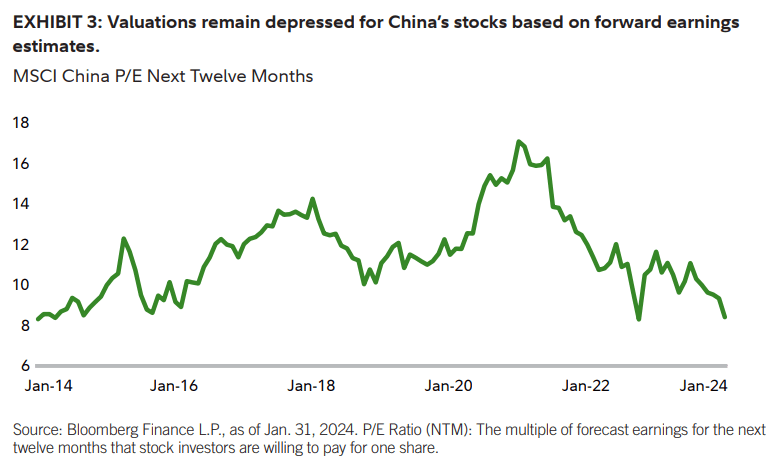

If you zoom out and look at the rest of the world, the concentration is significantly higher in many other markets. This is of interest to me because the majority of my stock market portfolio is in stocks outside the United States. I own value funds that have little exposure to these larger (more expensive) companies that dominate their country’s market, but the concentration is worrisome because selloffs tend to drag everything down together. If the big boys fall, they can bring the smaller stocks down with them.

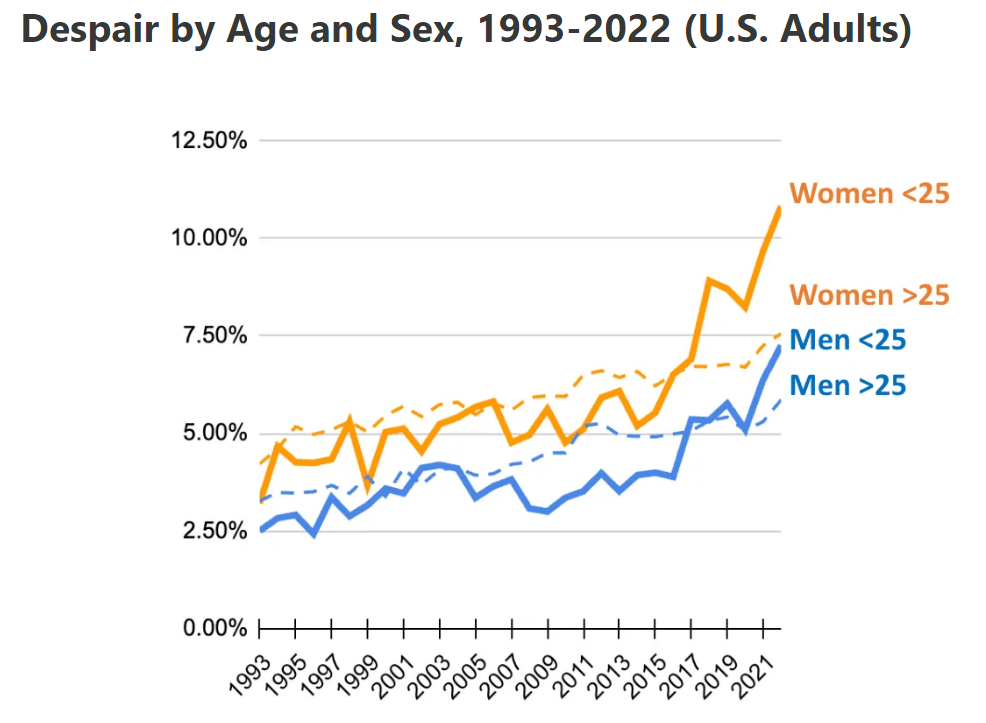

Throughout history happiness for most people followed a U-shaped curve. They were happy in their youth, became less happy during middle age, then became happy again in the later years of life.

Between 1993 and 2016, despair was hump-shaped in age. The rapid rise in despair before the age of 45, and especially before the mid-20s, has fundamentally changed the lifecycle profile of despair such that the hump shape is no longer apparent.

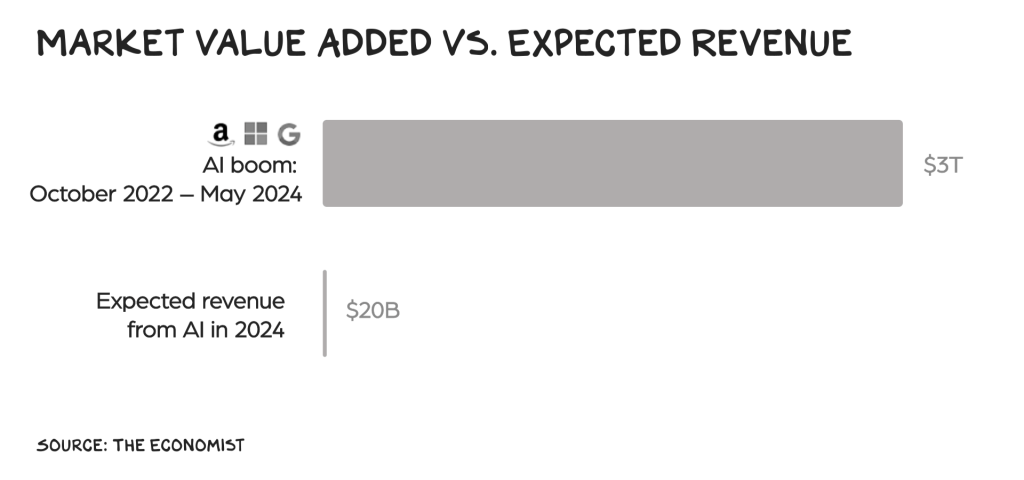

U.S. stocks have crushed the rest of the world over the last 15 years. However, betting on the U.S. from where we are today is effectively a bet on a repeat performance from the Magnificent Seven because, when they’re excluded, there’s nothing extraordinary about US stocks these past 15 years. And an encore is unlikely.

U.S. stock buybacks are back. Analysts at Goldman Sachs project that total S&P 500 repurchases will reach $925 billion this year and $1.075 trillion in 2025, which would mark annual growth rates of 13% and 16%, respectively.

The top 20 PINs (out of 10k) constitute 27% of all PIN numbers.

Birth years are common… you can see the 2000s start to take off

As promised on the “Favorite Books” page (link above), when I come across a book on the financial markets that is a good read for this present moment in time, I will make a note of it here on the main page. I listened to one of those books this past week (it’s currently free to listen to on Spotify):

How much is a memory worth? Memories of experiences tend to increase in value over time – even if the experience doesn’t last long. Physical “Stuff” tends to last longer, but the value usually decreases over time. You can think of experiences vs. physical goods like appreciating assets vs. depreciating assets.

One piece of this equation of memories growing in value is because our ability to recall is quite poor. As time goes on, we also tend to remember the positive things more and block out the negatives.

If you share an experience, it creates a bond. When it comes to “stuff,” people don’t share, they compare.

“It’s not the bond market of the 1980s or 1990s or even the 2000s anymore. It’s a big, bloated bond market that requires constant intervention by fiscal policymakers and monetary policymakers. There are pockets of information and pockets of opportunity here and there, but the overall market itself is not what it used to be.

Inflation manifested in recent years without the bond market anticipating it at all, and it can certainly happen again in the future. The same is true for periods of disinflation or economic deceleration. And the bond market can’t really front-run the sheer supply of Treasuries that will be coming to the market over the upcoming years; for the most part it can only respond in real time from the flows.”

Just 2 percent of 12-17 year-old marijuana users consume daily or near daily. It is becoming something of an old person’s drug. As a group, 35-49-year-olds consume more than 26-34-year-olds, who account for a larger share of the market than 18-25-year-olds.

How to protect your keyless car from theft.Auto technology has evolved and many newer cars use wireless key fobs and push-button starters instead of traditional metal keys. That technology makes things easier for thieves. A simple but effective way to stop auto bandits from purloining your key fob signal is to use a Faraday bag or pouch.

How music impacts our brain making us feel different ways. During peak emotional moments in the songs identified by the listeners, dopamine is released in the nucleus accumbens, a structure deep within the older part of our human brain.

Zero To Small Effect: age, gender, education, social class, income, having children, ethnicity, intelligence, physical attractiveness.

Moderate Effect: number of friends, being married, religiousness, level of leisure activity, physical health, conscientiousness, extraversion, neuroticism (negative correlation), internal locus of control.

Large Effect: gratitude, optimism, being employed, frequency of intercourse (yeah, that means what you think it means), percent of time experiencing positive affect, self-esteem.

______________________________

______________________________

Kids in third and fourth grade are beginning to stop reading for fun. It’s called the “Decline by 9,” and it’s reaching a crisis point for publishers and educators. According to research by the children’s publishers Scholastic, at age 8, 57 percent of kids say they read books for fun most days; at age 9, only 35 percent do. This trend started before the pandemic, experts say, but the pandemic accelerated things.

No one has the ability to predict what will happen in the financial markets. For most of its existence, the investment business was driven by information. Today, and unlike the past, most of us have access to the same information. What it means has now taken center stage. The world we live in is infinitely complex. We like to think that intelligence and effort can readily overcome the vagaries of the markets. That’s largely because we are addicted to certainty. However, the financial markets are simply too complex and too adaptive to be readily predicted.

_________________________

There is a beautiful and melancholic word I like called anemoia. It means nostalgia for a time or a place one has never known. This is a sentiment I often sense from Gen Z—especially in recent years. New technologies cheapen and undermine every basic human value. Friendship, family, love, self-worth—all have been recast and commodified by the new digital world: by constant connectivity, by apps and algorithms, by increasingly solitary platforms and video games. I watch ‘90s videos, and I have the overwhelming sense that something has been lost. Something communal, something joyous, something simple.

SEINFELD: In the eighties, this is the tragic turn of American culture. And this was explained to me by Mario Joiner who cracked this puzzle that I could not figure out what the hell happened. That money became everything. It was not like that in the seventies. In the seventies, it’s how cool is your job? How cool is what you’re doing? If your job’s cooler than my job, you beat me.

Envy is inversely correlated with self-examination. The less you know yourself, the more you look to others to get an idea of your worth. But the more you delve into who you are, the less you seek from others, and the dissolution of envy begins.

One of the most important skills of the future will be learning how to become indistractable. The root cause of human behavior is the desire to escape discomfort. The truth is, we overuse video games, social media, and our cell phones not just for the pleasure they provide, but also because they free us from psychological discomfort. Distraction, then, is an unhealthy escape from bad feelings.

When Raymond Dolphin became assistant principal of a middle school in Connecticut two years ago, it was clear to him that the kids were not all right. The problem was cellphones. So in December, Dolphin did something unusual: He banned them. The experiment has already generated profound and unexpected positive results.

__________________________________

A few short stories on seat belts, Dunkirk, Notorious BIG, shorting housing, and astronauts.

You need to move beyond a rational return analysis to understand why poor people play the lottery. The average American living in the poorest 1% of zip codes spends $600 a year, or $50 per month, on lottery tickets. Assuming they bought tickets for 30 years, their total lottery spending would’ve been $18,000. If they had saved that money in cash instead, this means they could’ve had an extra $50 per month for 30 years in retirement.

There is a profound difference between thinking less of yourself (not useful) and thinking of yourself less (better).

Forget trying to decide what your life’s destiny is. That’s too grand. Instead, just figure out what you should do in the next 2 years.

Interview your parents while they are still alive. Keep asking questions while you record. You’ll learn amazing things. Or hire someone to make their story into an oral history, or documentary, or book. This will be a tremendous gift to them and to your family.

Asking “what-if?” about your past is a waste of time; asking “what-if?” about your future is tremendously productive.

Discover people whom you love doing “nothing” with and do nothing with them on a regular basis. The longer you can maintain those relationships, the longer you will live.

Humility is mostly about being very honest about how much you owe to luck.

_________________________________

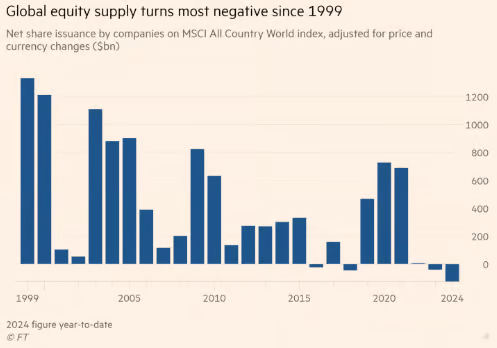

Net share issuance (the amount of new stock being issued vs. how much companies are buying back) is shrinking at the fastest pace in 25 years:

Car insurance premiums have been skyrocketing due to car and auto parts prices rising, drivers getting worse, and more vehicles being damaged by storms. Even with the increase in premiums, the payouts have been higher for private insurers the last few years.

__________________________

Great interview with Scott Galloway where he lightly discusses some of the topics of his new book, The Algebra Of Wealth, before going into a deeper, introspective conversation about his personal life in his 20s, 30s and 40s. He talks about the mistakes he made and the things that were worth it.

__________________________

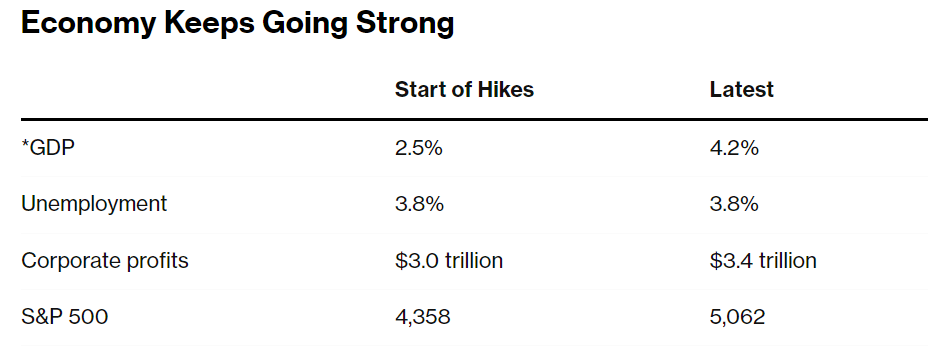

It’s well understood how Fed rate hikes slow areas of the economy (real estate transactions, consumer loans and small business loans), but they also stimulate the economy in other ways. Bloomberg discussed it this week noting: the jump in benchmark rates from 0% to over 5% is providing Americans with a significant stream of income from their bond investments and savings accounts for the first time in two decades.

The government’s debt has ballooned to $35 trillion, double what it was just a decade ago. That means those higher interest rates it’s now paying on the debt translate into an additional $50 billion or so flowing into the pockets of American (and foreign) bond investors each month.

US households receive income on more than $13 trillion of short-term interest-bearing assets, almost triple the $5 trillion in consumer debt, excluding mortgages, that they have to pay interest on. At today’s rates, that translates to a net gain for households of some $400 billion a year.

__________________________________________

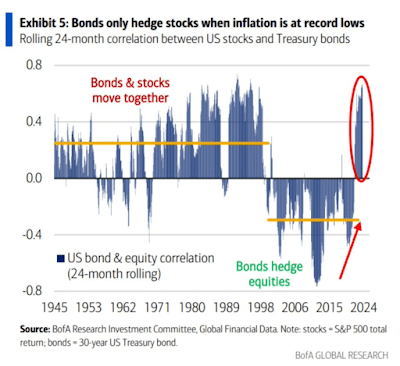

Bonds and stocks started moving together recently (stocks falling in price while bond interest rates rise meaning their underlying value falls). This is a new phenomenon for most investors (including me: I’m only 41). However, the graphic below shows that from 1940 to 2000 stocks and bonds moved together the majority of the time: