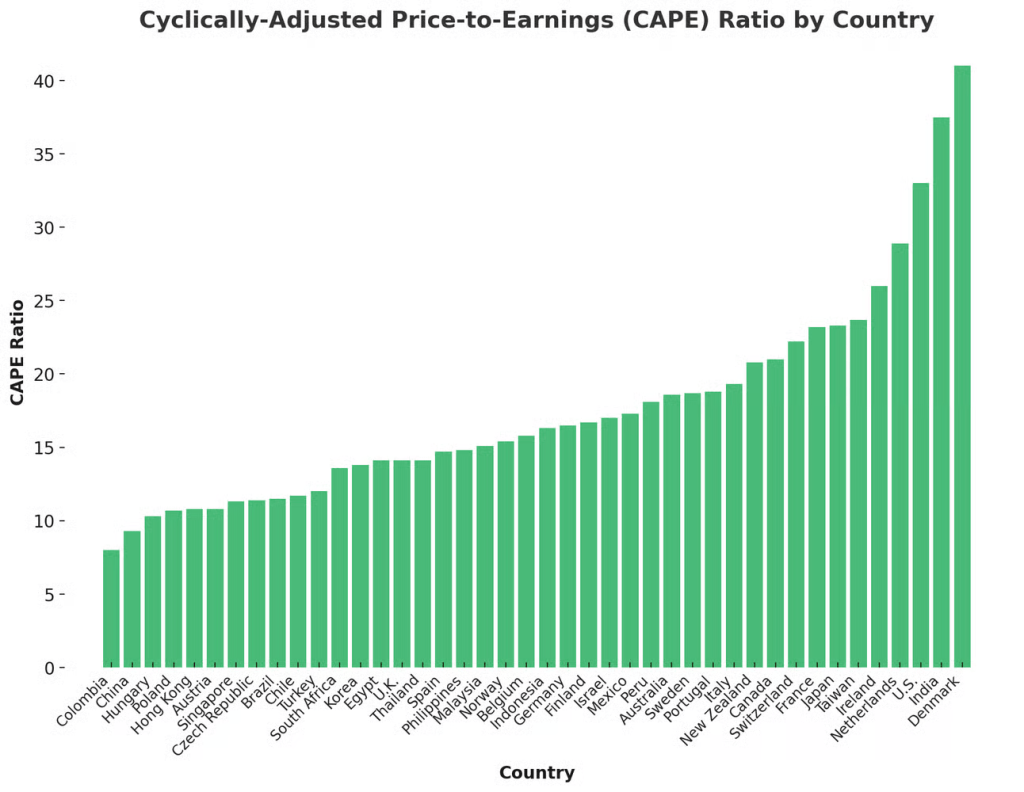

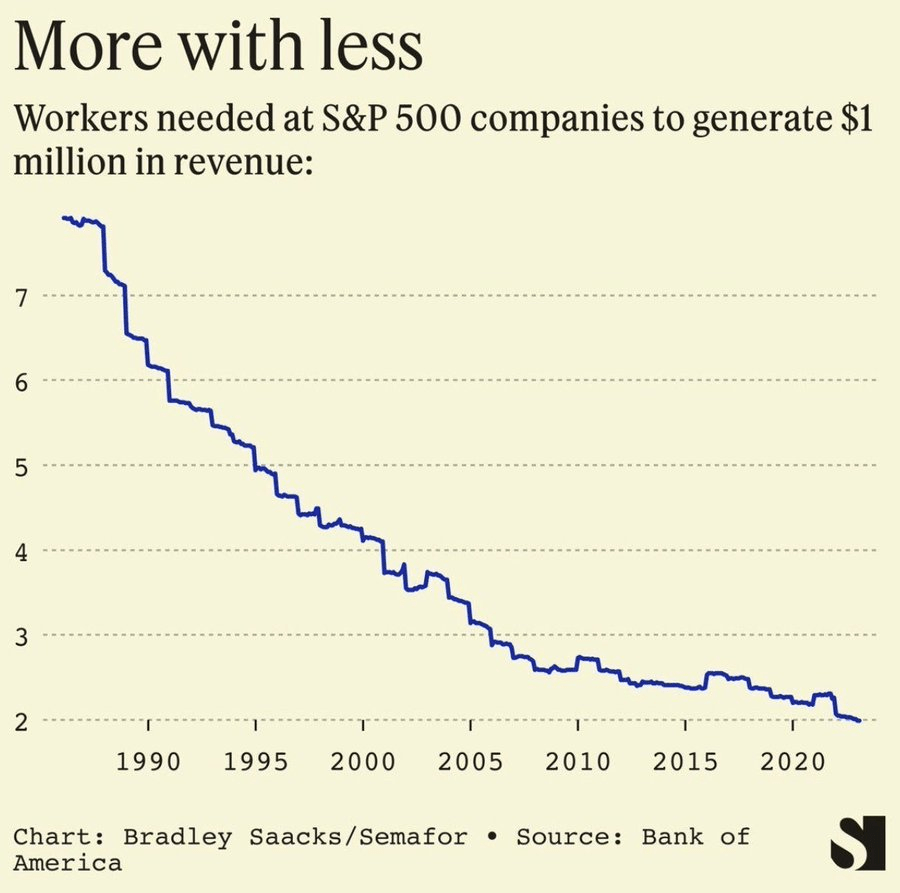

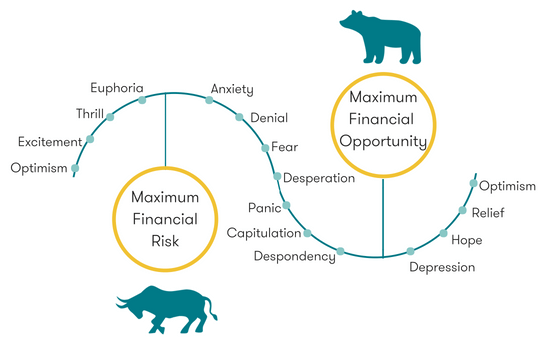

How Much Is Luck Involved vs. How Much Is Repeatable? In business and investing, you want to learn the big lessons about why things behave the way they do without assuming the past is a direct guide to the future, because it’s not – most of the details are not repeatable. History is the study of change, ironically used as a map of the future.

_________________________________

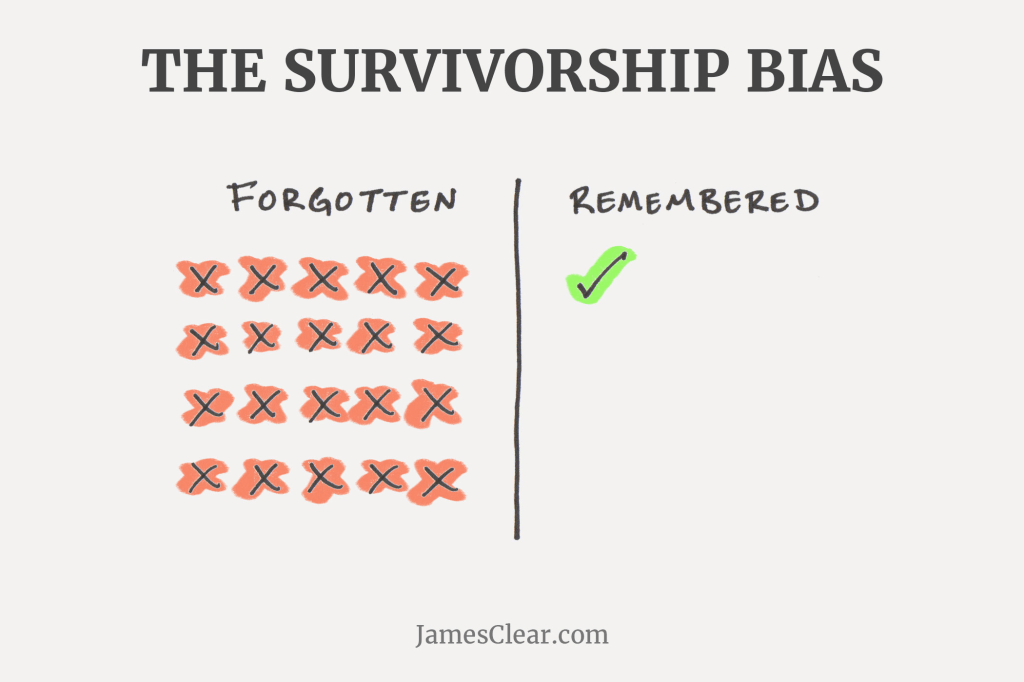

Self-reflection is pointless unless the person in the mirror is you: not the person you wish you were, but the flawed and fallible person you are. Instead of relying on all available information, we jump to sweeping conclusions from fragmentary data. We think vivid events are more frequent than they are. We overestimate our own experience and expertise. We anchor on irrelevant numbers, exaggerate our successes and forget our failures.

_________________________________

Q&A With Ed Thorp on diet, exercise and managing risks in life. Ed wrote the original book on beating blackjack at casinos (“Beath The Dealer”), then created one of the most successful hedge funds in history (he recently wrote a great book about his life called “A Man For All Markets”).

I read a great book last month called “Fluke” that goes into extraordinary detail on how much luck (or flukes) impact everything in the world.

_________________________________

Bill Perkins wrote a book called Die With Zero that has had an enormous impact on my life over the last few years. In this video interview he provides a great analogy on trying to get the order of things correct in your life:

Life is like Tetris…Let’s say you’re in heaven and you’re about to be born and God is like, “Here is the infinite bucket of experiences. Choose what you would like on your adventure.” And you’re like “Okay. This sex thing seems interesting…okay I wanna ride a bike. I wanna get a job. I wanna graduate. I think I wanna get married and have kids. Strip clubs? That seems interesting. I’ll throw in a couple of those.”

God goes, “Okay you can have them all on one condition—you have to get the order right.” So the people that do the marriage thing and have kids and then put the strip club afterwards don’t kind of get the high score. Because it interferes with it…or they put the heliskiing Mt. Kilimanjaro at 86. It’s kind of in the wrong spot, right?

_______________________________

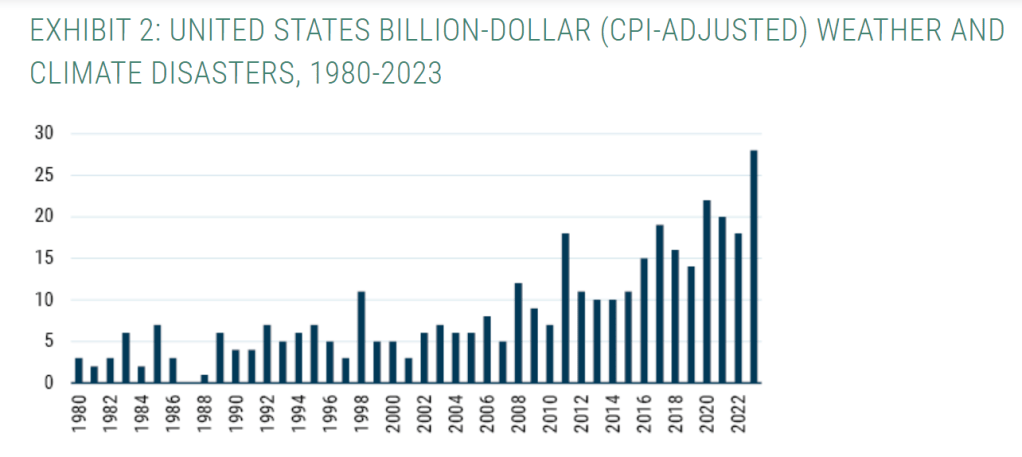

Insurance companies are taking pictures of our homes from the sky. Nearly every building in the country is being photographed, often without the owner’s knowledge. Companies are deploying drones, manned airplanes and high-altitude balloons to take images of properties. The array of photos is being sorted by computer models to spy out underwriting no-nos, such as damaged roof shingles, yard debris, overhanging tree branches and undeclared swimming pools or trampolines. The red-flagged images are providing insurers with ammunition for nonrenewal notices nationwide.

______________________________

Rangan Chatterjee speaks with Laurie Santos on The Happiness Lab Podcast, and they discuss why (and how) physicians like him are making happiness a priority for health.

________________________________