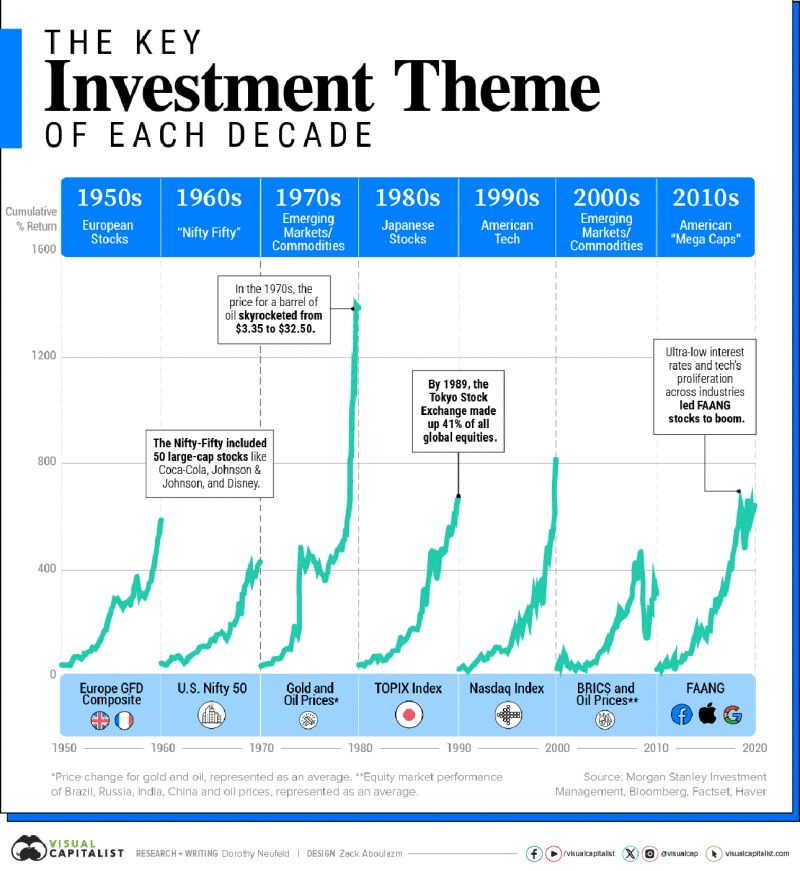

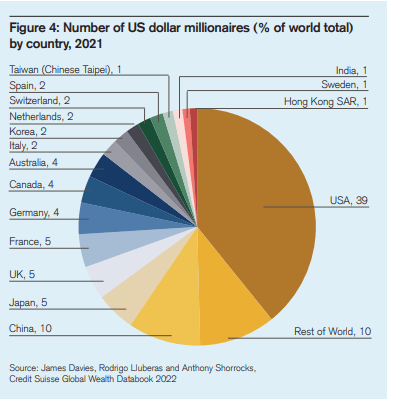

We always hear how the United States stock market capitalization is concentrated in the Magnificent Seven, but other countries have a far higher concentration:

A.I. has already begun to increase productivity for companies, a trend that will likely continue as we move forward:

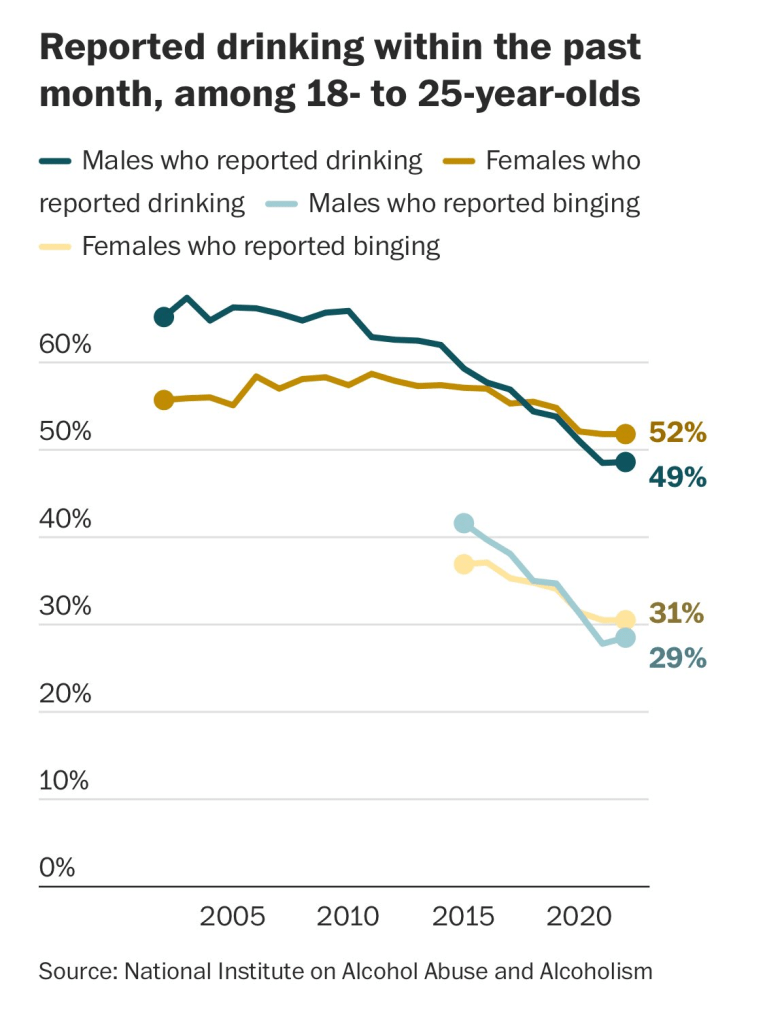

Results From A Study On Zero Tolerance Alcohol Laws For Kids Under 21 – “We find that Zero Tolerance Laws led to significant improvements in later-life health. Individuals exposed to the laws during adolescence were substantially less likely to suffer from cognitive and physical limitations in their 40s. The health effects are mirrored by improved labor market outcomes. These patterns cannot be attributed to changes in educational attainment or marriage. Instead, we find that affected cohorts were significantly less likely to drink heavily by middle age, suggesting an important role for adolescent initiation and habit-formation in affecting long-term substance use.”

Lakers’ LeBron James is the first NBA player to score 40,000 points. James scored his first 10,000 points in the exact same number of games as it took him to go from 30,000 to 40,000 – 10K in 368 games – 10K to 20K in 358 games – 20K to 30K in 381 games – 30K to 40K in 368 games.

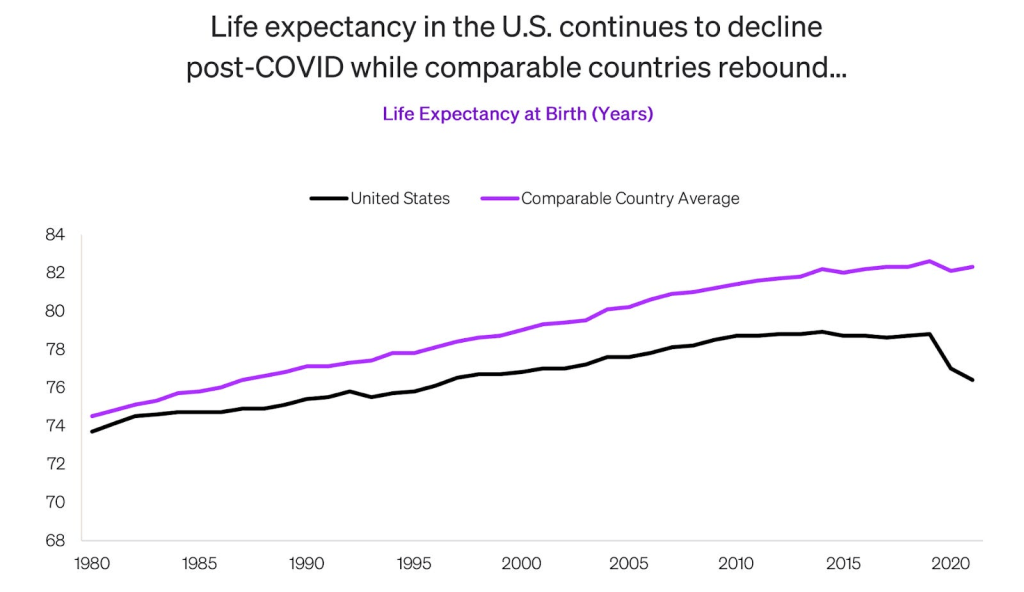

One quick note on the graph above. I’ve read/heard that one of the biggest reasons America’s average lifespan is so low compared to other developed countries is due to the enormous number of young men that are killing each other (mostly with guns) in the United States. Those (young) deaths pull the average down significantly.

Some of the pandemic darlings are still down 76% or more:

Why Appliances Break Down More Often Than They Used To – When a complicated machine fails, technicians say they have a much harder time figuring out what went wrong. Even if the technician does diagnose the problem, consumers are often left with repairs that exceed half the cost of replacement, rendering the machine totaled. In the majority of cases, buying a new one makes more economic sense than repairing it.

The argument against a P/E ratio that looks backward is that companies can grow their earnings in the future in order to validate their higher price. This is obviously true, and it’s exactly what some of the higher growth companies, concentrated in U.S. technology, have done over the last 14 years.

The graph below looks at forward P/E ratios for different countries. Instead of looking backward, this takes current prices and projects them against future earnings. These P/E ratios are almost always lower than those that look backward because Wall Street analysts and companies (that make their money selling stocks) want them to look less expensive and more attractive. They do this by projecting strong future earnings growth. I do the same thing when selling commercial real estate (investors need to project income growth over the coming years in order to model returns).

Even using forward estimated P/E assumptions, this model gives you a view of countries that are expensive (red) and those that are inexpensive (green).

The problem comes when you’ve already priced in massive future growth (higher forward P/E ratios), and there is a speedbump along the way. The company has to deliver on the lofty projections.

The opposite occurs when you’re looking at inexpensive stocks or countries. If valuations are already low, and future earnings are projected to be low, any news that’s more positive to the upside can become a catalyst upward for prices.

I like to do the latter; buy companies and regions that are out of favor at low valuations. That may sound obvious, but that strategy has significantly underperformed over the last 14 years. The investors that purchased high projected growth expensive companies (technology) in expensive countries (the United States) have vastly outperformed almost everything else.

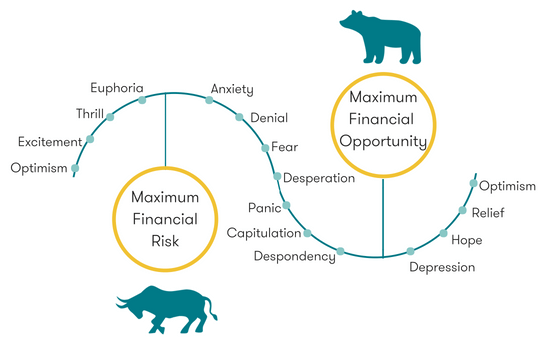

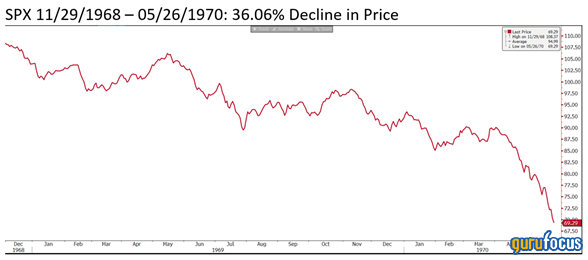

“The failure of the general market to decline during the past year despite its obvious vulnerability, as well as the emergence of new investment characteristics, has caused investors to believe that the U.S. has entered a new investment era to which the old guidelines no longer apply. Many have now come to believe that market risk is no longer a realistic consideration, while the risk of being underinvested or in cash and missing opportunities exceeds any other.

– Barron’s Magazine, February 3, 1969

The S&P 500, having peaked a few weeks earlier, was down 36% by May 1970. Perhaps more importantly, the cumulative total return of the S&P 500 lagged the cumulative return of Treasury bills from November 1968 until December 1985.

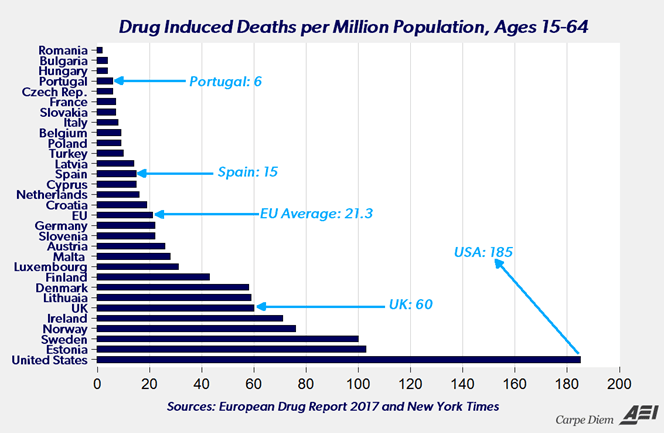

Portugal Has Nearly Eliminated Drug Overdoes While U.S. Deaths Continue To Skyrocket Higher – Portugal has roughly the same population as the state of New Jersey. But while New Jersey alone sees nearly 3,000 fatal drug overdoses a year, Portugal averages around 80. What’s different in Portugal? In the late 1990s, the country faced an explosion of heroin use. The drug was causing roughly 350 overdose deaths a year and sparked a wave of HIV/AIDS and other diseases linked to dirty needles. Portugal’s leaders responded by pivoting away from the U.S. drug war model, which prioritized narcotics seizures, arrests and lengthy prison sentences for drug offenders. Instead, Portugal focused scarce public dollars on health care, drug treatment, job training and housing. The system, integrated into the country’s taxpayer-funded national health care system, is free and relatively easy to navigate.

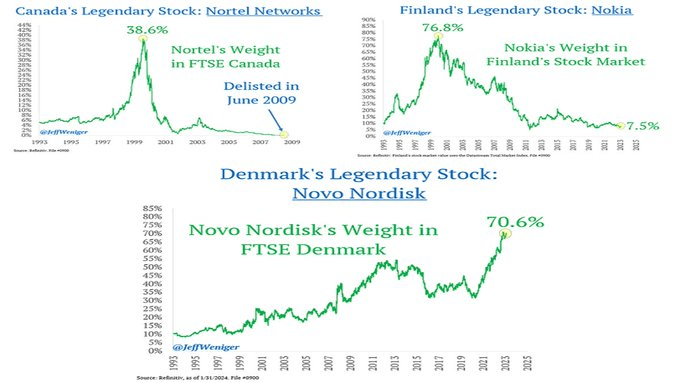

At its peak, Nortel reached 38.6% of Canada’s stock market. The stock went to zero. In Finland, Nokia reached 76.8% of the stock market’s total value. Today, Novo Nordisk is 70.6% of Denmark’s stock market:

After 35 years, the Japanese stock market has finally reached new record highs. You can see the moment on the chart below when “Abenomics” was introduced in Japan:

Abenomics was a “three quiver” approach to try and boost the markets and economy. It involved (1) structural reforms (2) deficit spending and (3) massive money printing:

The other thing that helped start the rally in Japanese stocks back in 2012 was a low price to earnings valuation.

The CAPE ratio (Shiller Price to Earnings ratio) reached 80 at the peak of Japan’s stock market bubble in 1989. That means investors were willing to pay 80 times the average earnings over the previous 10 years. The price to earnings ratio bottomed in 2012 at 16.

Investors once willing to pay 80 times earnings now wanted nothing to do with stocks paying 16 times earnings. There was extreme pessimism and investors (after being destroyed in the market for 23 straight years) understandably had given up.

Here are some other high-water marks for the CAPE Price To Earnings ratio in other stock markets over the last 35 years:

In 1998 Switzerland reached 58.

In 2000 Germany hit 58. Canada, France, Germany and Italy all crossed 60, while Sweden hit 80.

In 2007, China hit 60 and India reached 48.

Just like Japan, all of these countries have experienced horrific returns since their price to earnings valuation peaks. Some are still well below their all-time highs, 17 to 26 later.

The United States stock market reached 47 in March 2000 at the peak of the dot com bubble. It reached 39 in late 2021 and sits around 34 today (February 2024). It’s currently one of the most expensive stock markets in the world.

The following is a quick snapshot/summary of where price to earnings valuations stood for countries around the world entering 2024:

Average of Foreign Developed Countries: 19 (38% less expensive than the United States) Average of Foreign Emerging Countries: 15 (51% less expensive than the United States)

What does this mean for the United States stock market moving forward? Reviewing the history of other stock market bubble peaks above, there is plenty of room for valuations to go much higher from where they are today.

Fortunately for us, we don’t have to invest in an expensive stock market (the United States). We can invest in other markets around the world that are much less expensive, typically pay higher dividends, and offer a higher probability of stronger returns relative to the U.S. moving forward.

The Dark Side of the Internet’s Obsession with Anxiety (Podcast) – Derek Thompson asks if we have “overcorrected” from an era when mental health was shameful to talk about, to an era where people talk about anxiety so much online that it’s now possibly worsening mental health?

Anger Leaves A Lasting Mark – After unleashing a critical barrage on your child, you seek to justify it, mitigate it, by saying how overworked and stressed out you’ve been. But your child doesn’t register this context at the time, and ten, twenty, thirty years later, it will still very much be forgotten, while the sting of your words indelibly remains.

However, the concentration is even greater in other stock markets around the world:

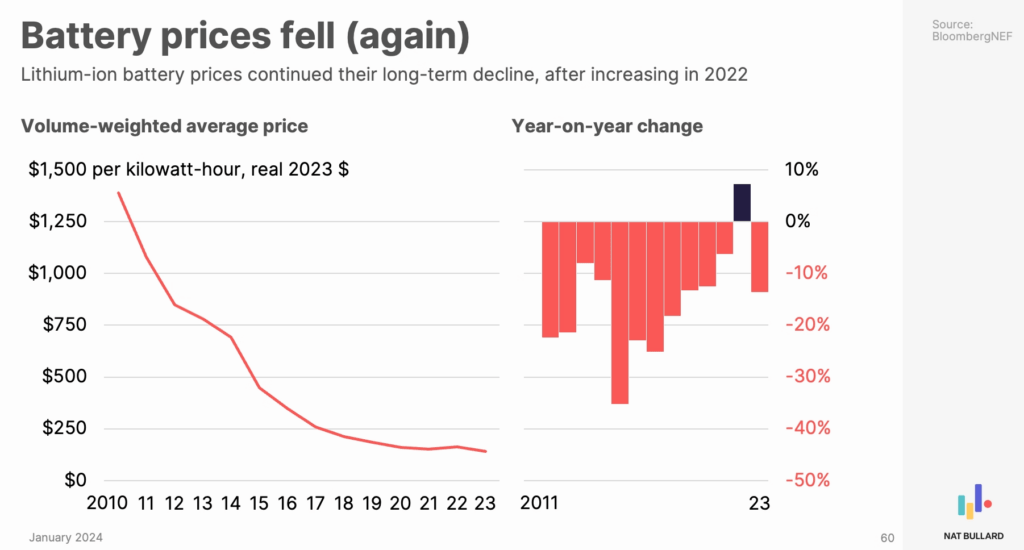

Lithium battery prices continue to get cheaper:

A scathing review of Tony Robbins new book on investing in private investments. The article was written by someone who makes a living keeping his clients in public investments. Not saying there’s anything wrong with that, but if you ask a realtor what someone should invest in, I think you can guess what their answer will be.

I started blogging way back in 2006, and 18 years later I guess I’m still going. For those of you that found this site because you were forwarded here from my previous site, thanks for continuing the journey.

I’m 41 years old now, with a wonderful wife, amazing daughter and real estate company that consume most of my mental energy and thoughts.

While I don’t have the time to write that I did 10 to 15 years ago, I still spend many (probably too many) hours every week reading books/articles and listening to books/podcasts about the financial markets, real estate and behavioral psychology.

My hope is to start writing down more of the things I come across that I find interesting, or worth recommending, here on the site. I’ve realized after doing this for a long time that when I take the time to write things down it helps me remember them. As I move into the second half of my life, remembering things will probably become more and more important.

Hopefully people stopping by this site will find some of these thoughts interesting as well, and we can continue learning together. Here’s to 18 more years!